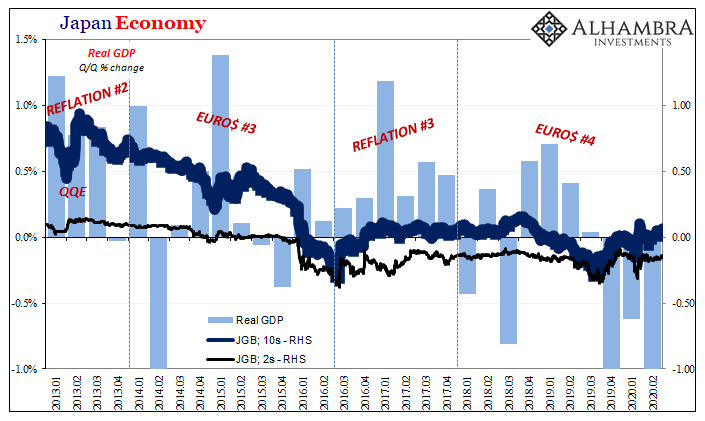

If we are going to see negative nominal Treasury rates, what would guide yields toward such a plunge? It seems like a recession is the ticket, the only way would have to be a major economic downturn. Since we’ve already experienced one in 2020, a big one no less, and are already on our way back up to recovery (some say), then have we seen the lows in rates? Not for nothing, every couple years when we do those (record low yields) that’s what “they” always say and yet they only ever go lower the next time. But what do we mean by “the next time?” Before getting into it, the central bank simply doesn’t factor. Japan Economy, 2013-2020 - Click to enlarge Monetary authorities possess no monetary abilities therefore they follow along with what bond markets are

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bond market, bonds, currencies, economy, Featured, Federal Reserve/Monetary Policy, german bunds, interest rate fallacy, Interest rates, Japan, JGB, Markets, negative interest rates, newsletter, QE, Recession, U.S. Treasuries, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| If we are going to see negative nominal Treasury rates, what would guide yields toward such a plunge? It seems like a recession is the ticket, the only way would have to be a major economic downturn. Since we’ve already experienced one in 2020, a big one no less, and are already on our way back up to recovery (some say), then have we seen the lows in rates?

Not for nothing, every couple years when we do those (record low yields) that’s what “they” always say and yet they only ever go lower the next time. But what do we mean by “the next time?” Before getting into it, the central bank simply doesn’t factor. |

Japan Economy, 2013-2020 - Click to enlarge |

| Monetary authorities possess no monetary abilities therefore they follow along with what bond markets are already doing. Sometimes that means lowering their benchmarks, like Jay Powell’s “unexpected” cuts last year, at other times it means yet another QE.

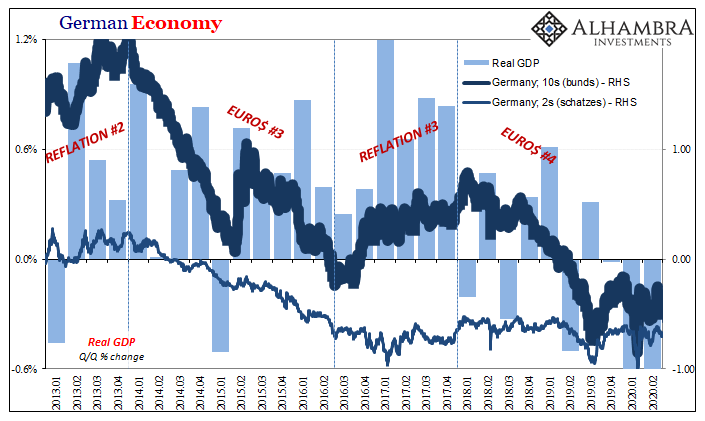

Continuously low rates are, interest rate fallacy, the product of QE’s many failures rather than QE’s bond buying itself. Using the two primary examples of negative yields, Japan and Germany, it’s pretty clear what it is that steers the bond market. It’s a word that starts with “euro” and ends with “dollar.” |

German Economy, 2013-2020 - Click to enlarge |

| In 2015-16, for example, during Euro$ #3 there wasn’t recession in either Japan or Germany. There were rising risks for one in both places, sure, but the resulting global downturn which did produce recessions in other locations is ultimately what pushed rates all the way to zero with each long end for a time dropping into the minuses.

But, and this is the important part, it was the lack of altitude, the direct product of these persistent monetary problems as described by lackluster reflation (as distinct from real recovery), which is why when the world moved into Euro$ #4 zero nominals were so easily reachable for so many parts of each curve. |

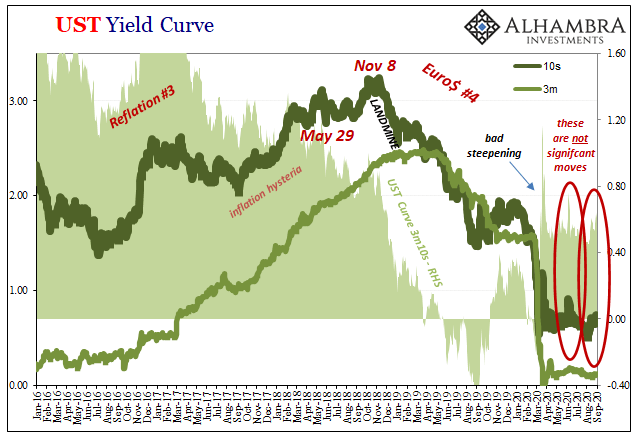

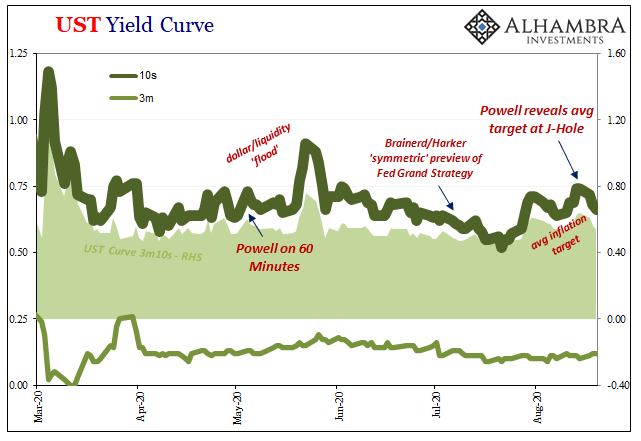

UST Yield Curve, 2003-2020 - Click to enlarge |

In other words, not recession precisely but lack of recovery in between downturns of whatever ultimate size. That’s why yields turned negative in these key sovereign markets when they did (and why they were nearly simultaneous in doing so). Rising liquidity risks combined with little to no prospects for meaningful economic growth to offset them (recession or not) resulted in this situation people struggle to understand.

Even Economists have figured this out – sort of. They get the result without being able to figure out the cause. When they talk or write about low perhaps negative R* what they are saying is just what I said. The only difference is in assigning the blame for it; the R* people believe the problem is you and me rather than incompetent policymakers. |

|

| Funny how it is those incompetent policymakers who have come up with this R* theory conveniently shifting the blame elsewhere – especially since any real evidence, including bond market behavior, literally, in this case, falls so perfectly and uncomfortably against them.

Getting back to the US Treasury market, then, we don’t necessarily need re-recession in 2020 or early 2021 for the “impossible” to happen in it. After thirteen years of one “impossible” event after another, all it would take would be, essentially, for nothing to meaningfully change. Just more of the same; the interest rate fallacy. Continued liquidity risk plus lack of recovery/growth. And that seems to be the way the final few months of this year might be shaping up. Another recession not required because, when you look at the whole, we never really left the first one. |

UST Yield Curve, 2016-2020 - Click to enlarge |

You Might Also Like

From QE to Eternity: The Backdoor Yield Caps

From QE to Eternity: The Backdoor Yield Caps

So, you’re convinced that low rates are powerful stimulus. You believe, like any good standing Economist, that reduced interest costs can only lead to more credit across-the-board. That with more credit will emerge more economic activity and, better, activity of the inflationary variety. A recovery, in other words. Ceteris paribus. What happens, however, if you also believe you’ve been responsible for bringing rates down all across the curve…and then no recovery.

There Was Never A Need To Translate ‘Weimar’ Into Japanese

There Was Never A Need To Translate ‘Weimar’ Into Japanese

After years of futility, he was sure of the answer. The Bank of Japan had spent the better part of the roaring nineties fighting against itself as much as the bubble which had burst at the outset of the decade. Letting fiscal authorities rule the day, Japan’s central bank had largely sat back introducing what it said was stimulus in the form of lower and lower rates.No, stupid, declared Milton Friedman.

Accusing the Accused of Excusing the Mountain of Evidence

Accusing the Accused of Excusing the Mountain of Evidence

Why not let the accused also sit in the jury box? The answer seems rather obvious. While maybe the truly honest man accused of a crime he did commit would vote for his own conviction, the world seems a bit short on supply of those while long and deep offering up practitioners of pure sophistry in their stead.

Powell Would Ask For His Money Back, If The Fed Did Money

Powell Would Ask For His Money Back, If The Fed Did Money

Since the unnecessary destruction brought about by GFC2 in March 2020, there have been two detectable, short run trendline upward moves in nominal Treasury yields. Both were predictably classified across the entire financial media as the guaranteed first steps toward the “inevitable” BOND ROUT!!!!

So Much Bond Bull

So Much Bond Bull

Count me among the bond vigilantes. On the issue of supply I yield (pun intended) to no one. The US government is the brokest entity humanity has ever conceived – and that was before March 2020. There will be a time, if nothing is done, where this will matter a great deal.That time isn’t today nor is it tomorrow or anytime soon because it’s the demand side which is so confusing and misdirected.

Science of Sentiment: Zooming Expectations Wonder

Science of Sentiment: Zooming Expectations Wonder

It had been an unusually heated gathering, one marked by temper tantrums and often publicly expressed rancor. Slamming tables, undiplomatic rudeness. Europe’s leaders had been brought together by the uncomfortable even dangerous fact that the economic dislocation they’ve put their countries through is going to sustain enormously negative pressures all throughout them. What would a “united” European system do to try and fill in this massive hole?The marathon bargaining session began on an ominously hot Friday in late July with birthday celebrations and was expected to breezily wrap up by the following Sunday. By the Monday morning, however, the gloves had come off and high-level talks were often replaced by mid-level staff meetings to hammer out details the bosses, apparently, could no

Not This Again: Too Many Treasuries?

Not This Again: Too Many Treasuries?

Tomorrow, the Treasury Department is going to announce the results of its latest bond auction. A truly massive one, $47 billion are being offered of CAH4’s notes dated August 31, 2020, maturing out in August 31, 2027. In other words, the belly of the belly, the 7s.We’ve already seen them drop for two note auctions this week, both equally sizable.

Fama 2: No Inflation For Old Central Banks

Fama 2: No Inflation For Old Central Banks

The Bureau of Labor Statistics reported that the core CPI in July 2020 jumped by the most (+0.62%) in almost thirty years. After having dropped month-over-month for three months in a row for the first time in its history, it has posted back to back gains the latest of which pushing the index back above its February level.

Tags: bond market,Bonds,currencies,economy,Featured,Federal Reserve/Monetary Policy,german bunds,interest rate fallacy,Interest rates,Japan,JGB,Markets,negative interest rates,newsletter,QE,recession,U.S. Treasuries,Yield Curve