Last month’s downdraft in equities spooked investors. The fear that is often expressed is that the end of the business cycle may coincide with the end of a credit cycle and a return to 2008-2009 crisis. It seems like an increasing number of economists agree with the sentiment expressed by President Trump that the Fed is too aggressive. Of course, they do not think the president should comment on Fed policy, but they generally concur with the assessment. To be sure, we continue to track data that points to late-cycle activity, like weakness in interest rate sensitive sectors, such as housing. The 12-month average non-farm payrolls peak in the middle of a cycle and the peak was recorded in 2015, even though job growth

Topics:

Marc Chandler considers the following as important: 4) FX Trends, China, Featured, Federal Reserve, newsletter, SPX, trade

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Last month’s downdraft in equities spooked investors. The fear that is often expressed is that the end of the business cycle may coincide with the end of a credit cycle and a return to 2008-2009 crisis. It seems like an increasing number of economists agree with the sentiment expressed by President Trump that the Fed is too aggressive. Of course, they do not think the president should comment on Fed policy, but they generally concur with the assessment.

To be sure, we continue to track data that points to late-cycle activity, like weakness in interest rate sensitive sectors, such as housing. The 12-month average non-farm payrolls peak in the middle of a cycle and the peak was recorded in 2015, even though job growth remains robust. The flattening of the yield curve typically happens late in a cycle.

However, it is difficult to imagine a much better economic news stream than the US has reported recently. The economy was stronger than expected in Q3 (3.5%) on the heels of 4.2% growth in Q2. Auto sales in October were stronger than expected. The employment report was solid. Not only did job growth surprises on the upside (250k) but average hourly earnings rose 3.1% from a year ago, which is the most since April 2009. The underemployment rate ticked down.

This week is the last of the non-live FOMC meetings, which means that every meeting after November 8 will be followed by a press conference. This has long been due. Since the first hike in December 2015, the Fed only has hiked at meetings with a press conference, which takes place at the quarterly meetings. The reduces the Fed’s freedom of movement and allows speculators to game the market. More frequent press conferences do not mean an acceleration of hikes. The precise timing of the gradual move does become a little less predictable. There is something to be said for strategic ambiguity.

No one expects a hike this week, but an increase next month is highly probable. The CME model points to a nearly 80% chance of a hike in December having been discounted. There is much speculation about the Fed’s statement. Some look the Fed to address topics like the pressure on the effective Fed funds rate, which is now at the rate paid on reserves (2.20%), and maybe slow the balance sheet unwind, which some think is a significant cause.

This all seems too fanciful and may misunderstand the purpose of the statement. If anything, the economic data have been stronger than the Fed expected. By all reckoning, the economy is growing faster than trend with the help of a large deficit and debt burden. The 15% drop in oil prices over the past five weeks may reduce a headwind. The statement is likely to be succinct, and important will say nothing to dissuade expectations for a December hike and more hikes in 2019. There seems to be little to no chance of dovish hold.

United StatesIn fact, a dovish hold, where the Fed signaled any kind of course moderation, would be destabilizing. It would confuse investors and begs the question of what the Fed knows the market doesn’t. This could weigh on equities, though utilities and interest-rate sensitive sectors could outperform. The dollar would likely spike lower, and the yield curve may steepen. Those sectors, companies, and investment strategies that have been squeezed by the nearly doubling of three-month LIBOR over the past year to 2.70% could see quick relief. Equities turned higher last week, and the apparent spark was the comment by President Trump giving an optimistic spin on trade talks with China, which Kudlow, his senior economic adviser, had a few days before bemoaned the lack of PRC engagement on the US trade concerns. The MSCI Emerging Markets Index rallied 6%, Japan’s Nikkei rose, while the S&P 500 and the Dow Jones Stoxx 600 advanced a more modest 2.4%. The rally in equities so directly linked to the possibility that a trade war between the two largest economies can be averted offers a prima facie that the decline in the stocks may be more complicated than can simply be laid at the Fed’s feet. However, the S&P 500’s recovery stalled ahead of the weekend as yields also rose sharply after the jobs and average hourly earnings data. Two levels that may act as pivots for the S&P 500. The first is the 200-day moving average. It starts the week near 2764.6. It peaked about a third of one percent shy of that average. On the downside is the gap created by the sharply higher opening last Wednesday. The bottom of the gap, then, is last Tuesday’s high, which is found near 2685.5. |

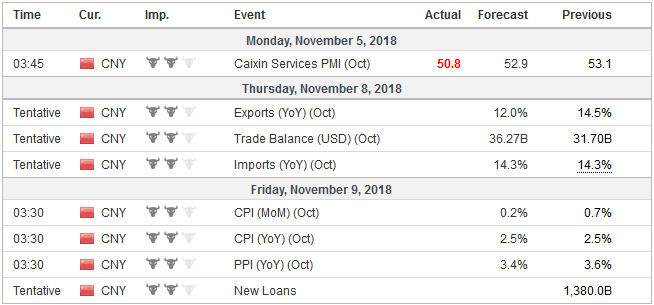

Economic Events: United States, Week November 05 - Click to enlarge |

ChinaPerhaps due to scar tissue from August 2015, Chinese stocks are often seen as a (potential) bellwether. Chinese officials want to push a different policy level to support the economy than debt. It appears to be settling on tax cuts (income, and some sales tax, such as on autos). The Shanghai Composite finished last week (~2676) at its best level since October 10. It gapped lower on October 11. The gap was entered but not closed. The top of it is about 2703. China faces both domestic and foreign challenges. A resolution of the trade conflict would be helpful. The fact of the matter is that belief that China has taken advantage of the United States is one of the few bipartisan views amid a very polarized electorate. The difference following the elections in which Democrats achieve a majority in the House of Representative might not be much of a change in policy as in the process and curbs on some executive action (e.g., ZTE). How likely is a near-term US-China trade agreement or even the beginning of a de-escalation? We think not very. First, the idea that many Americans are pinning their hopes on is that China will capitulate under the crippling pressure. This seems to be a self-serving exaggeration. A loss of all exports to the US would cost China roughly $550 bln on its approximately $12 trillion economy. This is a little less than 5%. It is a blow, but it is not insurmountable, and the income tax cuts are a modest down payment. China has already offered to by more US goods including agriculture and energy. Many economists criticize managed trade but do not have much objection to China’s proposals in spirit. It is the same with the currency. Markets should determine foreign exchange levels, but Chinese intervention is agreeable if it stops the yuan from falling. We suspect if market forces were allowed full sway, the yuan would likely decline and by more than it has. By IMF models, the yuan is close to fair value. Given that the dollar is stronger against nearly all the currencies means that one does not need a special explanation of the yuan’s decline (such as intervention or efforts use the exchange rate to offset the tariffs). Moreover, China’s economy is slowing, and the central bank is easing financial conditions. In contrast, the Fed is hiking and the economy by nearly any metric is strong. |

Economic Events: China, Week November 05 - Click to enlarge |

Switzerland |

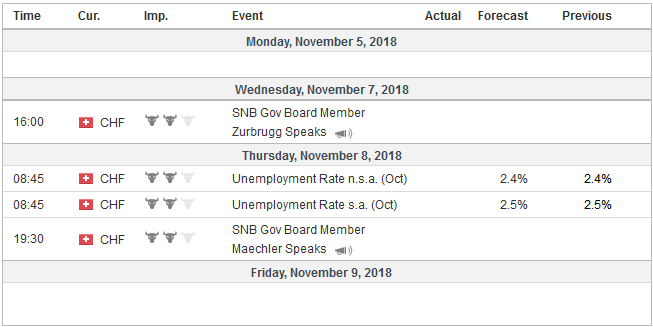

Economic Events: Switzerland, Week November 05 - Click to enlarge |

Trump’s comments about good talks with Xi, especially on trade were undermined by Kudlow the next day. Why would the President fan such hopes then? Two motivations have been attributed to him: Election considerations and/or concern about the stock market, which Trump had previously used a litmus test of his presidency. At the same time, Trump’s record suggests he is willing to accept minor concessions and give his stamp of approval, ostensibly turning what he has claimed were horrible agreements into the best ever.Polls show that the most likely scenario is for the Democrats to secure a narrow majority in the House of Representatives and the Republicans to hold on to the Senate. A critical wild card is the turnout. Early voting has been particularly robust. For example, more people have voted early in Texas than voted in the 2014 mid-term election.

Mid-term elections typically see the party that controls the executive branch to lose seats, and the Democrat voters seem particularly energized. However, Trump’s emphasis on immigration and “caravan” 1000 miles away and the deployment of troops to the border appear designed to fire up his base. Some late polls suggest it may be having the desired effect. While the particulars may change, the broad policy mix of tighter monetary policy and looser fiscal policy in the US will likely persist.

Tags: China,Featured,Federal Reserve,newsletter,SPX,Trade