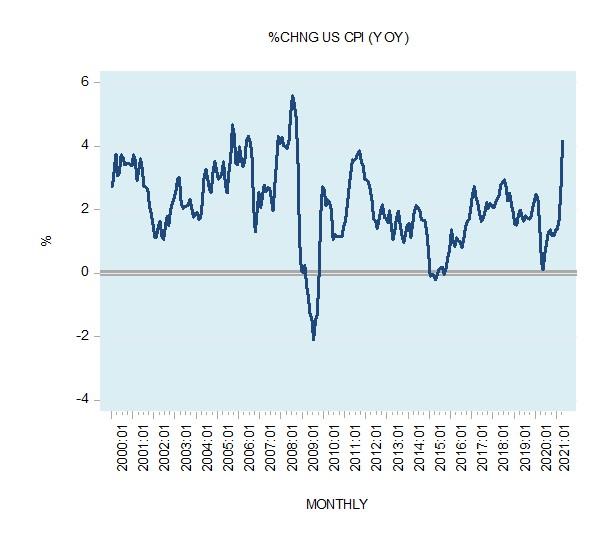

The increase in the growth rate of the Consumer Price Index (CPI) has fueled concerns that if the rising trend were to continue the Fed is likely to tighten its interest rate stance. Observe that the yearly growth rate in the CPI climbed to 4.2 percent in April from 2.6 percent in March and 0.3 percent in April 2020. We hold that because of massive increases in the money supply, it is likely that the growth momentum of prices is going to follow a rising trend. U.S. CPI YoY, 2000 - 2021 - Click to enlarge Note that the yearly growth rate of money supply climbed to 79 percent in February from 6.5 percent in February 2020. Various increases in the prices of goods are just the manifestation of increases in money supply. Once money enters a particular market,

Topics:

Frank Shostak considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The increase in the growth rate of the Consumer Price Index (CPI) has fueled concerns that if the rising trend were to continue the Fed is likely to tighten its interest rate stance. Observe that the yearly growth rate in the CPI climbed to 4.2 percent in April from 2.6 percent in March and 0.3 percent in April 2020.

We hold that because of massive increases in the money supply, it is likely that the growth momentum of prices is going to follow a rising trend. |

U.S. CPI YoY, 2000 - 2021 - Click to enlarge |

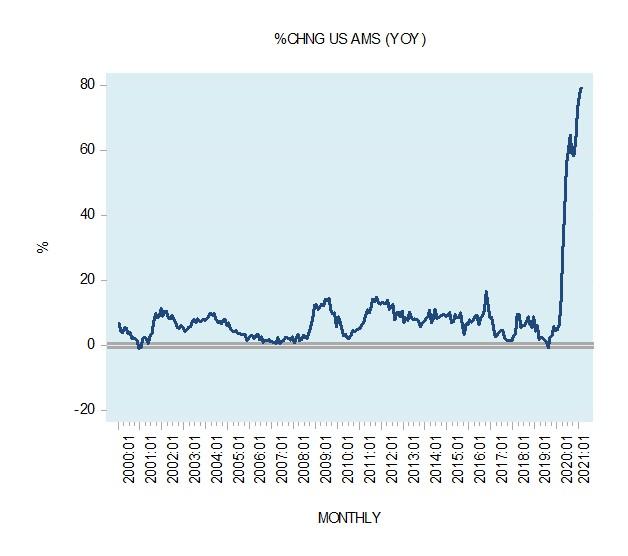

| Note that the yearly growth rate of money supply climbed to 79 percent in February from 6.5 percent in February 2020. Various increases in the prices of goods are just the manifestation of increases in money supply.

Once money enters a particular market, this means that more money is paid for a product in that market. Alternatively, we can say that the price of a good in this market has gone up. Note that a price is the number of dollars per unit of something. |

U.S. AMS YoY, 2000 - 2021 - Click to enlarge |

Hence, an increase in money supply, all other things being equal, implies that a greater amount of money is going to enter into various markets. This means that the prices of goods will follow suit.

Also, note that when money is injected it enters a particular market. Once the price of a good is rising to the level that is perceived as fully valued then the money leaves to another market, which is considered as undervalued. The shift from one market to another market gives rise to a time lag from increases in money and its effect on the average price increases.

Because of the time lag, the manifestation of the current strong increases in money supply in terms of the prices of goods is likely to become visible in the months ahead.

On account of the likely uptrend in the growth rate of the prices of goods in the months ahead we hold that the economic bust is going to emerge regardless of whether the Fed is going to tighten its interest rate stance or not. Here is why.

Money Supply and Liquidity

In a market economy, a major service that money provides is that of the medium of exchange. Producers exchange their goods for money and then exchange money for other goods. As the production of goods increases, this results in a greater demand for money. Conversely, as economic activity slows down the demand for money follows suit.

The demand for money is also affected by changes in prices. An increase in the prices of goods and assets leads to an increase in the demand for money. People now demand more money to facilitate goods and assets that are more expensive. A fall in the prices of goods and assets results in a decline in the demand for money.

According to Mises,

The services money renders are conditioned by the height of its purchasing power. Nobody wants to have in his cash holding a definite number of pieces of money or a definite weight of money; he wants to keep a cash holding of a definite amount of purchasing power.1

Changes in the Supply of Money and Liquidity

Consider an increase in the supply of money for a given state of economic activity. Since we did not have here a change in the demand for money, this means that people now have a surplus of money. No individual wants to hold more money than is required. An individual can get rid of surplus money by exchanging the money for goods and assets. Individuals as a group however cannot dispose of the surplus of money just like that. They can only shift money from one individual to another individual.2

The mechanism that generates the reduction of the surplus of money is the increase in the prices of goods and assets. Once individuals start to employ the surplus of money in acquiring goods and assets this pushes goods and asset prices higher. As a result, the demand for money increases. All this in turn works towards the decline in the monetary surplus.

Whilst increases in the money supply for a given level of economic activity results in a monetary surplus, a fall in the money supply for a given level of economic activity leads to a monetary deficit.

Individuals still demand the same amount of money. To accommodate this they will start selling goods and assets for money, thus pushing goods and asset prices lower. At lower prices, the demand for money declines and this in turn works towards the elimination of the monetary deficit.

When Changes in Liquidity Occur Due to Factors Other Than Changes in the Money Supply

A monetary surplus or a deficit can also emerge in response to changes in economic activity and changes in prices.

For instance, an increase in liquidity can emerge for a decline in economic activity whilst the stock of money and the prices of goods and assets remain unchanged. A decline in economic activity results in a fewer goods produced. This means that less goods are going to be exchanged – implying a decline in the demand for money. Conversely, an increase in economic activity whilst the stock of money and the prices of goods and assets stay unchanged produces a monetary deficit.

If an increase in the prices of goods and assets, all other things being equal, takes place this triggers an increase in the demand for money. This puts downward pressure on liquidity. To restore the balance individuals are likely to start selling goods and assets in order to accommodate the increase in the demand for money. Conversely, a decline in the prices of goods and assets triggers a decline in the demand for money and within all other things being equal to the increase in liquidity.

Note that changes in real economic activity and changes in prices are factors that affecting the demand for money. Hence, we can suggest that changes in liquidity are driven by changes in the supply of money minus changes in the demand for money.

Consequently, changes in liquidity are defined as

% Change in Liquidity = % Change in Money Supply – % Change in Real Economic Activity – percent Change in Prices

We can thus establish that changes in monetary liquidity are the outcome of the interplay between the supply and the demand for money.

Easy Monetary Policy Sets the Stage for an Economic Bust

Again, the yearly growth rate of the US money supply as depicted by our AMS (Austrian money supply) metric stood at 79 percent in February this year against 6.5 percent in February 2020. This massive increase has likely severely undermined the pool of real savings and set the platform for large increases in the prices of goods and assets. We suggest that within all other things being equal, a rising momentum of prices is going to increase the demand for money thereby weakening the excess money growth, i.e., the monetary liquidity.

This is likely to result in the selling of goods and assets and to the decline in the growth momentum of prices. Consequently, within all other things being equal nominal economic activity in terms of GDP is likely to come under downward pressure.

We suggest that a weakening in the pool of real savings due to very loose monetary and fiscal policies is going to exert a further downward pressure on the growth rate of GDP.

Note that the likely economic slump is because of the increase in the prices of goods and assets coupled with the weakening in the pool of real savings. The increase in prices is expected to weaken the monetary liquidity thereby setting in motion the selling of goods and assets thus depressing the goods and asset prices momentum. Observe that the trigger to all this is past strong increases in money supply.

If the Fed were to embark on aggressive monetary pumping to counter economic recession this is going to dilute further the pool of real savings and make things much worse. Note that the economic slump is likely to emerge regardless of whether the Fed is going to tighten its interest rate stance or not. The key cause for this is the increase in the growth momentum of goods and asset prices because of past strong monetary growth.

Hence, we could end up in an economic slump as a result of the past strong monetary growth. The economic slump is likely to emerge regardless of whether the Fed is going to tighten its monetary stance or not. The severity of the slump is going to be dictated by the state of the pool of real savings.

- 1. Ludwig von Mises, Human Action: A Treatise on Economics, 3d rev. ed. (Chicago: Contemporary Books, 1966), p. 421.

- 2. Murray N. Rothbard, The Mystery of Banking (New York: Richardson and Snyder, 1983), pp. 29–41.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-07

Update June 04 2021: SNB intervening. Sight Deposits have risen by +0.3 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

Title IX Will Become a Vehicle of More Injustice

Title IX Will Become a Vehicle of More Injustice

2021-02-07

President Joe Biden vowed to put a “quick end” to the Trump administration’s Title IX regulations and return to Obama-era ones at universities. If this happens, the sexual misconduct hearings will be deeply impacted.

There’s Nothing Wrong with Short Selling

There’s Nothing Wrong with Short Selling

2021-02-04

The recent GameStop short-squeeze drama has riveted financial markets. Given the historic unpopularity of short sellers (e.g., Holman Jenkins has written that “short-selling is…widely unpopular with everyone who has a stake in seeing stock prices go up”), the resulting heightened invective against them is not a surprise.

Biden Nominee Rachel Levine Was a Disaster in Pennsylvania. Now She’s Headed to Washington.

Biden Nominee Rachel Levine Was a Disaster in Pennsylvania. Now She’s Headed to Washington.

2021-01-25

On January 19 it was announced that Joe Biden planned to nominate Rachel Levine, the Pennsylvania (PA) secretary of health, for the position of assistant secretary of health in the Department of Health and Human Services. This is potentially good news for Pennsylvanians, who will finally be rid of her after having had to endure her disastrous covid lockdowns and restrictions for nearly a year, but is likely bad news for the rest of the country.

The Myths Behind the “Capitalism Is Racist” Claim

The Myths Behind the “Capitalism Is Racist” Claim

2021-01-22

Though numerous studies prove the contrary, it is still widely assumed that capitalism perpetuates racism. Celebrities and academics incessantly broadcast the message that capitalism engenders racism.

The Upside of Lockdowns: More Saving

The Upside of Lockdowns: More Saving

2021-01-18

Rothbard: “At the outset of every step forward on the road to a more plentiful existence is saving….Without saving and capital accumulation there could not be any striving toward nonmaterial ends.”

Fiscal Stimulus vs. Economic Growth

Fiscal Stimulus vs. Economic Growth

2021-01-12

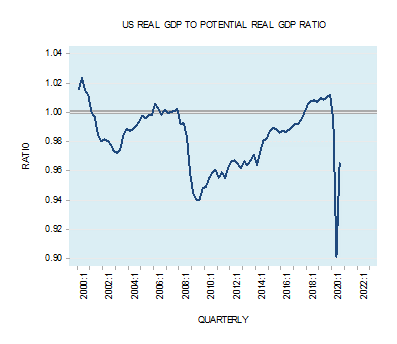

[unable to retrieve full-text content]For most experts a key factor that policymakers should be watching is the ratio between actual real output and potential real output. The potential output is the maximum output that the economy could attain if all resources are used efficiently. In Q3 2020, the US real GDP–to–potential US real GDP ratio stood at 0.965 against 1.01 in Q3 2019.

California Now Wants to Tax People Who Live in Other States, Too

California Now Wants to Tax People Who Live in Other States, Too

2021-01-07

California’s government has become infamous for abusing its citizens, from steep taxation to burdensome regulations to arbitrary covid impositions. But less noticed is how it is also trying to abuse other Americans as well.

Tags: Featured,newsletter