The eurozone economy is expected to collapse in 2020. In countries such as Spain and Italy, the decline, more than 9 percent, will likely be much larger than in emerging market economies. However, the key is to understand how and when the eurozone economies will recover. There are three reasons why we should be concerned: The eurozone was already in a severe slowdown in 2019. Despite massive fiscal and monetary stimulus, negative rates, and the European Central Bank’s (ECB) balance sheet above 40 percent of GDP, France and Italy showed stagnation in the fourth quarter and Germany narrowly escaped recession. The eurozone weakness had already started in 2017, and disappointing economic figures continued throughout the next years. Many governments blamed the weakness

Topics:

Daniel Lacalle considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The eurozone economy is expected to collapse in 2020. In countries such as Spain and Italy, the decline, more than 9 percent, will likely be much larger than in emerging market economies. However, the key is to understand how and when the eurozone economies will recover.

The eurozone economy is expected to collapse in 2020. In countries such as Spain and Italy, the decline, more than 9 percent, will likely be much larger than in emerging market economies. However, the key is to understand how and when the eurozone economies will recover.

There are three reasons why we should be concerned:

- The eurozone was already in a severe slowdown in 2019. Despite massive fiscal and monetary stimulus, negative rates, and the European Central Bank’s (ECB) balance sheet above 40 percent of GDP, France and Italy showed stagnation in the fourth quarter and Germany narrowly escaped recession. The eurozone weakness had already started in 2017, and disappointing economic figures continued throughout the next years. Many governments blamed the weakness on Brexit and trade war, but it was significantly more structural. The eurozone abandoned all structural reforms in 2014, when the ECB started its quantitative easing program (QE) and expanded its balance sheet to record levels. Manufacturing PMIs were already in contraction, government spending remained too high, and the elevated tax wedge weighed on growth and jobs. In 2019, almost 22 percent of the gross value added (GVA) to the eurozone GDP came from travel and leisure, a sector that unlikely to come back any time soon, while the exporting sector is also likely to suffer a prolonged weakness.

- The banking sector is still weak. In the eurozone, 80 percent of the real economy is financed via the banking channel (compared to less than 15 percent in the United States). Eurozone banks still have more than €600 billion in nonperforming loans (3.3 percent of total assets vs. 1 percent in the US), an almost unprofitable business with a poor return on tangible assets (ROTA) due to negative rates. This is a significant challenge ahead, as most of the growth investments may reduce capital strength significantly in the next months (this is true of Latin America in particular). Most of the eurozone governments are relying on leveraging the banks’ balance sheets in their “recovery plans.” A massive increase in loans, even with some form of state guarantee, is likely to cause significant strains on lending capacity and solvency in the next years, even with massive targeted longer-term refinancing operations (TLTROs) and capital requirement reductions.

- Most of the recovery plans go to government current spending, and tax increases will surely impact growth and jobs. The eurozone tax wedge on jobs and investment is already very high. According to the Paying Taxes 2019 report, the majority of eurozone economies show highly uncompetitive taxation levels. As most governments massively increase deficits to combat the COVID-19 crisis, there will be a high likelihood of massive tax increases that will make it more difficult to attract investment and jobs. Most of the recovery plans are also aimed at bailing out the past and letting the future die. There are massive bailout packages for traditional conglomerates and industries, but investment in technology and R&D (research and development) continues to have high burdens and no support. Considering that the eurozone was already in contraction in the middle of the massive Juncker plan (which mobilized more than €400 billion in investments) and the large green policies implemented, it is safe to say that relying on a Green Deal is unlikely to boost growth or reduce debt. The main problem of these large investment plans is that they are politically directed and as such have a large tendency to fail, as we saw with the Jobs and Growth Plan of 2009.

Almost 30 percent of the eurozone labor force is expected to be under some form of unemployment scheme, be it temporary, permanent, or self-employed cessation of activity. After a decade of recovery from the past crisis, the eurozone still had almost double the unemployment rate of its large peers, the US, and China. Germany may recover jobs fast, but France, Spain, and Italy, with important rigidities and tax burdens on job creation, may suffer high unemployment levels for longer.

The eurozone also faces important challenges in a recovery. The reality of having more flexible job markets and higher support for entrepreneurial activity in the form of attractive taxation will help China and the US recover faster. Considering the severity of the crisis, the eurozone is likely to need at least 10 percent of its GDP to rebuild the economy, but that figure is almost completely absorbed by the traditional sectors (airlines, autos, agriculture, tourism). Furthermore, the Green Deal initiative includes severe restrictions on travel and energy-intensive industries that may act as a brake on future growth.

The ECB policy of the past years was already unnecessarily expansionary, and now it has run out of tools to address the unprecedented challenge of recovery post-COVID-19. With negative rates, targeted liquidity programs, asset purchases of private and public debt, and a balance sheet that exceeds 42 percent of the eurozone’s GDP, the best it can do is disguise some of the risk, not eliminate it. We should also warn against adding massive monetary imbalances when demand for euros globally is acceptable but shrinking according to the Bank of International Settlements and the risk of redenomination remains in a politically unstable eurozone.

Our estimates show that, even with large fiscal and monetary stimulus, the eurozone economy will not recover its output and jobs until 2023. Debt rising to record highs as well as monetary imbalances due to a massive supply of euros in a diminishing demand environment may also cause significant problems for the stability of the eurozone.

The eurozone needs to understand that if it decides to increase taxes to address the rising debt due to the COVID-19 response, its ability to recover will be irreparably damaged.

Originally published at DLacalle.com.

You Might Also Like

The Fed Has Gone Nuts. And It Can Get Worse.

The Fed Has Gone Nuts. And It Can Get Worse.

With its $700 billion bond-buying expansion in response to the COVID crisis, the Federal Reserve has thrust itself into the limelight. Like a sixteen-year-old with a credit card, the Fed is salivating over what money-printing powers it shall seize next. How is the prudent investor to respond?

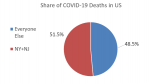

New York vs Texas: NY Has Nearly 50 Times More COVID-19 Deaths Per Capita

New York vs Texas: NY Has Nearly 50 Times More COVID-19 Deaths Per Capita

As of April 26, there were nearly 55,000 COVID-19 deaths reported in the United States. Of those, more than 22,000 (or about 40 percent) were in the state of New York alone. New Jersey was in second place, with nearly 5,900 COVID-19 deaths reported.

Dusty Wunderlich on FinTech Financing: Entrepreneurs Helping Entrepreneurs

Dusty Wunderlich on FinTech Financing: Entrepreneurs Helping Entrepreneurs

Key Takeaways and Actionable Insights. Consider these findings from a 2017 report from the G20 Global Partnership For Financial Inclusion, titled Alternative Data: Transforming SME Finance.

COVID-19 Is Teaching Us Decentralization Is Needed More Now Than Ever

COVID-19 Is Teaching Us Decentralization Is Needed More Now Than Ever

In the increasingly polarized America, Black Swan moments like the COVID-19 pandemic have further confirmed growing divides in the country. Our textbooks would like us to believe that emergencies create fertile grounds for unity. But when you have a populace that is politically dividing itself even when it comes to the TV shows it watches, there comes a point when we have to start recognizing that the prospect of national unity is becoming more of a mirage as the days go by.

Politicians Have Destroyed Markets and Ignored Human Rights with Alarming Enthusiasm

Politicians Have Destroyed Markets and Ignored Human Rights with Alarming Enthusiasm

An economic cataclysm has been unleashed upon the world by Western politicians and bureaucrats. Unbelievably, economic activity in the West has slowed to a creep, as entire populations have been confined to their homes for weeks, if not months. As a result, millions have had their lives turned upside down. Most entrepreneurs and self-employed persons have had their livelihoods jeopardized.

Money Creation – Not Low Interest Rates – Is Behind the Boom-Bust Cycle

Money Creation – Not Low Interest Rates – Is Behind the Boom-Bust Cycle

In a recent article entitled “Where Are All the Austrian Scholars’ Yachts?” John Tamny has criticized Austrian economists, and Mark Thornton in particular, for their skepticism regarding the relatively “ebullient stock market” in the midst of the pandemic. Mark Thornton responded to Tamny’s main argument in an earlier post. In this post, I will address two serious errors that underlie Tamny’s argument.

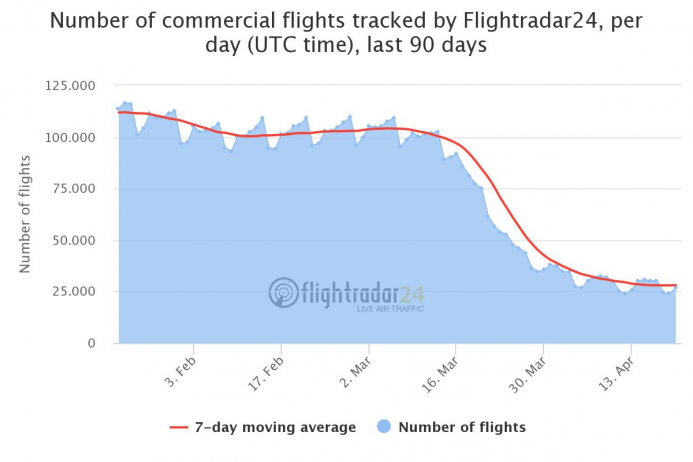

The Global Airline Industry Is in Even Worse Shape Than You Think

The Global Airline Industry Is in Even Worse Shape Than You Think

The economic impact of the COVID-19 pandemic has reached all productive sectors. The massive spread of the virus and social distancing measures have led to a dramatic decrease in economic activity. The aviation industry, vital for tourism and business, has been hit hard. Investors and analysts state that this crisis could be worse than the one that followed the SARS outbreak in 2003 and the one after 9/11.

Police Are Complicit in Politicians’ Disregard for the Rule of Law

Police Are Complicit in Politicians’ Disregard for the Rule of Law

People of a certain age might remember the old John Birch Society slogan "Support your local police!" The idea here is that your local policeman is a liberty-loving buddy of yours who would only ever support just laws and constitutional mandates. Only those bad guys in the FBI or BATF would ever consider violating your rights.

Now, obviously that has always been a rather naïve fantasy, but the notion certainly has a long history of support among American conservatives. The idea that unionized, well-paid government employees sympathize with the common man instead of with the government that signs the cops’ checks apparently has long made sense (for some reason) to conservatives and many others.

But thanks to the ongoing "state of emergency" and the fact that state governors, mayors, and

Tags: Featured,newsletter