George Dorgan

My articles My siteAbout meMy booksMy videos

Follow on:TwitterFacebookGoogle +

CFA SocietySeeking Alpha

The increasing volatility of SNB Earnings Annual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings. But the SNB may lose 50 billion in one year and win 60 billion in the next year or vice verse. Franc will rise again with crisis or inflation With a new financial crisis or a with a big rise of inflation, the run into the Swiss franc will start again. Deflationary period (e.g. Corona Crisis) During deflationary periods and recessions, the SNB will strongly intervene, similarly as she did in 2008/2009. During the Corona Crisis, the SNB intervened at 1.05 – 1.06 for a euro, in 2009 even for 1.50 These high intervention levels pave the way for later losses, which are the inflationary periods.

Topics:

George Dorgan considers the following as important: 1.) SNB Press Releases, 1) SNB and CHF, Featured, newsletter, SNB balance sheet, SNB equity holdings, SNB Gold Holdings, SNB profit, SNB results, SNB sight deposits, Swiss National Bank

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The increasing volatility of SNB EarningsAnnual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings. But the SNB may lose 50 billion in one year and win 60 billion in the next year or vice verse. Franc will rise again with crisis or inflationWith a new financial crisis or a with a big rise of inflation, the run into the Swiss franc will start again. Deflationary period (e.g. Corona Crisis)During deflationary periods and recessions, the SNB will strongly intervene, similarly as she did in 2008/2009. During the Corona Crisis, the SNB intervened at 1.05 – 1.06 for a euro, in 2009 even for 1.50 These high intervention levels pave the way for later losses, which are the inflationary periods.

|

|

Inflationary periodsDuring an inflationary period the

And this will lead to a massive SNB of at least 150 billion CHF. This is not a black swan, but a normal inflation scenario. We have seen a 60% rise of CHF in the 1970s; this was a black swan. In this case all assets except gold will fall. However, SNB’s gold share of 6% is too small to cushion this scenario. Some additional technical details: The crux, however, is

|

|

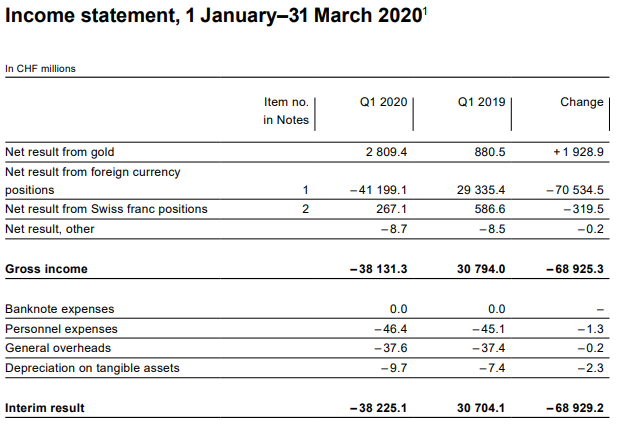

Some extracts from the official statement with annotations.

|

Income Statement for Q1 2020 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

SNB Asset Allocation and Expected ReturnMain insights:

A roughly calculated expected return should be around 2% as of Q1/2020.

This should be re-compensate for the on average 2% yearly increase of the Swiss franc. |

SNB Asset Allocation per 31.3.2020 (compared with Q4 2019)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

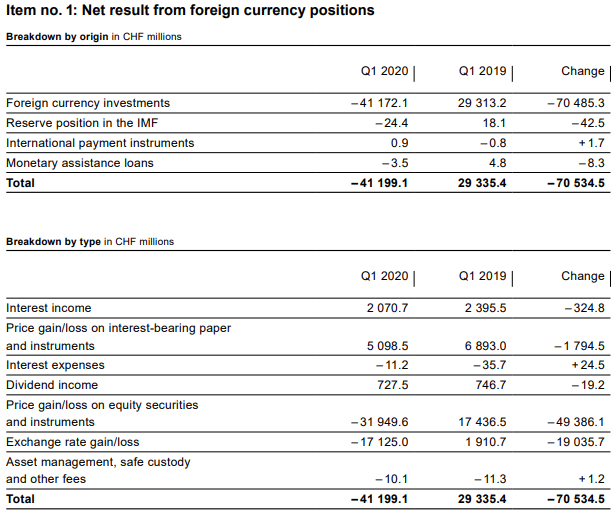

Loss on foreign currency positionsWe see the typical consequence of a recession

The following numbers are in billion Swiss Francs.

|

SNB Loss on Foreign Currencies Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

Valuation gain on gold holdingsA valuation gain of CHF 2.8 billion was recorded on gold holdings, which remained unchanged in volume terms. Gold was trading at CHF 49,923 per kilogram at the end of March 2020 (end 2019: CHF 47,222).

Percentage of gold to balance sheetThe percentage of gold has risen to 6.09% thanks to these rising prices.

Balance Sheet compared to GDP

|

SNB Balance Sheet for Gold Holdings for Q1 2020 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

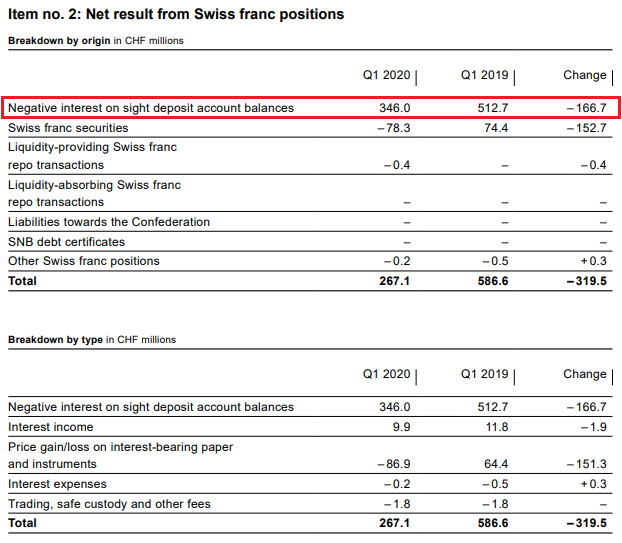

Profit on Swiss franc positionsThe SNB maintains its profitability, last but not least, thanks to the reduction of the profitability of banks. When too many funds arrive on their accounts, they must deposit them on their sight deposit account at the SNB.

Negative Interest ratesFurthermore, the SNB harms the Swiss economy, when it reduces the profits of Swiss banks by negative interest rates. But with this measure she maintains her own profitability. Still, as compared to the FX profits or gains on equities, this number is relatively low.

|

SNB Result for Swiss Franc Positions for Q1 2020 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

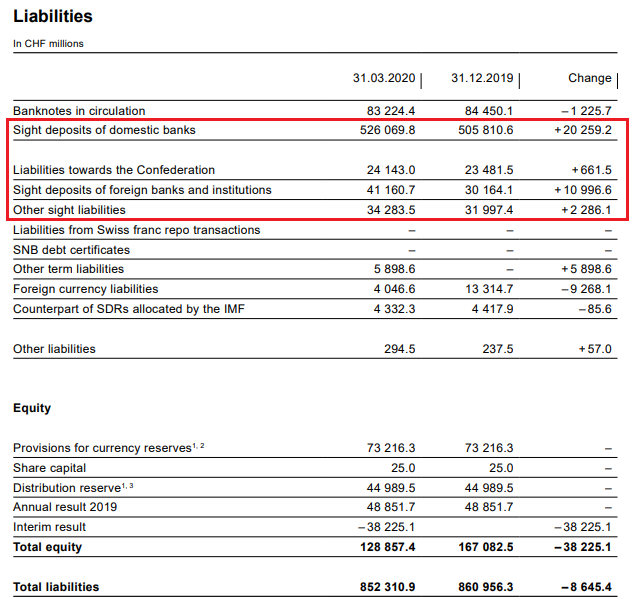

SNB LiabilitiesElectronic Money Printing: Sight Deposits Sight deposits are the biggest part of SNB interventions. In Q1 2020 the SNB intervened again, increasing sight deposits and its debt towards the Swiss state.

Paper PrintingBanknotes in circulation: -2.54 bn francs to 79.7 bn. CHF This old form of a printing press, today a less important form of central bank interventions. It showed that safe-haven Swiss francs, e.g. 1000 franc bank notes are currently less in demand than previously. |

SNB Liabilities and Sight Deposits for Q1 2020 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

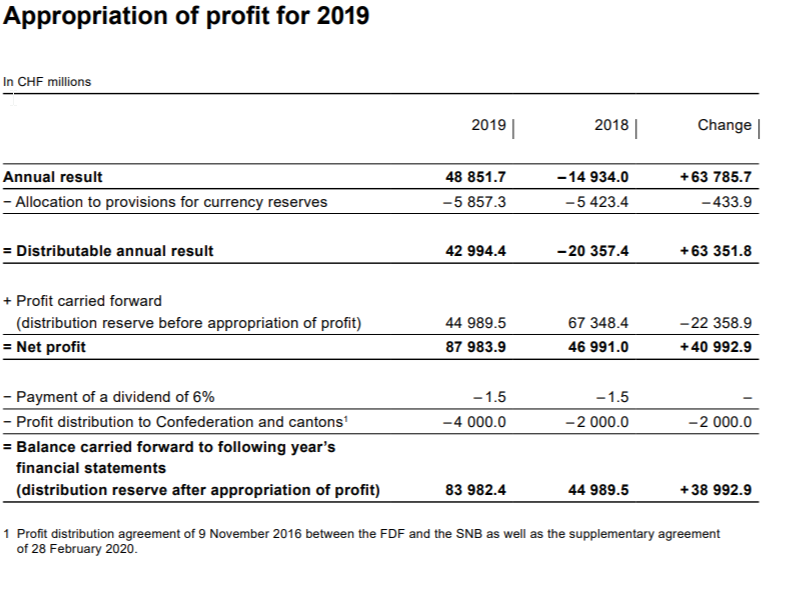

Provisions for currency reservesThe provisions for currency reserves cannot cover the potential loss 150 bn mentioned in the beginning for the inflation scenario. The SNB has only added the minimum of 8% of the result to these provisions. SNB’s Profit Game:

Then the SNB carries forward the profits of the previous years in form of a “distribution reserve”. The idea is to be able to pay a distribution/dividends even in bad years. Dividend yieldFor investors: The dividend yield is extremely low. Buying the SNB stocks is a bet on the stock price.

While the Swiss confederation and cantons, the SNB stock is a nice investment.

On the other side, they have a higher risk.

|

|

You Might Also Like

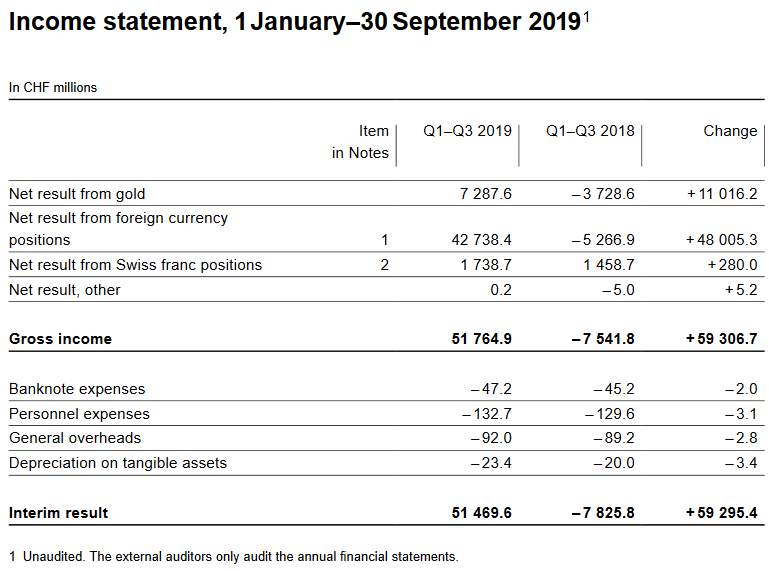

The Swiss National Bank reports a profit of CHF 51.5 billion for the first three quarters of 2019

The Swiss National Bank reports a profit of CHF 51.5 billion for the first three quarters of 2019

The Swiss National Bank reports a profit of CHF 51.5 billion for the first three quarters of 2019. The profit on foreign currency positions amounted to CHF 42.7 billion. A valuation gain of CHF 7.3 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 1.7 billion.

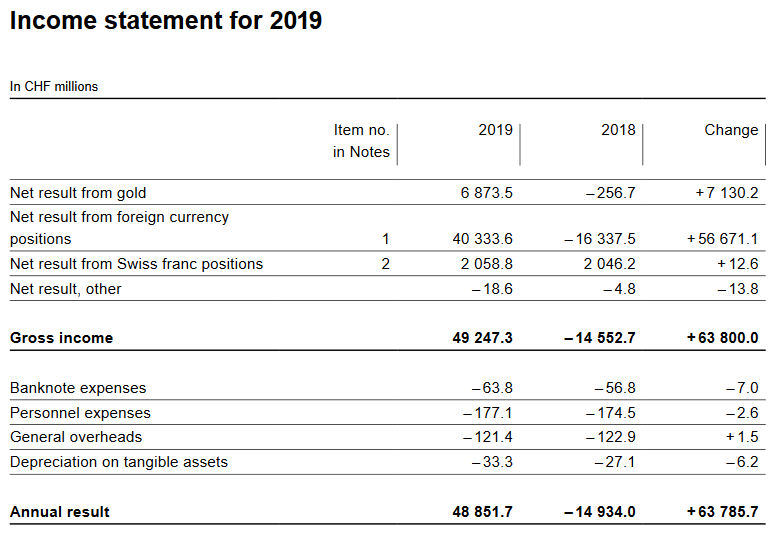

SNB Profit in 2019: 48.9 billion (2018: loss of CHF 14.9 billion, 2020 Does not Look Good)

SNB Profit in 2019: 48.9 billion (2018: loss of CHF 14.9 billion, 2020 Does not Look Good)

The increasing volatility of SNB Earnings Annual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings. But the SNB may lose 50 billion in one year and win 60 billion in the next year or vice verse. Good years of the Credit Cycle This trend was … Continue reading »

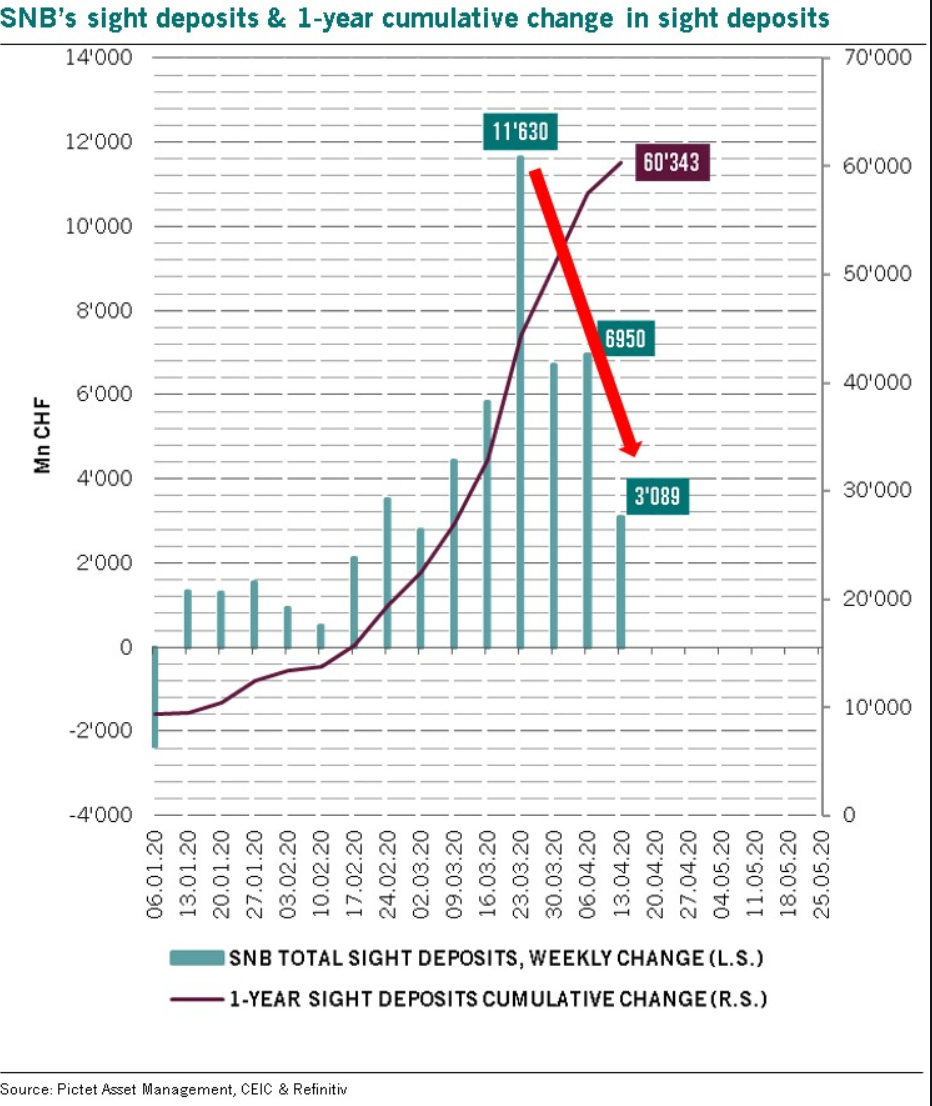

Weekly SNB Sight Deposits and Speculative Positions: Corona period

Weekly SNB Sight Deposits and Speculative Positions: Corona period

Update April 20, 2020: Corona panic Sight Deposits have risen by 3.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +3.1 bn. compared to last week.

The intervention point is between 1.05 and 1.0550 for EUR/CHF.

Central Banks Zoom In on CBDC

Central Banks Zoom In on CBDC

According to a BIS press release, several leading central banks collaborate with the BIS on matters relating to the introduction of CBDC: The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Sveriges Riksbank and the Swiss National Bank, together with the Bank for International Settlements (BIS), have created a group to share experiences as they assess the potential cases for central bank digital currency (CBDC) in their home jurisdictions.

Sollen Zentralbanken Klimapolitik betreiben?

Sollen Zentralbanken Klimapolitik betreiben?

Warum die Forderung nach einer klimafreundlichen Anlagepolitik schwierig bis gar nicht umzusetzen ist. Aufgrund ihrer extrem expansiven Geldpolitik sind sowohl die EZB als auch andere wichtige europäische Zentralbanken wie die SNB zu Grossinvestoren auf Anleihenmärkten und teilweise auch an Börsen geworden.

Ein rationaler Erklärungsansatz für negative Zinsen

Ein rationaler Erklärungsansatz für negative Zinsen

In einem Beitrag auf LinkedIn am 29. Dezember 2019 wirft Prof. Erwin Heri von der Universität Basel in die Runde, dass negative (Real-)Zinsen möglicherweise vernünftig sind. Sie wären das natürliche Ergebnis der Präferenzen der Wirtschaftssubjekte – und nicht primär das Ergebnis einer Manipulation von Zentralbanken.

Swiss National Bank to distribute 4 billion francs of profit

Swiss National Bank to distribute 4 billion francs of profit

In 2019, the Swiss National Bank (SNB) made a profit of around CHF 49 billion. These profits came mainly from the rising value of the assets on the bank’s balance sheet. In 2019, the value of its holdings of foreign currency and gold rose substantially. When combined with interest, dividend income and gains on shares total profits for the year were CHF 49 billion.

Switzerland Peps Up SMEs

Switzerland Peps Up SMEs

How Switzerland peps up SMEs: Banks are encouraged to extend credit (at 0%). The treasury guarantees the loans. The SNB refinances banks and accepts the guaranteed loans as collateral. Fast and efficient. Eventually, some of these loans will turn into grants of course. But that’s ok; the first-best response to a shock with asymmetric effects does involve transfers if markets are incomplete.

Tags: Featured,newsletter,SNB balance sheet,SNB equity holdings,SNB Gold Holdings,SNB profit,SNB results,SNB sight deposits,Swiss National Bank