Jeffrey P. Snider

May 30, 2019

SNB & CHF

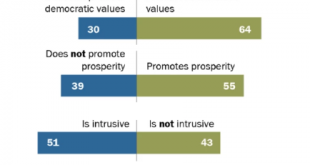

In May 2018, the European Parliament found that it was incredibly popular. Commissioning what it calls the Eurobarameter survey, the EU’s governing body said that two-thirds of Europeans inside the bloc believed that membership had benefited their own countries. It was the highest showing since 1983.

Voters in May 2019 don’t appear to have agreed with last year’s survey. For the first time since 1979, Social Democrats...

Read More »

Marc Chandler

April 1, 2019

SNB & CHF

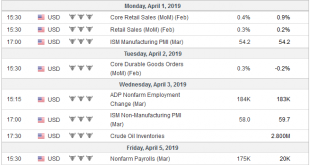

Investors have worked themselves into a lather. Equities crashed in Q4 last year amid on corporate earnings and concerns about growth. The Fed’s tightening decision in December was made unanimously. The above-trend growth, the preferred inflation measure was near target, unemployment was the lowest in a generation and real rates were historically low.

There are myths in the market, like the Plunge Protection Committee,...

Read More »

Marc Chandler

March 25, 2019

SNB & CHF

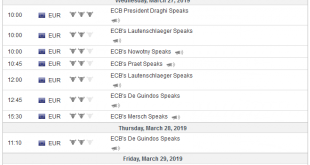

The combination of the dovish hold by the Federal Reserve and the eurozone’s miserable flash Purchasing Managers Index casts a pall over the economic outlook. Japan’s flash PMI remained stuck at February’s 48.9, while core inflation unexpectedly eased. Three months after the European Central Bank stopped buying bonds, the German 10-year Bund yield fell below zero for the first time since 2016. Japan’s 10-year yield is...

Read More »

Jeffrey P. Snider

February 24, 2019

SNB & CHF

It infects every boardroom across the world. Big business requires decent forecasting, yet time and again it seems they are deprived of what they desperately need. Instead, even after this last decade, the world’s largest companies continue to be surprised by weakness that is far more prevalent than strength.

It has been the one constant. Central bankers declare their policies successful, ignoring mountains of...

Read More »

Marc Chandler

February 13, 2019

SNB & CHF

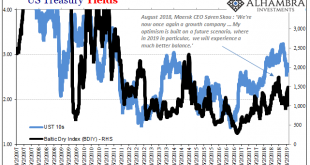

Swiss Franc

The Euro has fallen by 0.25% at 1.1367

EUR/CHF and USD/CHF, February 13(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge

FX Rates

The Federal Reserve has long been clear on the sequence of events as it innovated the playbook during the Great Financial Crisis. There would be a considerable period between when the Fed would finish its credit easing operations that...

Read More »

Jeffrey P. Snider

February 3, 2019

SNB & CHF

Men have long dreamed of optimal outcomes. There has to be a better way, a person will say every generation. Freedom is far too messy and unpredictable. Everybody hates the fat tails, unless and until they realize it is outlier outcomes that actually mark progress.

The idea was born in the eighties that Economics had become sufficiently advanced that the business cycle was no longer a valid assumption. The mantra,...

Read More »

Joseph Y. Calhoun

January 27, 2019

SNB & CHF

A Return To Normalcy

In the first two years after a newly elected President takes office he enacts a major tax cut that primarily benefits the wealthy and significantly raises tariffs on imports. His foreign policy is erratic but generally pulls the country back from foreign commitments. He also works to reduce immigration and roll back regulations enacted by his predecessor. This President is widely rumored to have...

Read More »

Joseph Y. Calhoun

January 8, 2019

SNB & CHF

The secret of health for both mind and body is not to mourn for the past, nor to worry about the future, but to live in the present moment wisely and earnestly.

Buddha

Review

It’s that time of year again, time to cast the runes, consult the iChing, shake the Magic Eight Ball and read the tea leaves. What will happen in 2019? Will it be as bad as 2018 when positive returns were hard to come by, as rare as affordable...

Read More »

Jeffrey P. Snider

January 4, 2019

SNB & CHF

It was only near the quarter end, that’s what made it so unnerving. We may have become used to these calendar bottlenecks over the years, but they still remind us what they are. Late October 2012 was a little different, though. On October 29, the GC repo rate for UST collateral (DTCC) surged to 52.6 bps. The money market floor, so to speak, was zero at the time and IOER (the joke) 25 bps.

We also have to keep in mind...

Read More »

Joseph Y. Calhoun

November 30, 2018

SNB & CHF

Is the Fed’s monetary tightening about over? Maybe, maybe not but there does seem to be some disagreement between Jerome Powell and his Vice Chair, Richard Clarida. Powell said just a little over a month ago that the Fed Funds rate was still “a long way from neutral” and that the Fed may ultimately need to go past neutral. Clarida last week said the FF rate was close to neutral and that future hikes should be “data...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org