It makes perfect financial sense to crash the market and no sense to reward the retail options marks by pushing it higher. An extraordinary opportunity to scoop up mega-millions in profits has arisen, and grabbing all this free money makes perfect financial sense. Now the question is: will those who have the means to grab the dough have the guts to do so? Here’s the opportunity: retail punters have gone wild for call options, churning .6 trillion in mostly short-term calls–bets on gains now, not later. This expansion of retail options exposure is unprecedented not just in its volume but in its concentration in short-term bets (options that expire in a few days) and in mega-cap tech companies that are commanding rich premiums for options. Goldman Stunned By The

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

It makes perfect financial sense to crash the market and no sense to reward the retail options marks by pushing it higher. An extraordinary opportunity to scoop up mega-millions in profits has arisen, and grabbing all this free money makes perfect financial sense. Now the question is: will those who have the means to grab the dough have the guts to do so?

Here’s the opportunity: retail punters have gone wild for call options, churning $2.6 trillion in mostly short-term calls–bets on gains now, not later. This expansion of retail options exposure is unprecedented not just in its volume but in its concentration in short-term bets (options that expire in a few days) and in mega-cap tech companies that are commanding rich premiums for options. Goldman Stunned By The Record $2.6 Trillion In Option Notional Traded Last Friday

The options market is like every other market only more so. The price of an option–a bet that a stock, ETF or index will go up or down before the option expires–is sensitive to the volatility of the underlying equity, the demand of other punters for options and the premium being demanded for time: the farther out the expiration date, the higher the cost of the option.

Recall that anyone with 100 shares of the underlying equity can write/originate an option. Each option controls 100 shares, so a call option that is listed at $1 costs the buyer of the call $100.

This is very sweet leverage if the market goes your way. You get all the gains of the 100 shares for a cost considerably less than buying the 100 shares outright. No wonder retail punters are going crazy for this cheap leverage to maximize gains in “can’t lose” trades.

Options have one funny trait: they can expire worthless and the punter loses the entire bet. Each option has an expiration date and a strike price–the price of the underlying equity that’s the pivot point for the bet: calls gain value if the equity’s price moves above the strike price and puts gain value if the equity’s price falls below the strike price.

The entity that sold the option gets to keep the money if it expires without any value. If you have 100 shares of Engulf & Devour and you sell me a call for $500 at a strike price of $100, if Engulf & Devour closes below $100 at expiration, you keep the $500 as pure profit and I lose the entire bet.

It would be extraordinarily profitable to sell a huge number of calls–bets on a move higher–and then pull the rug out by crashing the market just as all those options expire. It would criminally foolish not to crash the market and scoop up all that free money.

It would be extraordinarily profitable to sell a huge number of calls–bets on a move higher–and then pull the rug out by crashing the market just as all those options expire. It would criminally foolish not to crash the market and scoop up all that free money.

Here’s what makes the opportunity so extraordinary: the options universe is extremely lopsided. Bearish bets have dried up as the market has melted higher month after month; short bets are at record lows and the put-call ratio reflects the same capitulation of Bears and Bulls’ supreme confidence in near-term gains.

This means a crash will cost very little in terms of puts gaining value because there are so few puts out there and reap enormous gains as the vast majority of call options will expire worthless, leaving those who wrote the calls immensely wealthier.

In previous eras with lower retail option volume and a less lopsided options market, it wouldn’t be worth the trouble to flash-crash the market to scoop up retail calls. But a trillion here and a trillion there, and pretty soon you’re talking real money.

Buyers of “can’t lose” calls may be unaware that the tail can wag the dog. Mega-cap tech companies appear invulnerable to declines, but they are now the 800-pound gorillas in all the indices (Dow-30, S&P500, Nasdaq) and a boatload of ETFs. So triggering a mass sell-off in an index play such as SPY will trigger a sell-off in all the components of that index, including the invulnerable mega-cap tech names.

The opportunity here is amplified by the dominance of computer trading algorithms. Once a crash begins, the algos will trend-follow and liquidate exposure to lower risk. This sets up a self-reinforcing chain of selling as every drop triggers more sell programs.

Volumes are so low that it won’t take that big of a leveraged sell order to start the rug-pull.

Add up the extraordinary size of retail options bets, the lopsided Bullish bias in calls and the short-duration of the calls and you have an unprecedented opportunity to scoop mega-millions of dollars by doing a rug-pull of the market via selling leveraged indices instruments.

Retail call buyers are basically begging the big players to take their money via a flash-crash, and the players would be insanely incompetent not to take the money laying on the table. It has all the moving parts of a perfect con: convince the retail punters that they can’t lose by buying calls, jack up the premium they’re paying to own that beautiful leverage for a few days or weeks, lead them on with little rallies, “proving” they can’t lose and encouraging them to buy more high-priced calls, crush volatility to show the futility of buying puts and persuade the punters they have no need for any hedge, as the market can only loft higher because the Fed, etc.

Then bang, pull the rug out and crash the market limit down for a few days. It’s a gorgeous set-up, literally picture-perfect. It makes perfect financial sense to crash the market and no sense to reward the retail options marks by pushing it higher. Let’s see who gets to be the Roadrunner and who ends up as Wile E. Coyote.

You Might Also Like

Will China Pop the Global Everything Bubble? Yes

Will China Pop the Global Everything Bubble? Yes

2021-11-02

The line of dominoes that is already toppling extends around the entire global economy and financial system. Plan accordingly. That China faces structural problems is well-recognized.

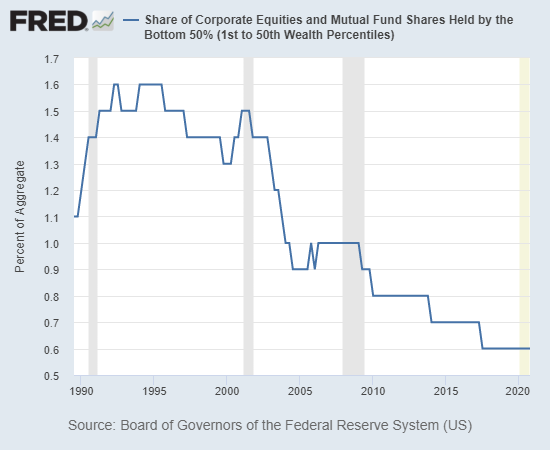

America’s Bottom 50 percent Have Nowhere To Go But Down

America’s Bottom 50 percent Have Nowhere To Go But Down

2021-10-14

One might anticipate that the bottom 50%’s meager share of the nation’s exploding wealth would have increased as smartly as the wealth of the billionaires, but alas, no.

Risk Was Never Low, It Was Only Hidden

Risk Was Never Low, It Was Only Hidden

2021-10-05

The vast majority of market participants are about as ready for a semi-random “volatility event” as the dinosaurs were for the meteor strike that doomed them to oblivion.

Are We Really So “Rich”? A New Way of Defining Wealth

Are We Really So “Rich”? A New Way of Defining Wealth

2021-09-27

What if our commoditized, financialized definition of wealth reflects a staggering poverty of culture, spirit, wisdom, practicality and common sense? The conventional definition of wealth is solely financial: ownership of money and assets.

The assumption is that money can buy anything the owner desires: power, access, land, shelter, energy, transport and if not love, then a facsimile of caring.

The Upside of a Stock Market Crash

The Upside of a Stock Market Crash

2021-08-24

A drought-stricken forest choked with dry brush and deadfall is an apt analogy. While a stock market crash that stairsteps lower for months or years is generally about as welcome as a trip to the guillotine in Revolutionary France, there is some major upside to a crash.

When Expedient “Saves” Become Permanent, Ruin Is Assured

When Expedient “Saves” Become Permanent, Ruin Is Assured

2021-07-01

The belief that the Federal Reserve possesses god-like powers and wisdom would be comical if it wasn’t so deeply tragic, for the Fed doesn’t even have a plan, much less wisdom. All the Fed has is an incoherent jumble of expedient, panic-driven “saves” it cobbled together in the 2008-2009 Global Financial Meltdown that it had made inevitable.

The Sources of Rip-Your-Face-Off Inflation Few Dare Discuss

The Sources of Rip-Your-Face-Off Inflation Few Dare Discuss

2021-06-09

Inflation will be transitory, blah-blah-blah–I beg to differ, for these reasons. There are numerous structural sources of inflation, which I define as prices rise while the quality and quantity of goods and services remain the same or diminish.

Tags: Featured,newsletter