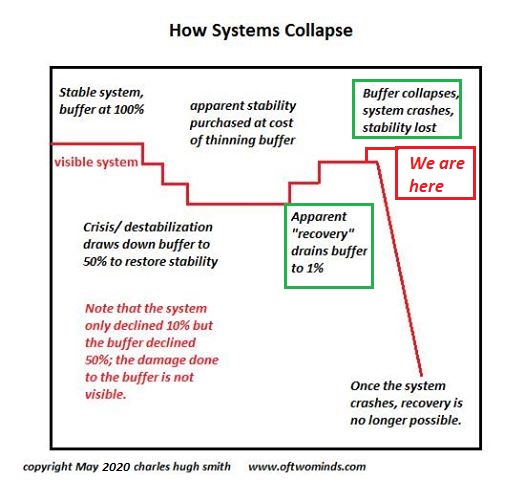

Risk has not been extinguished, it is expanding geometrically beneath the false stability of a monstrously manipulated market. One of the most under-appreciated investment insights is courtesy of Mike Tyson: “Everybody has a plan until they get punched in the mouth.” At this moment in history, the plan of most market participants is to place their full faith and trust in the status quo’s ability to keep asset prices lofting ever higher, essentially forever. In other words, the vast majority of punters are convinced they will never suffer the indignity of getting punched in the mouth by a market crash. What makes this confidence so interesting is massively distorted markets always end the same way: crisis, crash and collapse. The core dynamic here is distorted

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Risk has not been extinguished, it is expanding geometrically beneath the false stability of a monstrously manipulated market.

| One of the most under-appreciated investment insights is courtesy of Mike Tyson: “Everybody has a plan until they get punched in the mouth.” At this moment in history, the plan of most market participants is to place their full faith and trust in the status quo’s ability to keep asset prices lofting ever higher, essentially forever.

In other words, the vast majority of punters are convinced they will never suffer the indignity of getting punched in the mouth by a market crash. What makes this confidence so interesting is massively distorted markets always end the same way: crisis, crash and collapse. The core dynamic here is distorted markets provide false feedback and misleading information which then lead to participants making catastrophically misguided decisions. Investment decisions made on poor information will also be poor, leading participants to end up poor, to their very great surprise. The surprise comes from the falsity of the feedback, as those who are distorting markets want punters to believe “the market” is functioning transparently. If you’re manipulating the market, the last thing you want is for the unwary marks to discover that the market is generating false signals and misleading information on risk, as knowing the market is being distorted would alert them to the extraordinary risks intrinsic to heavily distorted markets. The risks arise from the disconnect between the precariousness of the manipulated market and the extreme confidence punters have in its stability and predictability. The predictability comes not from transparent feedback and market signals but from the manipulation. This stability is entirely fabricated and therefore it lacks the dynamic stability of truly open markets. |

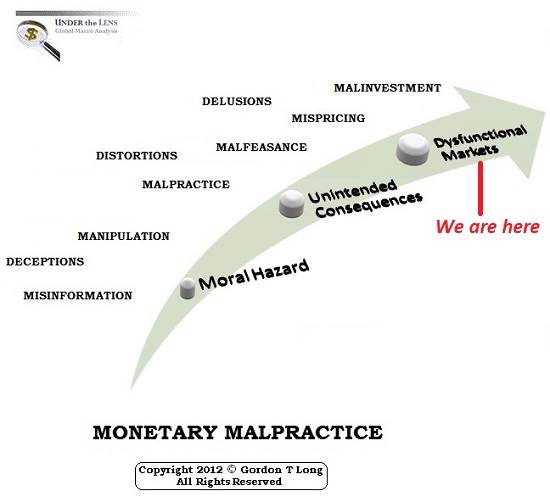

Dysfunctional Markets - Click to enlarge |

| Markets that are being distorted/manipulated to achieve a goal that is impossible in truly open markets–for example, markets that only loft higher with near-zero volatility–lull participants into a dangerous perception that because markets are so stable, risk has dissipated.

In actuality, risk is skyrocketing beneath the surface of the artificial stability because the market has been stripped of the mechanisms of dynamic stability. This artificial stability derived from sustained manipulation has the superficial appearance of low-risk markets, i.e., low levels of volatility, but this lack of volatility derives not from transparency but from behind-the-scenes suppression of volatility. Another source of risk in distorted markets is the illusion of liquidity: in low-volume markets of suppressed volatility, participants are encouraged to believe that they can buy and sell whatever securities they want in whatever volumes they want without disturbing market pricing and liquidity. In other words, participants are led to believe that the market will always have a bid due to the near-infinite depth of liquidity: no matter how many billions of dollars of securities you want to sell, there will always be a bid for your shares. In actual fact, the bid is paper-thin and it vanishes altogether once selling rises above very low levels. Heavily manipulated markets are exquisitely sensitive to selling because the entire point is to limit any urge to sell while encouraging the greed to increase gains by buying more. The illusions of low risk, essentially guaranteed gains for those who increase their positions and near-infinite liquidity generate overwhelming incentives to borrow more and leverage it to the hilt to maximize gains. The blissfully delusional punter feels the decision to borrow the maximum available and leverage it to the maximum is entirely rational due to the “obvious” absence of risk, the “obvious” guaranteed gains offered by markets lofting ever higher like clockwork and the “obvious” abundance of liquidity, assuring the punter they can always sell their entire position at today’s prices and lock in profits at any time. |

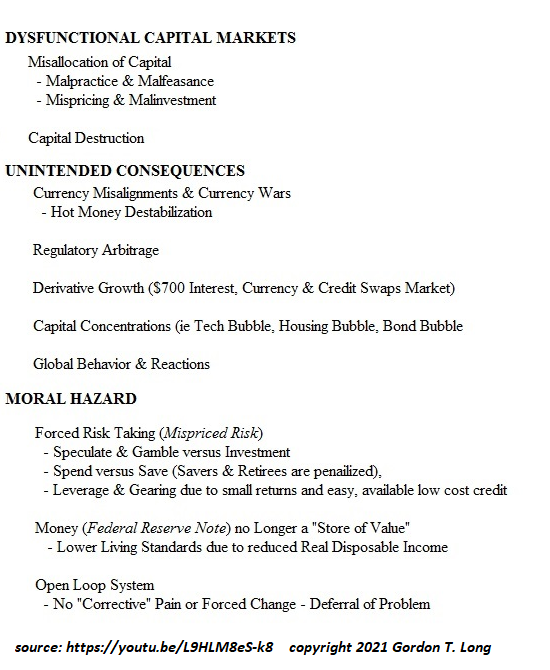

Monetary Malpractice - Click to enlarge |

| On top of all these grossly misleading distortions, punters have been encouraged to believe in the ultimate distortion: the Federal Reserve will never let markets decline again, ever. This is the perfection of moral hazard: risk has been disconnected from consequence.

In this perfection of moral hazard, punters consider it entirely rational to increase extremely risky speculative bets because the Federal Reserve will never let markets decline. Given the abundant evidence behind this assumption, it would be irrational not to ramp up crazy-risky speculative bets to the maximum because losses are now impossible thanks to the Fed’s implicit promise to never let markets drop. This is why distorted, manipulated markets always end the same way: first, in an unexpected emergence of risk, which was presumed to be banished; second, a market crash as the paper-thin bid disappears and prices flash-crash to levels that wipe out all those forced to sell by margin calls, and then the collapse of faith in the manipulators (the Fed), collapse of the collateral supporting trillions of dollars in highly leveraged debt and then the collapse of the entire delusion-based financial system. Gordon Long and I illuminate the many layers of distortion, manipulation and moral hazard in our new video presentation It Always Ends The Same Way (34:33). Amidst the ruins generated by well-meaning manipulation and distortion, the “well meaning” part will leave an extremely long-lasting bitter taste in all those who failed to differentiate between the false signals and distorted information of manipulated markets and the trustworthy transparency of signals arising in truly open markets. In summary: risk has not been extinguished, it is expanding geometrically beneath the false stability of a monstrously manipulated market. As I often note here, risk cannot be extinguished, it can only be transferred. By distorting markets to create an illusion of low-risk stability, the Federal Reserve has transferred this fatal supernova of risk to the entire financial system. |

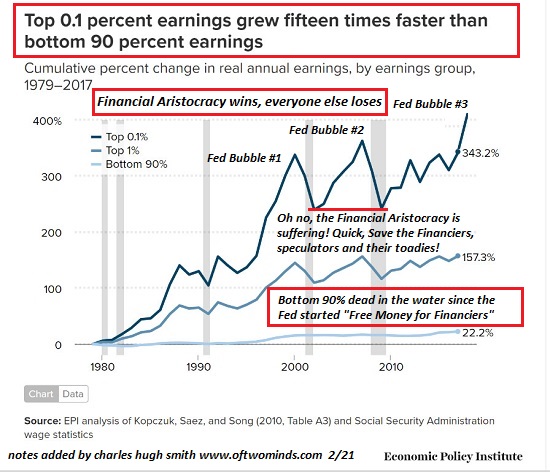

Inequality Income, 1980 - 2020 - Click to enlarge |

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-21

Update June 21 2021: SNB intervening. Sight Deposits have risen by +1.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

Sickcare is the Knife in the Heart of Employment–and the Economy

Sickcare is the Knife in the Heart of Employment–and the Economy

2021-05-18

We need to change the incentives of the

entire system, not just healthcare, but if we don’t start with healthcare, that financial

cancer will drag us into national insolvency all by itself.

American Healthcare is a growth industry in the same way cancer is a growth industry:

both keep growing until they kill the host, which in the case of healthcare is the U.S. economy.

While a great many individuals in the system care about improving the health of their patients,

the healthcare system itself only cares about one thing: maximizing profits by any means

available, including sending many patients to an early grave via medications which corporations

declared "safe" and rigged the political-regulatory-research systems to comply.

I call this maximizing profits by any means available

Hey Fed, Explain Again How Making Billionaires Richer Creates Jobs

Hey Fed, Explain Again How Making Billionaires Richer Creates Jobs

2021-05-08

Despite their hollow bleatings about ‘doing all we can to achieve full employment’,

the Fed’s policies has been Kryptonite to employment, labor and the bottom 90%–and most especially

to the bottom 50%, the working poor that one might imagine most deserve a leg up.

As wealth and income inequality soar to new heights thanks to the Federal Reserve’s policies

of zero interest rates, money-printing and financial stimulus, the Fed says its goal is to create

more jobs. Really? OK, let’s look at how the Fed’s doing with that.

I’ve assembled a chart deck to display the consequences of Fed policies on debt, wealth

inequality and employment. Recall what Fed policies actually do:

1. Zero interest rate policy (ZIRP) destroyed the low-risk return on savings and money market funds,

stripping

If You Don’t See Any Risk, Ask Who Will “Buy the Dip” in a Freefall?

If You Don’t See Any Risk, Ask Who Will “Buy the Dip” in a Freefall?

2021-04-20

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted, liquidity is not guaranteed. The current market melt-up is taken as nearly risk-free because the Fed has our back, i.e. the Federal Reserve will intervene long before any market decline does any damage.

The Middle Class Has Finally Been Suckered into the Casino

The Middle Class Has Finally Been Suckered into the Casino

2021-04-15

The Fed’s casino isn’t just rigged; it’s criminally unstable. The decay of America’s middle class has been well documented and many commentators have explored the causal factors. The bottom line is that this decay isn’t random; the income of the middle class isn’t going to suddenly increase at 15 times the growth rate of the income of the top 0.1%. (see chart below) The income of the top 0.1% grew 15 times faster than the incomes of the bottom 90% because that’s the only possible output of America’s distorted financial system.

Too Busy Frontrunning Inflation, Nobody Sees the Deflationary Tsunami

Too Busy Frontrunning Inflation, Nobody Sees the Deflationary Tsunami

2021-03-08

Those looking up from their "free fish!" frolicking will see the tsunami too late to save themselves. It’s an amazing sight to see the water recede from the bay, and watch the crowd frolic in the shallows, scooping up the flopping fish. In this case, the crowd doing the "so easy to catch, why not grab as much as we can?" scooping is frontrunning inflation, the universally expected result of the Great Reflation Trade.

Our Fragile, Brittle Stock Market

Our Fragile, Brittle Stock Market

2021-02-03

This heavily managed ‘market structure’ is far from equilibrium and extremely prone to instability.

The Coming Revolt of the Middle Class

The Coming Revolt of the Middle Class

2021-01-28

That’s how Neofeudal systems collapse: the tax donkeys and debt-serfs finally

rebel and start demanding the $50 trillion river of capital take a new course.

The Great American Middle Class has stood meekly by while the New Nobility stripmined

$50 trillion from the middle and working classes. As this RAND report documents, $50 trillion has

been siphoned from labor and the lower 90% of the workforce to the New Nobility and their

technocrat lackeys who own the vast majority of the capital:

Trends in Income From 1975 to 2018.

Why has the Great American Middle Class meekly accepted their new role as debt-serfs and

powerless peasants in a Neofeudal Economy ruled by the New Nobility of Big Tech /

monopolies / cartels / financiers? The basic answer is the New Nobility’s PR has been

so

Tags: Featured,newsletter