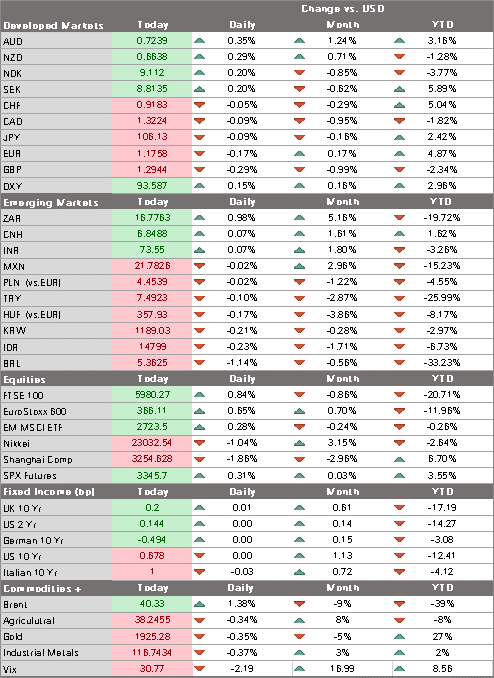

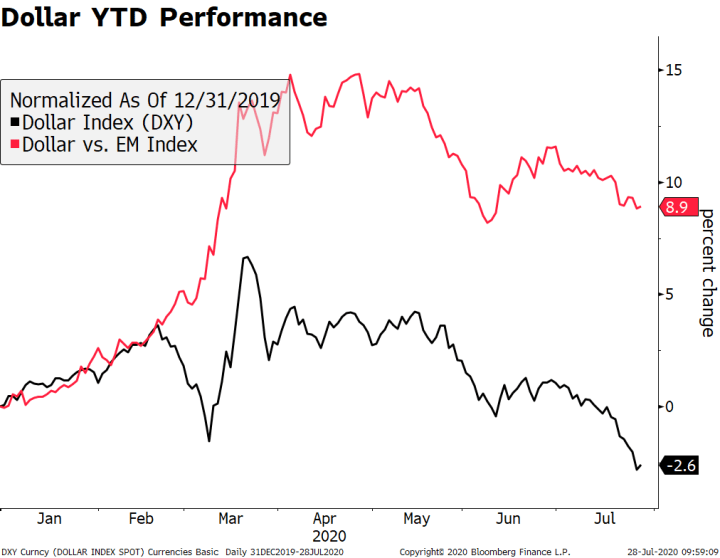

The dollar rebound continues; odds of a near-term stimulus bill in the US are falling; ahead of inflation readings later this week, the US holds a 10-year auction today Bank of Canada is expected to keep policy steady; Mexico reports August CPI; Brazil reports August IPCA inflation The Brexit fallout widens; UK will have trouble striking new trade deals if it can’t be counted on to honor its past agreements; no surprise then that sterling remains under pressure Australia September Westpac consumer confidence rose to 93.8 from 79.5 in August; New Zealand 3-year bond yields turned negative for the first time ever The dollar rebound continues. DXY is trading at the highest level since August 12. However, for us to get more constructive on the greenback, DXY would

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, Daily News, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

- The dollar rebound continues; odds of a near-term stimulus bill in the US are falling; ahead of inflation readings later this week, the US holds a 10-year auction today

- Bank of Canada is expected to keep policy steady; Mexico reports August CPI; Brazil reports August IPCA inflation

- The Brexit fallout widens; UK will have trouble striking new trade deals if it can’t be counted on to honor its past agreements; no surprise then that sterling remains under pressure

- Australia September Westpac consumer confidence rose to 93.8 from 79.5 in August; New Zealand 3-year bond yields turned negative for the first time ever

The dollar rebound continues. DXY is trading at the highest level since August 12. However, for us to get more constructive on the greenback, DXY would have to break above the 94.00 area, which represents some highs from August as well as the 38% retracement objective of its fall from the June 30 peak. This corresponds with the $1.17 area for the euro and the $1.30 area for sterling. Sterling is leading this move, having already broken below that level on negative Brexit developments. Much will depend on whether US equity markets can regain some traction this week. If not, continued stock market losses could morph into a more broad-based risk-off trading environment that gives the dollar another boost higher. US stock futures are pointing to a higher open today but sentiment is likely to remain fragile. Stay tuned.

AMERICAS

Odds of a near-term stimulus bill in the US are falling. As noted yesterday, Senate Leader McConnell plans to pass a “skinny” bill worth $500-700 bln this week but needs Democratic support to get the 60 votes. It would restore $300 per week of enhanced jobless benefits, as well as provide $100 bln for schools, $10 bln for the Postal Service, and $258 bln for the Paycheck Protection Program for small businesses. What’s missing is another round of $1200 stimulus checks and any state and local aid. As such, House Speaker Pelosi called this smaller package “fraudulent” and so we assume it will be dead in the water.

Ahead of the August PPI and CPI readings later this week, the US Treasury holds a 10-year auction today. $35 bln will be on offer. Tomorrow, it will sell $23 bln of 30-year bonds. The sales come after a largely lackluster showing at the quarterly refunding last month. Back then, the 3-year leg went fine but the 10- and 30-year legs did not as bid to cover ratios fell to 2.41 and 2.14, respectively, and high yields rose to 0.677% and 1.406%, respectively. The only US data report today is July JOLTS job openings , which are expected at 6000 vs. 5889 in June.

Bank of Canada is expected to keep policy steady. The bank has been on hold since its last 50 bp cut March 27. At its last policy meeting July 15, Governor Macklem noted that the bank’s economic forecasts suggest that rates will remain at current levels for at least two years. Note that the Loonie tends to gain on BOC decision days. In four of the past five, the currency has strengthened. USD/CAD is trading at the highest level since August 17 after finding strong support near the 1.30 area last week. The 1.3245 area is key, as a clean break above would set up a test of the August 7 high near 1.34.

Mexico reports August CPI. Headline inflation is expected to accelerate to 4.04% y/y from 3.62% in July. If so, it would be the highest since May 2019 and above the 2-4% target range. Banco de Mexico has cut rates at every meeting this year. At its last meeting August 13, it cut rates 50 bp to 4.5% and signaled further easing was likely. Next policy meeting is September 24 and rising inflation makes this a tough call. While we had thought another 50 bp cut to 4.0% was likely, the bank may be forced by rising inflation to do a more cautious 25 bp move then.

Brazil reports August IPCA inflation. It is expected to accelerate to 2.44% y/y from 2.31% in July. If so, it would be the third straight month of acceleration and the highest since March and just below the 2.5-5.5% target range. At the last COPOM meeting August 5, it cut rates 25 bp to 2.0% and left the door open for further easing. Next meeting is September 16 and no change is expected then as we believe the easing cycle has ended.

| EUROPE/MIDDLE EAST/AFRICA

The Brexit fallout widens. Two of the UK government’s most senior legal advisors quit over professed plans to abrogate portions of the Brexit Withdrawal Agreement. More specifically, the UK plans to revoke its agreement to keep Northern Ireland aligned with EU customs rules. Northern Ireland Minister Lewis admitted to Parliament that an attempt to rewrite any portion of the deal would “break international law, in a very specific and limited way.” UK will have trouble striking new trade deals if it can’t be counted on to honor its past agreements. Ireland Deputy Prime Minister, Varadkar put it best when he said that “A country either abides by the rule of law or it does not, it honors international treaties and obligations or it does not.” Many of the staunchest critics come from Johnson’s own Tory party, with former Prime Minister May asking “How can the government reassure future international partners that the UK can be trusted to abide by the legal obligations of the agreements it signs?” While some are chalking this up to mere brinksmanship, there is more to this than meets the eye. Either way, it is a very risky gamble to take at such a crucial juncture in the Brexit talks. No surprise then that sterling remains under pressure. Cable is trading below $1.30 and at the lowest level since July 29. The break below $1.2965 sets up a test of the July 22 low near $1.2645, with intermediate support seen at the 200-day moving average currently near $1.2740. Elsewhere, the EUR/GBP cross traded above .9100 today and is on track to test the July 27 high near .91482 and then the June 29 high near .91759. ASIA Australia September Westpac consumer confidence rose to 93.8 from 79.5 in August. Yesterday, August NAB business conditions came in at -6 vs. 0 in July and business confidence came in at -8 vs. -14 in July. The economic outlook remains mixed as the RBA left rates steady last week but expanded its Term Funding Facility for banks. The RBA also signaled willingness to ease further, noting that it “continues to consider how further monetary measures could support the recovery.” Rising tensions with China has weighed on the Aussie. AUD found some support today just below the .7200 level, the lowest since August 26. New Zealand 3-year bond yields turned negative for the first time ever. This largely reflects rising market expectations that the RBNZ will eventually take its policy rate negative. This has gathered steam after the bank acknowledged that it would consider negative rates at its August 12 meeting. It also unexpectedly expanded QE then. Next policy meeting is September 23 and no change is expected. However, the bank will likely address the issue of negative rates in greater detail now that the market is doing the heavy lifting for it. NZD found some support near the .66 area but the near-term direction will still depend largely on the broader USD trend. |

. |

You Might Also Like

Dollar Begins the Week Under Pressure Again

Dollar Begins the Week Under Pressure Again

The virus news stream remains negative; pressure on the dollar has resumed. The US economy is taking a step back just as Q3 is about to get under way; there are some minor US data reports today. UK Labour leader Starmer overtook Prime Minister Johnson in the latest opinion poll; Macron’s party did poorly in French local elections.

Dollar Bid as Market Sentiment Yet to Recover

Dollar Bid as Market Sentiment Yet to Recover

The US has started the formal process of withdrawing from the WHO; the dollar continues to benefit from risk-off sentiment but remains stuck in recent ranges. The White House is asking Congress to pass another $1 trln stimulus plan by early August; President Trump hosts Mexican President AMLO for a two-day visit.

Market Sentiment Dented by Weak Data and Rising US-China Tensions

Market Sentiment Dented by Weak Data and Rising US-China Tensions

Market sentiment has been dented by more than just rising virus numbers; yet the dollar continues to trade within recent well-worn ranges. California’s decision to reverse partial reopening will likely have a huge economic impact; June CPI may hold a bit more interest in usual; June budget statement is worth a quick mention.

Market Sentiment Boosted by Stimulus Outlook

Market Sentiment Boosted by Stimulus Outlook

Today, it’s all about the stimulus; the dollar remains under pressure. Mnuchin and Pelosi kick off the first round of talks for the next stimulus package this afternoon; it’s another quiet day in terms of US data; Canada reports May retail sales

EU finalized its recovery package; UK reported June public sector net borrowing; Hungary is expected to cut rates 15 bp to 0.60%.

Dollar Remains Under Pressure as European Outlook Shines

Dollar Remains Under Pressure as European Outlook Shines

The outlook for risk assets remains uncertain; the dollar continues to make new lows; the uncertain outlook continues to propel gold and silver higher. The next round of stimulus in the US is proving to be difficult; regional Fed manufacturing surveys for July will continue to roll out. German July IFO survey came in better than expected; eurozone June M3 rose 9.2% y/y vs. 8.9% in May.

Dollar Stabilizes but Further Losses Likely

Dollar Stabilizes but Further Losses Likely

The dollar is stabilizing today but further losses are likely. Senate Republicans have proposed a sharp cut to weekly unemployment benefits; Senator Collins will oppose Judy Shelton’s nomination to the Fed. Regional Fed manufacturing surveys for July will continue to roll out; early July reads for the US economy support our view that Q3 is off to a rocky start.

Dollar Weak Ahead of Likely Dovish Hold from the Fed

Dollar Weak Ahead of Likely Dovish Hold from the Fed

The FOMC decision today is likely to deliver a very dovish tone; the dollar tends to weaken on FOMC decision days. Tensions about the latest US stimulus bill are rising; core bond yields have been remarkably stable over the last several months.

Dollar Softens, Equities Rise as Markets Ignore the Negatives

Dollar Softens, Equities Rise as Markets Ignore the Negatives

Markets seem to be increasingly desensitized to the usual negative drivers; the dollar is under pressure again. Stimulus talks remain stalled; reports suggest Trump is mulling a capital gains tax cut of some sort. US data highlight today will be July PPI; US Treasury begins its record $112 bln quarterly refunding.

Tags: Articles,Daily News,Featured,newsletter