It’s not just the flood of never-ending inventory. That’s a huge and growing problem, sure, as the chickens of last year’s short-termism overordering finally come home to their retailer roost. Being stuck with too many goods isn’t necessarily fatal to the global and domestic manufacturing sectors. The scale of the burden is one key worry, though equally so is demand. When the orders were placed during last year, companies appear to have fully bought into (literally) the permanent plateau of fiscal prosperity brought about by repeated war-scale government interventions. They never questioned the current nor future state of the American consumer, laser-focused instead on supply problems exclusively. I wrote all the way back last September, just as Euro$ #5 was

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, demand, economy, Featured, Federal Reserve/Monetary Policy, Inventory, inventory cycle, manufacturing, Markets, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

It’s not just the flood of never-ending inventory. That’s a huge and growing problem, sure, as the chickens of last year’s short-termism overordering finally come home to their retailer roost. Being stuck with too many goods isn’t necessarily fatal to the global and domestic manufacturing sectors.

The scale of the burden is one key worry, though equally so is demand. When the orders were placed during last year, companies appear to have fully bought into (literally) the permanent plateau of fiscal prosperity brought about by repeated war-scale government interventions. They never questioned the current nor future state of the American consumer, laser-focused instead on supply problems exclusively.

I wrote all the way back last September, just as Euro$ #5 was turning up the deflationary probabilities worldwide:

How’s it going for consumer demand now that we’ve reached “at some point?” Well, not good. Seriously, not good.

Tapped out customers when inventories levels and flows are at historic highs. That’s not inflationary, rather the opposite – as we see in more and more places by the week. |

. |

| We’ll get advance inventory estimates tomorrow morning for the month of May. They’re already expected to be stout, closer to recent ridiculous highs than even normal highs; and recent estimates have been revised yet higher after more complete data comes in.

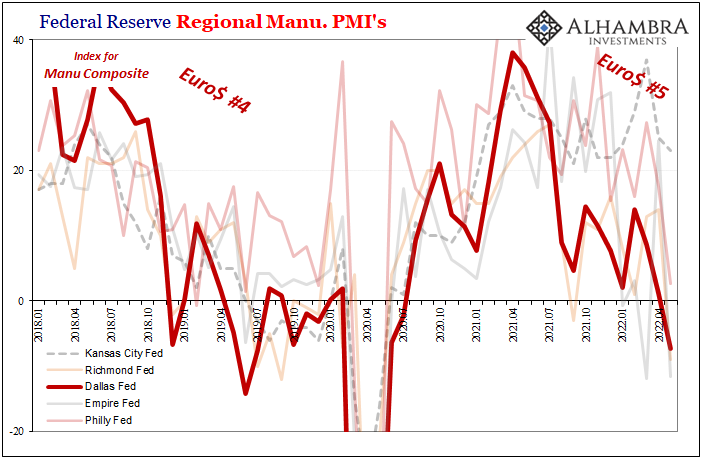

Demand trouble combined with excessive goods on hand, no wonder the manufacturing sector is really starting to fall apart. The latest today was the regional manufacturing survey out of the Fed’s Dallas folks. Their sector PMI was expected to rebound from -7.3 to around +1 or maybe zero. Instead, the overall figure dropped another 10 to end up at -17.7 for June 2022. |

. |

| It’s not the level – though in this case, yeah, the level is alarming, too – as it is the pace of this downturn. And it’s one that shows no signs of letting up anytime soon.

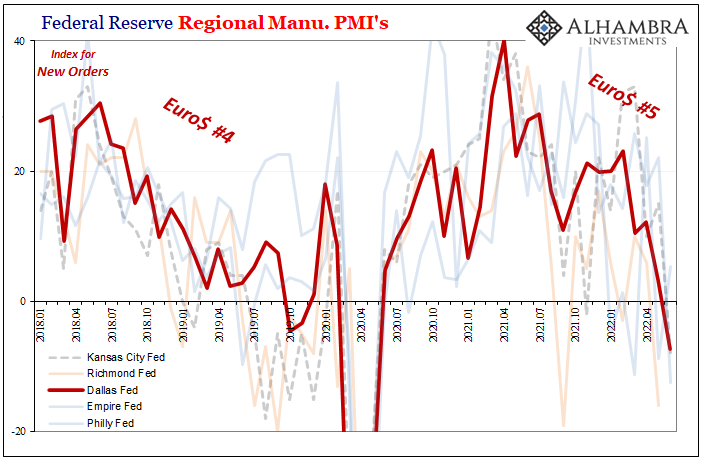

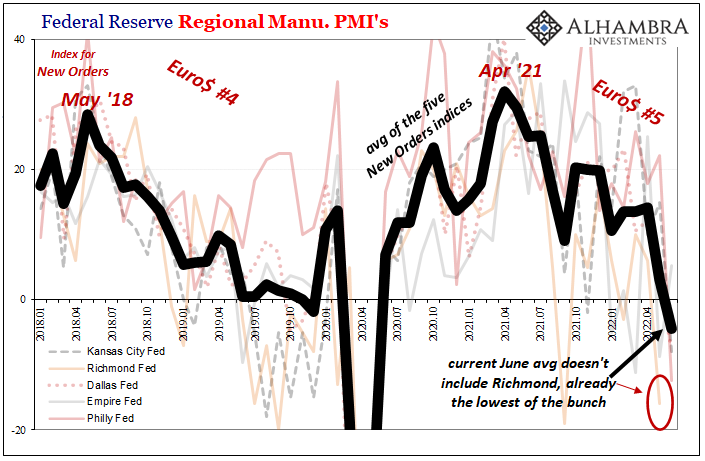

On the contrary, the forward-looking numbers clearly indicate worse still to come. For this survey, that meant June New Orders falling 10.5 points to read -7.3; lowest in Texas since 2020 and it’s not close. While the Richmond survey results will be released tomorrow (to go with inventory updates), even without it (and Richmond’s is the lowest yet) our five-survey regional average spells big trouble ahead for much of US domestic manufacturers. If this last of the quintuple just stays near where it’s been, the average’s only going much lower than what you see below (subtract another three). Classic inventory cycle, only in 2022 this means more than it did the last few times like 2018-19 or 2014-15. While during those the eventual “manufacturing recession” led to serious and synchronized global downturns, the goods economy today hyped up on this massive fed-fueled consumer frenzy was about the only recovery-like condition in the entire global system. What happens when, not if, this lone bright fire turns from burning red-hot to ice cold? It’s a rhetorical question, not rhetorically priced into market and curve probabilities. |

. |

You Might Also Like

Prices As Curative Punishment

Prices As Curative Punishment

2022-06-14

It wasn’t exactly a secret, though the raw data doesn’t ever tell you why something might’ve changed in it. According to the Bureau of Economic Analysis, confirmed by industry sources, US new car sales absolutely tanked in May 2022.

“Inflation” Not Inflation, Through The Eyes of Inventory

“Inflation” Not Inflation, Through The Eyes of Inventory

2022-06-11

It isn’t just semantics, nor some trivial, egotistical use of quotation marks. There is an actual and vast difference between inflation and “inflation.” And in the final results, that difference isn’t strictly or even mainly about consumer prices.Who cares, most people wonder. After all, what does it really matter why prices are going up so far?

ADP Front-Runs BLS and President Phillips

ADP Front-Runs BLS and President Phillips

2022-06-04

It’s gotten to the point that pretty much everyone is now aware of the risks. Public surveys, market behavior, on and on, hardly anyone outside politics thinks the economy is in a good place. Gasoline, sentiment, whatever, Euro$ #5 in total is much more than what’s shaping up inside the American boundary. Globally synchronized of which the US is proving to be a close part.

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown

2022-06-02

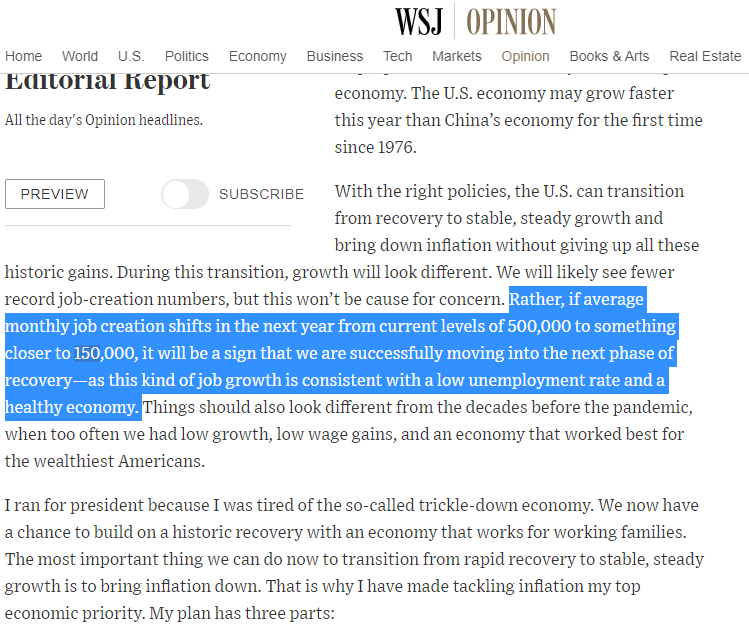

Just the other day, President Biden took to the pages of the Wall Street Journal to reassure Americans the government is doing something about the greatest economic challenge they face. Biden says this is inflation when that’s neither the actual affliction nor our greatest threat.

Is It Recession?

Is It Recession?

2022-04-30

According to today’s advance estimate for first quarter 2022 US real GDP, the third highest (inflation-adjusted) inventory build on record subtracted nearly a point off the quarter-over-quarter annual rate. Yes, you read that right; deducted from growth, as in lowered it. This might seem counterintuitive since by GDP accounting inventory adds to output.

Historic Inventory Continued In March, But Is It All Price Illusion, Too?

Historic Inventory Continued In March, But Is It All Price Illusion, Too?

2022-04-28

The Census Bureau today released its advanced estimates for March trade. These include, among other accounts like imports and exports, preliminary results reported by retailers and wholesalers. That means, for our purposes, inventories. Oh my, was there ever more inventory. It was, apparently, widely expected that following an avalanche of goods building up over the previous five months the situation might calm down a touch.

Briefing Even More Inventory

Briefing Even More Inventory

2022-03-01

Retail sales stumbled in December, contributing some to the explosion in inventory across the US supply chain – but not all. Inventories were going to spike even if sales had been better. In fact, retail inventories rose at such a record pace beyond anything seen before, had sales been far improved the monthly increase in inventories still would’ve unlike anything in the data series.

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

2022-01-29

The first time I can consciously remember using the term landmine was probably here in February 2019. I had described the same process play out several times before, I had just never applied that term. There was all sorts of market chaos in the final two months of 2018, including a full-on stock market correction, believe it or not, leaving the inflation and recovery narrative in near complete tatters.

Tags: currencies,demand,economy,Featured,Federal Reserve/Monetary Policy,Inventory,inventory cycle,manufacturing,Markets,newsletter