Any economy that concentrates its wealth and income in the top tier is a fragile economy. There are two structural reasons why consumer spending will not rebound, no matter how “open” the economy may be. Virtually everyone who glances at headlines knows the global economy is lurching into either a deep recession or a full-blown depression, depending on the definitions one is using. Everyone also knows the stock market has roared back as if nothing has happened. While most financial pundits have accepted that a V-shaped recovery is not possible, few (if any) observers have discussed two factors that will cause consumer spending to crash harder than generally expected: 1. The top 10% of households account for about half of all consumer spending, and these are the

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Any economy that concentrates its wealth and income in the top tier is a fragile economy.

There are two structural reasons why consumer spending will not rebound, no matter how “open” the economy may be. Virtually everyone who glances at headlines knows the global economy is lurching into either a deep recession or a full-blown depression, depending on the definitions one is using. Everyone also knows the stock market has roared back as if nothing has happened.

While most financial pundits have accepted that a V-shaped recovery is not possible, few (if any) observers have discussed two factors that will cause consumer spending to crash harder than generally expected:

1. The top 10% of households account for about half of all consumer spending, and these are the households that will be most affected by the sharp drop in assets, small business income and the shrinking of heretofore “safe” white-collar jobs in higher education, healthcare, finance, etc.

|

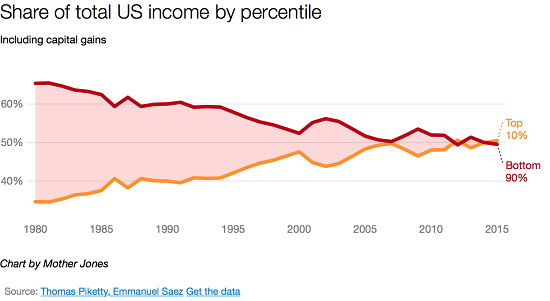

In other words, since the top 10% own roughly 85% of all non-family-home assets (i.e. stocks, bonds, business equity, rental real estate), the decline in the value of these assets and the decline in the income generated by these assets will hit the top 10%, not the bottom 90% who own a tiny sliver of these assets. (see charts below) Companies are slashing dividends, tenants are not paying rent and family-owned businesses will experience declines in revenues and profits–even those which have yet to feel the consequences. All of these income streams and assets are owned by the top 10%, and so all these declines in wealth and income will be concentrated in the top 10%. 2. The majority of the wealth owned by top 10% households is held by people 50 years of age or older, and this older cohort that owns most of the wealth and the income streams generated by the wealth are more at risk of Covid-19 than younger people. Surveys have found that people who feel more at risk are much less inclined to start going back to restaurants, musical events, etc., or going on cruises or airline flights. It’s important to note that risk is an internal assessment. Thus the economy can be completely open again but people who feel cautious won’t resume their old spending habits, and there is no way to force them to do so. The data strongly suggests elderly people and those with metabolic issues–obesity, high levels of sugar or cholesterol, and high blood pressure–are at greater risk than healthier people. (Vitamin D and zinc deficiencies may also play a role, as well as general immune response.) I recently saw a statistic that only 15% of the American populace is metabolically healthy. The point here is that a sense of heightened risk is sensible for a great many people, and since the owners of most of the wealth are older, this caution will have outsized impacts on consumer spending. |

Share of total US income, 1980-2015 - Click to enlarge |

| Combine this with the shrinking wealth and income of the top 10%, and you get a double-whammy reduction in consumption.

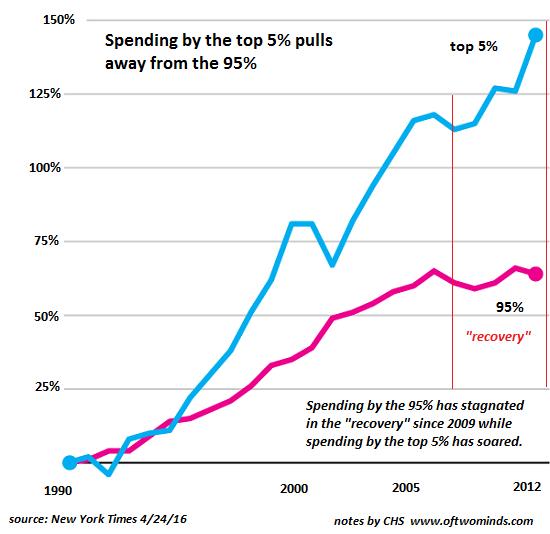

It’s also instructive to gauge the enormous asymmetry in what the top 10% spend on services compared to the bottom 90%. The bottom 90% may get their hair or nails done and have the oil changed in their car, but they typically can’t afford (or don’t need) all the services routinely engaged by the top 10%: dog walkers, CPAs, tax accountants, attendants for elderly parents, piano lessons and other tutoring for children, fitness trainers, career counselors, landscape designers and so on–the list is practically endless. Once the top 10% are forced to tighten their belts, it won’t be Wal-Mart sales that are hit–it will be millions of service providers who depended solely on the top 10% (or top 5%) for virtually all their income. All the professions that only served the top 10% will be decimated, as they are all inessential. Virtually every one of these tasks can be cancelled, put off into the future, or performed by the household if push comes to shove financially. The arts and performing arts that depend almost entirely on costly ticket sales to the wealthy and donations from top 5% households will also be decimated. If you attend the symphony, ballet or opera, you know 90%+ of the audience is over 60–the very cohort that will now hesitate to spend lavishly or attend crowded performances. Based on my admittedly informal observations, I think it’s a fair assessment to say that a great many top 10% households are in denial about the financial tsunami that’s about to hit them. Since they weren’t furloughed like lower-income workers, they have a delusional faith that their incomes, business and wealth will survive the depression intact. |

Spending by the top 5% pulls away from the 95% - Click to enlarge |

| They are looking at the water receding from the bay, leaving all the fish flopping in the seabed, and reckoning that’s the worst that will happen. They don’t yet understand that the tsunami that’s about to roar ashore is not yet visible. The financial wave has yet to hit them, but when it does, they will find:

1. Their unearned/investment income will drop. If assets will lose $10 trillion in value, virtually all of this will come out of the accounts of the top 10%. If investment and business income declines by $1 trillion, virtually all of this will come out of the incomes of the top 10%. |

Percent of total Investment assets held, by wealth distribution - Click to enlarge |

| In summary: the vast majority of spending by the bottom 90% isn’t discretionary: it’s mostly servicing debt (student loans, mortgages, auto/truck loans, credit cards, etc) and essentials (rent, food, utilities, etc.), with modest discretionary spending on fast food and cheap goods.

In contrast, the top 10% spending–almost half of all consumer spending– has supported a vast number of service businesses, jobs, arts organizations, etc.–entities that receive very little of their revenues from the bottom 90%. As the top 10%’s income crashes, so will their discretionary spending. The older the wealthy household, the more likely they will hesitate to spend as their nestegg is crushed and their caution about crowds endures. These dynamics are under-appreciated in my view, and so the majority of media commentators and the top 10% themselves are unprepared for the asymmetric impacts on their own wealth, income and livelihood that will sweep ashore later this year. Any economy that concentrates its wealth and income in the top tier is a fragile economy. |

For Richer and Poorer, 2002-2012 - Click to enlarge |

You Might Also Like

The Way of the Tao Is Reversal

The Way of the Tao Is Reversal

As Jackson Browne put it: Don’t think it won’t happen just because it hasn’t happened yet. We can summarize all that will unfold in the next few years in one line: The way of the Tao is reversal. This is the opening line of Chapter 40 of Lao Tzu’s 5,000-character commentary on the Tao, The Tao Te Ching. There are many translations of this slim volume, and for a variety of reasons I favor the 1975 translation by my old professor at the University of Hawaii, Chang Chung-yuan (1907-1988), whom I would occasionally see doing Tai Chi late at night on his front yard in Manoa Valley.

The Collapse of Main Street and Local Tax Revenues Cannot Be Reversed

The Collapse of Main Street and Local Tax Revenues Cannot Be Reversed

The core problem is the U.S. economy has been fully financialized, and so costs are unaffordable. To understand the long-term consequences of the pandemic on Main Street and local tax revenues, we need to consider first and second order effects. The immediate consequences of lockdowns and changes in consumer behavior are first-order effects: closures of Main Street, job losses, massive Federal Reserve bailouts of the top 0.1%, loan programs for small businesses, stimulus checks to households that earned less than $200,000 last year, and so on.

Different Type of Crisis, Some Old Concerns

Different Type of Crisis, Some Old Concerns

Over the past two months we have witnessed historic turmoil followed by unprecedented intervention by policy makers and central banks in supporting the capital markets (and more). In many ways the 2020 COVID-19 pandemic is very different from the 2008 global financial crisis, but for some, certain old concerns still linger. In the face of short selling bans and worries about market liquidity, we discuss below how best to navigate some of the common objections and concerns related to securities lending and how to position your securities lending program in the current environment and beyond.

Dollar Mixed as Markets Await Fresh Drivers

Dollar Mixed as Markets Await Fresh Drivers

The virus news stream is mixed; the dollar continues to consolidate; US-China tensions continue to rise. US Treasury wraps up its quarterly refunding; April budget statement is a harbinger of things to come; the next round of stimulus will be contentious. We got some dovish BOE comments yesterday; UK continues to play Brexit hardball; UK data was slightly better than expected but awful nonetheless.

Dollar Firm as Risk-off Sentiment Intensifies

Dollar Firm as Risk-off Sentiment Intensifies

Risk-off sentiment has intensified; as a result, the dollar is getting some more traction. Fed Chair Powell pushed back against the notion of negative rates in the US; US Treasury completed its quarterly refunding. Weekly jobless claims are expected at 2.5 mln vs. 3.169 mln last week; Mexico is expected to cut rates 50 bp to 5.5%

Restricted Market Trading Comments

Restricted Market Trading Comments

Covid-19 related measures for restricted markets remain largely unchanged this week. Philippines, Bangladesh and Kuwait have extended their lockdown periods, while Kenya and Nigeria continue to face limited liquidity. Please see trading comments below

FX Daily, May 12: Markets Tread Water, Looking for New Focus

FX Daily, May 12: Markets Tread Water, Looking for New Focus

Overview: Investors seem to be in want of new drivers, leaving the capital markets with little fresh direction. While Japanese and China equities were little changed, several markets in the region, including Australia, Hong Kong, Taiwan, and India, were off more than 1%. European bourses are mostly higher after the Dow Jones Stoxx 600 slipped 0.4% yesterday.

More Protectionism and Regulation Won’t Fix the Economy

More Protectionism and Regulation Won’t Fix the Economy

In the wake of the COVID-19 pandemic and its attendant economic strains, some protectionists and anti-immigration ideologues are trying to take advantage of this opportunity to advance their nationalist agenda. They argue that if the United States had restricted international trade and immigration more thoroughly in the past, as President Trump had fought to achieve, the public health crisis could have been curtailed.

Tags: Featured,newsletter