Summary: EMU preliminary August CPI headline rise may not translate into core. US jobs growth is fine; earnings growth is key. Trump’s coalition is fraying, and the weekend pardon will not help mend fences. The US dollar’s consolidation ended with an exclamation point last week. The downtrend since the beginning of the year is resuming, and there is a reasonable risk that the pace accelerates. In addition to the echoesand implications of last week’s developments, there are two data highlights: The US monthly jobs report and the flash CPI estimate for theeurozone. Eurozone The data are straightforward, so let’s look at them first. The eurozone CPI will be released on August 31. Before it is released, a few

Topics:

Marc Chandler considers the following as important: EUR, Featured, FX Trends, newsletter, Politics, USD

This could be interesting, too:

Investec writes The Swiss houses that must be demolished

Claudio Grass writes The Case Against Fordism

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Summary:

EMU preliminary August CPI headline rise may not translate into core.

US jobs growth is fine; earnings growth is key.

Trump’s coalition is fraying, and the weekend pardon will not help mend fences.

The US dollar’s consolidation ended with an exclamation point last week. The downtrend since the beginning of the year is resuming, and there is a reasonable risk that the pace accelerates. In addition to the echoesand implications of last week’s developments, there are two data highlights: The US monthly jobs report and the flash CPI estimate for theeurozone.

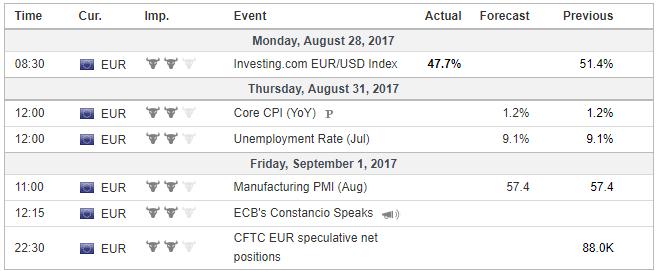

EurozoneThe data are straightforward, so let’s look at them first. The eurozone CPI will be released on August 31. Before it is released, a few countries will also report their national figures, including Germany. The national reports allow economists to fine tune their forecasts. In any event, little change is expected from the pace seen in July. Specifically, most economists expect a tick up in the headline rate to 1.4% from 1.3% (peaked at 2% in February), while the core rate is likely to remain flat at 1.2%. There can be no reasonable doubt that Draghi and an overwhelming majority at the ECB believe that inflation has still not reached a self-sustaining path toward the target. Therefore the asset purchase program will be extended. However, the downside risks to growth (recession) and prices (deflation) have been markedly reduced, and this allows for a reduced pace of purchases. Reports before the weekend that the ECB would vote in October on stopping asset purchases strikes us a wide of the mark. Leaving aside the significance of the vote, the ECB has liked to announce policy changes with the cover of new staff forecasts. These will be available in September. Just as importantly, the claim seems to misunderstand the decision-making process. Given the widely agreed upon recognition of the need to taper with than a hard stop, the idea that the ECB would decide to stop purchases is not very realistic. Moreover, there is no need to make a decision when to stop purchases. Instead, the two pressing issues are the amount to purchase and for how long. When we tried gaming it out, we suggest a 50% reduction to 30 bln euro a month for six months could produce a large consensus. The 50% reduction would appeal to the creditors as it is a bigger step that last year. It would also allow a cut of the same euro amount (30 bln) to allow a full stop at mid-year if desired. The creditors may push for a three-month extension, and it is possible that it carries the day, but in terms of communication and managing expectations, we suspect the six-month extension has more to recommend itself. |

Economic Events : Eurozone, Wekk August 28 - Click to enlarge |

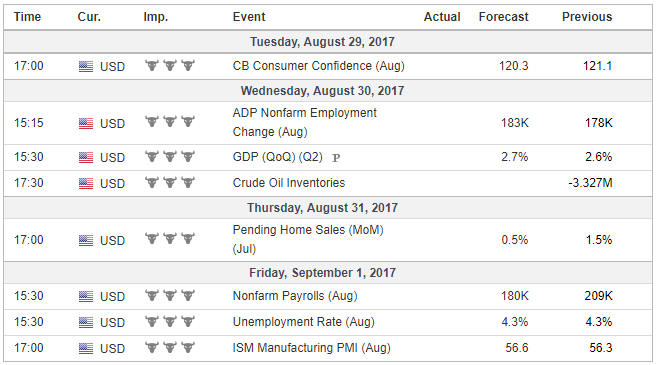

United StatesIn the US, the August jobs report, the day after the eurozone’s CPI, will be the main talking point. The headline non-farm payroll number that is the focus is less important now, barring a significant surprise. Jobs growth has been notable steady. In 2016, the US created 187k jobs a month on average. This year the average is 184k. In the past three months, US job growth accelerated a bit (average 195k), and a reversion to the mean, which is what the median forecast anticipate (180k) is neither here nor there. The point is that job growth remains impressive given the maturity of the business cycle. The unemployment rate returned to the cyclical low of 4.3% in July, and likely remained there in August. The underemployment rate (U6) has become of greater interest in this cycle than in previous cycles. It has fallen to 8.6% from 9.2% at the end of last year and 9.7% last July. There is scope for additional improvement. It averaged 8.2% in 2006. Earnings growth has also commanded more attention as a measure of the tightness of the labor market, potential pressure on prices, and an indicator of the fuel for effective demand. Average hourly earnings growth has also been remarkably steady. Although it stood at 2.5% year-over-year in July, three-month, 12- and 24-month averages stand at 2.6%. A rise to 2.6% in August as the median forecast expects is better than a decline but tells investors little new about the economy. Given the importance of prices for the Fed’s reaction function, the core PCE deflator that is reported the day before the employment data has potential to impact the interest rates and the dollar. The risk is that the core PCE deflator, which the FOMC targets, slipped to 1.4% from 1.5%. This would be the lowest since the end of 2015. Some would see it as reducing the chances for another rate hike before the end of the year. The dollar fell sharply at the end of last week. A fair hearing of both Yellen and Draghi’s speeches at Jackson Hole shows neither addressed near-term monetary policy. The December Fed Funds futures contract was unchanged before the weekend and for the week as a whole. Bloomberg’s model suggests a 34.7% chance of a hike by the end of the year is discounted. In the CME’s assessment, the market has priced in a 40% chance. Our calculation, which assumes no chance of a hike September or November, put it at a 38% probability. |

Economic Events: United States, Week August 28 - Click to enlarge |

Switzerland |

Economic Events, Switzerland, Week August 28 - Click to enlarge |

The fact that the neither Yellen or Draghi addressed monetary policy means that the information set of investors did not change. The status quo persists. The status quo is dollar negative. The status quo, in the consensus narrative, is that the ECB is about to take another step toward the exit, supported by a strengthening economy. The status quo includes doubts about whether the Fed can raise interest rates again this year, or under Yellen’s leadership.

Could a newly appointed chair lift rates early in their tenure if they were selected knowing the White House’s preferences? Inflation expectations would rise, but isn’t that partly what officials desire? The 10-year breakeven fell from just below 2.0% at the end of last year to 1.75% now. It had fallen to 1.67% in the middle of June, the recovery stalled earlier this month. The persistence of the status quo could see the 10-year breakeven fall to new lows, which would be consistent with the continued unwinding of the so-called Trump Trade, and the 10-year yield falling further.

Presidential pardons are rarely the stuff for macroeconomic and foreign exchange analysis, but this time is different because the context is different. The context is that Trump’s handling of the recent white nationalist-inspired violence that seemed to suggest a moral equivalency estranged the business wing of his coalition. Several such advisory panels imploded with resignations. Others have been shuttered. The pardon was for the controversial Sheriff Arpaio, who was convicted for his cruel treatment of immigrants.

Then, on a different front, in a strongly worded letter, nearly a dozen business leaders threatened to withdraw support for the President in renegotiating NAFTA, if the trade tribunals, which the Trump Administration has argued undermines US sovereignty, are abandoned. At the same time, several of the departures from the White House have jettisoned the personnel link between the Trump Administration and the Republican Party. The weakening support from the business community and increasing strained relationship between the administration and the Republican Party does not bode well for the policy outlook or the investment climate.

The pardon may bolster Trump’s base, but the challenge now is to increase it to govern. The pardon will not help Trump mend any fences or strengthen is negotiating position. His economic adviser and Director of the National Economic Council publicly was critical of Trump’s handling of the past couple of weeks. Cohn appeared to have considered resigning but thought his duty was to serve but expected an improvement. The pardon throws fresh gas on the fire.

At the same time the main strategy of tax reform has changed. Although in the high frequency news cycle it is easy to drop off the radar screen, but rather than provide a detailed tax reform plan, as has been promised would be delivered shortly, the White House is withdrawing from the process. Recall that the process was a group of six high placed officials, Mnuchin and Cohn representing the Administration, and top Republicans in the House and Senate (Ryan and McConnell) and the two key Republicans for writing the bill (Brady and Hatch). Before the weekend, it was announced that in essence Mnuchin and Cohn would not be participating.

At the same time that President Trump is more critical of the Republican leaders, he pulls back from shaping his signature initiative. It would seem to suggest a lack of confidence in success, and it will allow the President to campaign against the “do nothing” Congress in the primaries early next year. Last week, Trump threatened to allow the government to shut down unless Congress authorizes money for the Wall with Mexico. Last week’s developments would seem to undermine rather than strengthen the likelihood of tax reform, and a smooth increase in the debt ceiling (or face potentially missing a debt payment) and new spending authorization (without which parts of the federal government would close). A close call in 2011 led to the S&P’s decision to take away its AAA rating.

Tags: #USD,$EUR,Featured,newsletter,Politics