The clear winners in inflation are those who require little from global supply chains, the frugal, and those who own their own labor, skills and enterprises. As the case for systemic inflation builds, the question arises: who wins and who loses in an up-cycle of inflation? The general view is that inflation is bad for almost everyone, but this ignores the big winners in an inflationary cycle. As I’ve explained here and in my new book Global Crisis, National Renewal, the two primary dynamics globally are 1) scarcity of essentials and 2) extremes of wealth/power inequality. Scarcities drive prices higher simply as a result of supply-demand. Conventional economics holds that there are always cheaper substitutes for everything and hence there can never be scarcities

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The clear winners in inflation are those who require little from global supply chains, the frugal, and those who own their own labor, skills and enterprises.

As the case for systemic inflation builds, the question arises: who wins and who loses in an up-cycle of inflation? The general view is that inflation is bad for almost everyone, but this ignores the big winners in an inflationary cycle.

As I’ve explained here and in my new book Global Crisis, National Renewal, the two primary dynamics globally are 1) scarcity of essentials and 2) extremes of wealth/power inequality.

Scarcities drive prices higher simply as a result of supply-demand. Conventional economics holds that there are always cheaper substitutes for everything and hence there can never be scarcities enduring long enough to drive inflation: if steak gets costly, then consumers can buy cheaper chicken, etc.

But the conventional view overlooks essentials for which there is no substitute. Salt water may be cheap but it’s no substitute for fresh water.

There are no scalable substitutes for oil and natural gas. There are no scalable substitutes for hydrocarbon-derived fertilizers or plastics. As energy becomes more expensive due to the mass depletion of the cheap-to-extract resources, the costs of everything from fertilizer to plastics to steel to jet fuel rise.

This price pressure generates a number of effect. Rising costs embed a self-reinforcing feedback as prices are pushed higher in expectation of higher costs ahead, and these price increases generate the very inflation that sparked the pre-emptive price increase.

Second, increasing costs either reduce profits or force price increases. Neither is ideal, as higher prices tend to lower sales which then lowers profits.

Third, prices rise easily but drop only stubbornly, so sharp increases in prices aren’t reversed as cost pressures ease: enterprises and workers quickly become accustomed to the higher prices and pay and are extremely resistant to cutting either prices or pay.

As I’ve outlined here before, extremes of wealth-power inequality are systemically destabilizing. Extremes generate reversals as the pendulum reaches its maximum and then reverses direction and gathers momentum to the opposite extreme. In terms of wealth-power inequality, the pendulum is finally swinging back toward higher wages for labor and higher taxes for the super-wealthy, and increasing regulation on exploitive monopolies.

In other words, there is more driving systemic inflation than just “transitory” supply-demand issues. Speaking of supposedly “transitory” cost increases that are actually systemic, global supply chains that were deflationary (i.e. pushing prices lower) for 40 years are now inflationary (i.e. pushing prices higher) as costs rise sharply in exporting economies that are now facing much higher labor and energy costs, and also finally bearing the long-delayed costs of environmental damage caused by rampant industrialization.

As noted here in The Real Revolution Is Underway But Nobody Recognizes It, labor has been stripmined for 45 years, and now the worm has turned. As much as corporate employers and governments would love outright indentured servitude where they could force everyone to work for low pay in abusive circumstances, people are still free to figure out how to simplify their lives, cut expenses and work less.

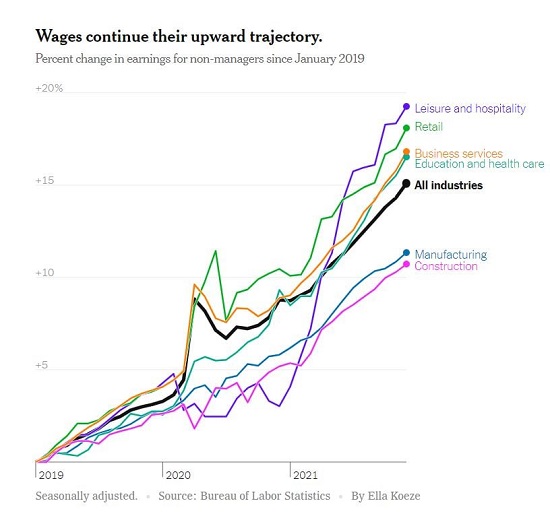

Scarcities of labor are enabling sharp increases in pay, especially in services. Anecdotally, I’m hearing accounts of service workers such as therapists, plumbers, accountants, architects, etc. raising their hourly rates by 20% overnight. In my own little sliver of the economy (writing / editing content), hourly rates are up as much as 30% for experienced independents.

So let’s highlight a few winners and losers in a self-reinforcing inflationary spiral.

Asset inflation driven by zero interest rates and a tsunami of central bank liquidity will lose steam as rates rise and the liquidity spigots are turned off. As mortgage rates rise, already overvalued homes will become even less affordable as the number of buyers who can afford much higher monthly payments recedes toward zero.

Local governments dependent on skyrocketing real estate valuations driving higher property taxes will be losers.

Bonds paying 1% interest are losers once rates click up to 2% or 3%.

Stocks are a mixed bag, as the relatively few companies with unlimited pricing power may benefit from inflation, but the majority will be pressured by higher labor, materials, shipping and energy costs, plus higher taxes and fees as the claw-back from capital gathers momentum.

|

Consumers are losers as costs soar, but service workers with pricing power are winners. The Federal Reserve can print $1 trillion in an instant but it can’t print experienced welders, plumbers, electricians, accountants, therapists, etc., and very little of this labor can be replaced by low-level (i.e. affordable) automation / robotics. Farmers who have been decimated by decades of low-cost imports might gain some pricing power as adverse weather, higher shipping costs and other factors increase the cost of imported agricultural commodities. Corporations with quasi-monopolies on essential industrial minerals/metals such as magnesium, nickel, etc. will have pricing power due to scarcity and the wide moat around their businesses: it isn’t cheap to set up competing mines and acquire rights to the minerals. As a general rule, keep an eye on inelastic demand and supply. Elastic demand refers to demand which can ebb and flow with costs–the classic substitution mentioned earlier in which costly beef is replaced by cheaper chicken. Elastic supply is ranchers responding to much higher beef prices by increasing their herds. There is always some elasticity in demand and supply as conservation, new efficiencies, recessions, etc. can stretch or shrink supplies and demand. But demand for essentials such as fertilizer, energy and food can only drop so much, and supply can only increase by so much. The clear winners in inflation are those who require little from global supply chains, the frugal, and those who own their own labor, skills and enterprises in sectors with relatively inelastic supply and demand. The losers are those who are entirely dependent on global supply chains for essentials, wastrels who squander resources, food, labor and money and those gambling on the quick return to zero-interest largesse and endless trillions in liquidity. |

. |

You Might Also Like

The Cult of Speculation Is a Cult of Doom

The Cult of Speculation Is a Cult of Doom

2022-01-25

Surely the Fed gods will affirm the cult’s most revered articles of faith. But false gods eventually fail, even the Fed. Every once in awhile the zeitgeist sets up an either / or: either the zeitgeist is crazy or I’m crazy. (OK, let’s agree I’m crazy; see, it’s not that hard to find something to agree on, is it?)

The Real Revolution Is Underway But Nobody Recognizes It

The Real Revolution Is Underway But Nobody Recognizes It

2022-01-15

Revolutions have a funny characteristic: they’re unpredictable. The general assumption is that revolutions are political. The revolution some foresee in the U.S. is the classic armed insurrection, or a coup or the fragmentation of the nation as states or regions declare their independence from the federal government.

Watch the Top 5percent – They’re the Key to the Whole Economy

Watch the Top 5percent – They’re the Key to the Whole Economy

2021-12-26

Go ahead and become dependent on asset bubbles and the free spending of the top 5%, and optimize your economy to serve this "growth," but be prepared for the consequences when the costs of this optimization and dependency come due.

The Fed’s Moral Hazard Monster Is About to Lay Waste to “Wealth”

The Fed’s Moral Hazard Monster Is About to Lay Waste to “Wealth”

2021-11-22

If the Fed set out to destroy the financial system, they’re very close to finishing the job. If you set out to destroy markets and the financial system, your most important weapon is moral hazard, the disconnection of risk and consequence. You disconnect risk from consequence by rewarding those making the riskiest bets and bailing out gamblers whose bets went bad.

Will China Pop the Global Everything Bubble? Yes

Will China Pop the Global Everything Bubble? Yes

2021-11-02

The line of dominoes that is already toppling extends around the entire global economy and financial system. Plan accordingly. That China faces structural problems is well-recognized.

Why Shortages Are Permanent: Global Supply Shortages Make Fantastic Financial Sense

Why Shortages Are Permanent: Global Supply Shortages Make Fantastic Financial Sense

2021-10-08

The era of abundance was only a short-lived artifact of the initial boost phase of globalization and financialization. Global corporations didn’t go to all the effort to establish quasi-monopolies and cartels for our convenience–they did it to ensure reliably large profits from control and scarcity.

The Banality of (Financial) Evil

The Banality of (Financial) Evil

2021-09-13

The financialized American economy and State are now totally dependent on a steady flow of lies and propaganda for their very survival. Were the truth told, the status quo would collapse in a putrid heap.

Please Don’t Pop Our Precious Bubble!

Please Don’t Pop Our Precious Bubble!

2021-09-09

It’s a peculiarity of the human psyche that it’s remarkably easy to be swept up in bubble mania and remarkably difficult to be swept up in the same way by the bubble’s inevitable collapse.

Tags: Featured,newsletter