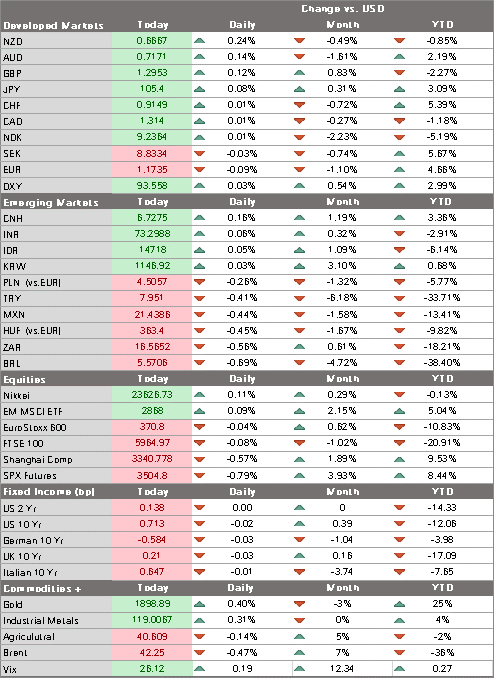

The dollar is making a modest comeback; stimulus talks have hit a dead end; we get more US inflation readings for September Brexit talks continue ahead of the EU summit Thursday and Friday; a new bill by the UK government could change the investment landscape in the country The EU recovery fund has hit some speed bumps; the Netherlands is the latest country to impose stricter measures; eurozone IP came in slightly lower than expected China reported strong money and loan data; Singapore and Korea kept monetary policy unchanged, as expected The dollar is making a modest comeback. Friday saw the biggest down day for DXY since August 28, but it has since risen three straight days and is stabilizing just above the 93.50 area. It has traded largely in a 93-94 range

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, Daily News, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

- The dollar is making a modest comeback; stimulus talks have hit a dead end; we get more US inflation readings for September

- Brexit talks continue ahead of the EU summit Thursday and Friday; a new bill by the UK government could change the investment landscape in the country

- The EU recovery fund has hit some speed bumps; the Netherlands is the latest country to impose stricter measures; eurozone IP came in slightly lower than expected

- China reported strong money and loan data; Singapore and Korea kept monetary policy unchanged, as expected

The dollar is making a modest comeback. Friday saw the biggest down day for DXY since August 28, but it has since risen three straight days and is stabilizing just above the 93.50 area. It has traded largely in a 93-94 range this month. With the US outlook softening, that 94 area will be very tough to break. Once this period of consolidation ends, we look for dollar weakness to resume. The euro is likely to find some support near $1.17, while sterling continues to be buffeted by Brexit-related headlines. Despite lack of concrete progress on a Brexit deal, sterling is holding up well and could test the $1.30 again.

AMERICAS

Stimulus talks have hit a dead end. House Speaker Pelosi has reportedly asked the White House to revamp its latest offer of $1.8 trln. The problem here remains that Senate Republicans are not on board with anything close to that amount. In fact, Senate Majority Leader McConnell is planning a vote next week on an even skinnier bill than the one previously passed by the Senate. Talks are said to be continuing this week but with both sides dug in, this really seems to be the end of the line.

We get more US inflation readings for September. PPI will be reported today, with headline and core inflation expected to accelerate to 0.2% y/y and 1.0% y/y, respectively. CPI came in as expected yesterday, with headline rising a tick to 1.4% y/y and core inflation remaining steady at 1.7% y/y. If price pressures rise further, this could provide further fuel to the recent curve steepening trade by hurting demand for USTs. Barkin, Clarida, Quarles, and Kaplan all speak.

| EUROPE/MIDDLE EAST/AFRICA

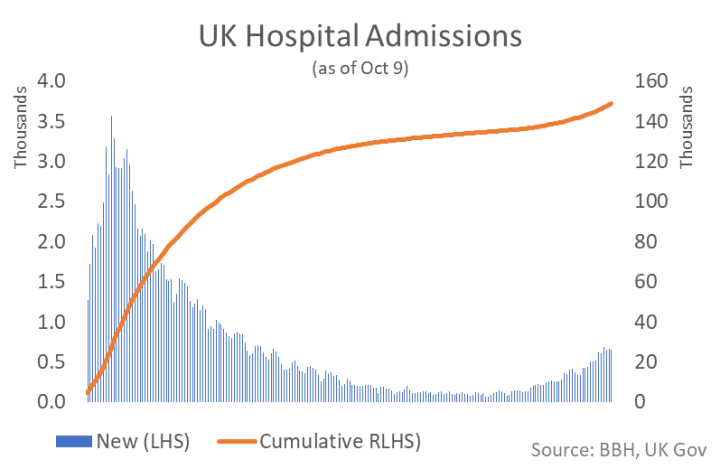

Brexit talks continue ahead of the EU summit Thursday and Friday. Irish Deputy Prime Minister Varadkar said yesterday that there is a better than 50% chance of a Brexit deal. More interestingly, he thinks it will be a skinny deal. We believe this is the first time that it’s been raised, as market pricing has been totally binary – either no deal or a comprehensive deal. To us, a skinny deal is better than no deal and so sterling would probably rally if this happens. A skinny deal would allow both sides to claim victory, avoid a no deal Brexit, and continue talks on the other contentious areas in 2021. A new bill by the UK government could change the investment landscape in the country. The National Security and Investment Bill, which has been discussed for some time, will give policymaker the power to act pre-emptively and retroactively (!) on foreign investments in critical sectors such as defense and infrastructure. China, and 5G technology, are likely the primary implicit targets here. But the bill might do broader damage sentiment for inbound investment in the country, especially once it’s no longer bound by the more predictable EU rules. UK government seems to be digging itself into an ever deeper political hole. In our view, the Internal Markets Bill (to rewrite elements of the Withdrawal Agreement with the EU) was a big miscalculation. It complicated its domestic political situation – by causing a rebellion within its party – and its external position – by creating another hurdle in the negotiations with the EU. To make things worse, the government’s recent 3-tier Covid reaction plan has been seriously criticized by MPs and parts of the scientific community. The Scientific Advisory Group, for example, is now arguing for a 2-week lockdown. The death rate in the UK remains comparatively low, even as cases rise, but hospitalization rates are rising fast. |

UK Hospital Admissions - Click to enlarge |

| The EU recovery fund has hit some speed bumps. Spain’s Economy Minister Calvino said negotiations are “still ongoing” but added that “We are doing our utmost to accelerate this process so that we can start the implementation of the recovery plan on January 1, 2021.” Poland is gumming up the works by threatening to veto the EU budget and recovery plan. The core of the dispute lies with the so-called rule of law clauses that seek to link democratic standards to any funds disbursed by the EU. Hungary and Poland are the main culprits here as their “illiberal democracies” appear to run counter to EU ideals. We do expect an eventual compromise after the bluster dies down.

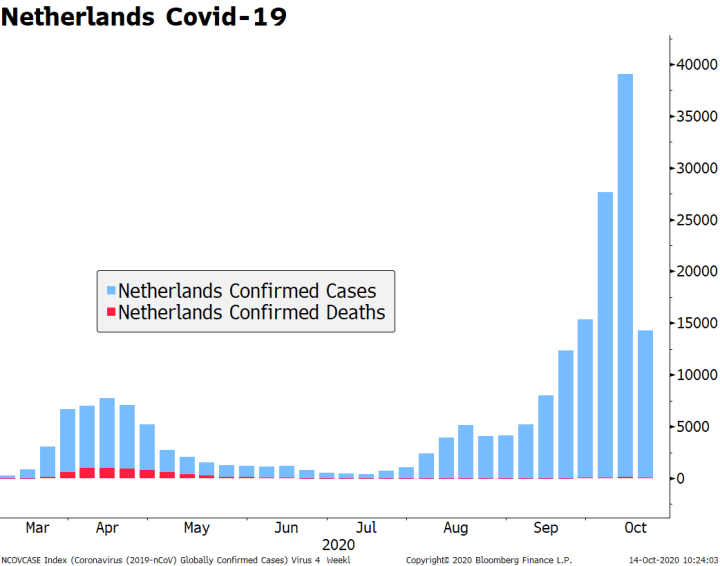

The Netherlands is the latest country to impose stricter measures. The government mandated obligatory use of masks in public and a partial lockdown, with restrictions on gatherings to four people and closure of bars and restaurants. The measures are expected to last four weeks. |

Netherlands Covid-19, 2020 - Click to enlarge |

| On the data front, eurozone industrial production came in slightly lower than expected. August IP rose 0.7% m/m vs. 0.8% expected, grinding slowly back towards pre-pandemic levels. July was revised up to 5.0% m/m from 4.1% previously. The recovery is likely to continue, but at a much slower pace, especially with pendulum swinging towards further restrictive measures in the region. As such, there will be pressure on the ECB to provide more stimulus. We see an increase to its PEPP before year-end. Next meeting is October 29 but we suspect the bank will wait until the December 10 meeting to move, as new macro projections will be released then. |

Euro Area Industrial Production, 2005-2020 - Click to enlarge |

|

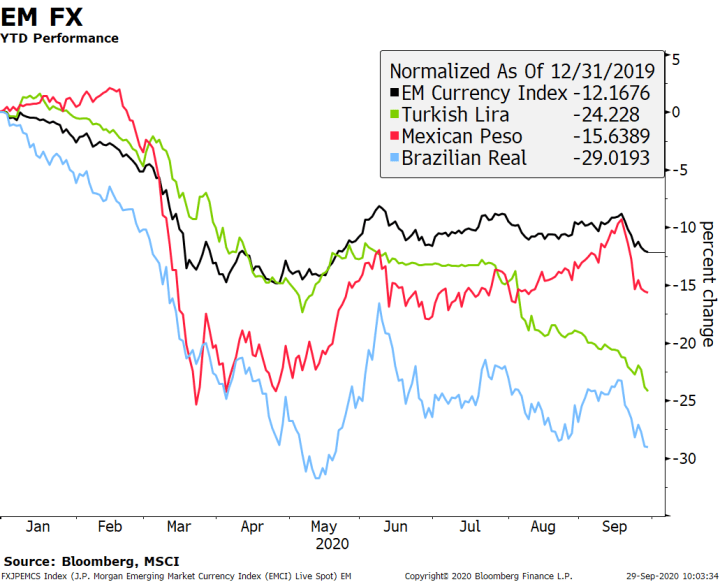

ASIA China reported strong money and loan data. Its rapidly expanding credit numbers are consistent with the solid recovery narrative we are getting from other data points. Aggregate financing beat expectations at RMB3.48 trln, roughly the same as the previous month, but new loans jumped to RMB1.9 trln from RMB1.28 trln. The numbers reinforce our view that the PBOC won’t enact any meaningful changes in the current policy stance as liquidity seems to ample enough for recovery to continue. Of course, external demand remains a potential downside risk, even though the latest trade figures were decidedly strong. Monetary Authority of Singapore kept policy unchanged, as expected. It provided dovish forward guidance, stating that “As core inflation is expected to stay low, MAS assesses that an accommodative policy stance will remain appropriate for some time.” It warned of a weak recovery and downside risks from still-challenging global demand, limited travel, a soft labor market, and ongoing public health concerns. Policymakers have signaled that fiscal policy will carry much of the load going forward. Q3 GDP was also reported and grew 35.4% SAAR vs. 33.5% expected and a revised -43.3% (was -42.9%) in Q2. |

EM FX YTD Performance, 2020 - Click to enlarge |

| The Bank of Korea left rates on hold at 0.5%, as expected. We think further monetary stimulus is unlikely unless we get a dramatic change in global landscape. The BOK expects GDP at -1.3% for this year, but the substantial fiscal effort will continue helping the economy move along as external demand picks up. Officials didn’t seem particularly concerned about the local bond market, suggesting ad-hoc purchases (or any more aggressive measures) are unlikely for now. The decision shouldn’t have any impact on asset prices. We expect appreciation pressure on the won to continue given the country’s favorable position for this part of the cycle. The currency is the best performing in the region over the last month (+3.2% against the dollar), but it’s still only 0.5% stronger year to date, underperforming the likes of TWD, PHP, and CNY. |

. |

You Might Also Like

Dollar Begins the Week Under Pressure Again

Dollar Begins the Week Under Pressure Again

The virus news stream remains negative; pressure on the dollar has resumed. The US economy is taking a step back just as Q3 is about to get under way; there are some minor US data reports today. UK Labour leader Starmer overtook Prime Minister Johnson in the latest opinion poll; Macron’s party did poorly in French local elections.

Dollar Bid as Market Sentiment Yet to Recover

Dollar Bid as Market Sentiment Yet to Recover

The US has started the formal process of withdrawing from the WHO; the dollar continues to benefit from risk-off sentiment but remains stuck in recent ranges. The White House is asking Congress to pass another $1 trln stimulus plan by early August; President Trump hosts Mexican President AMLO for a two-day visit.

Market Sentiment Dented by Weak Data and Rising US-China Tensions

Market Sentiment Dented by Weak Data and Rising US-China Tensions

Market sentiment has been dented by more than just rising virus numbers; yet the dollar continues to trade within recent well-worn ranges. California’s decision to reverse partial reopening will likely have a huge economic impact; June CPI may hold a bit more interest in usual; June budget statement is worth a quick mention.

Dollar Stabilizes but Further Losses Likely

Dollar Stabilizes but Further Losses Likely

The dollar is stabilizing today but further losses are likely. Senate Republicans have proposed a sharp cut to weekly unemployment benefits; Senator Collins will oppose Judy Shelton’s nomination to the Fed. Regional Fed manufacturing surveys for July will continue to roll out; early July reads for the US economy support our view that Q3 is off to a rocky start.

Dollar Bounce Ends Ahead of ECB Decision

Dollar Bounce Ends Ahead of ECB Decision

The dollar rally ran out of steam; US Senate will hold a vote today on its proposed “skinny” bill. US reports August PPI and weekly jobless claims; US will sell $23 bln of 30-year bonds today after a sloppy 10-year auction yesterday

BOC delivered a hawkish hold yesterday; Peru is expected to keep rates steady at 0.25%.

Dollar Soft as Markets Ignore Virus Numbers and Switch to Risk-On Mode

Dollar Soft as Markets Ignore Virus Numbers and Switch to Risk-On Mode

Virus numbers are rising across Europe and the US; the dollar is softening as risk-off sentiment ebbs. It is a fairly quiet day in the US; there is a glimmer of hope about a fiscal deal in the US; recent US data support the widely held view that more stimulus is needed.

Dollar Softens as Risk-Off Sentiment Ebbs

Dollar Softens as Risk-Off Sentiment Ebbs

The dollar continues to soften as risk-off sentiment ebbs; the first presidential debate will take place tonight. House Democrats have staked out their latest position at $2.2 trln; there is a fair amount of US data out today; Brazil has come under renewed pressure from fiscal concerns.

Dollar Softens and US Curve Steepens as Odds of Democratic Sweep Rise

Dollar Softens and US Curve Steepens as Odds of Democratic Sweep Rise

The dollar remains under pressure; the US curve continues to steepen; a compromise on fiscal stimulus before the election still seems unlikely; this is another quiet day in terms of US data. President Lagarde said the ECB is prepared to inject fresh monetary stimulus to support the recovery; we expect the ECB to increase its PEPP in Q4.

Tags: Articles,Daily News,Featured,newsletter