Spillover effects Turkey’s debt problem, coupled with the plummeting lira, is arguably the most important risk factor for the nation’s economy. To make matters worse, far from it posing a threat just to Turkey itself, it also has the potential to inflict significant damage elsewhere too, starting with key economies in the Eurozone. At first glance, the situation in Turkey might resemble many past similar scenarios of a heavily indebted nation with a plummeting currency that descends into a severe recession and eventually gets bailed out, like Greece. However, there is one key difference that makes Turkey’s debt problem much more complicated and potentially dangerous. Unlike Greece, Italy or other seriously debt-laden economies, it’s not just government borrowing that’s the main risk

Topics:

Claudio Grass considers the following as important: Economics, Finance, Gold, Monetary, Politics

This could be interesting, too:

Investec writes The Swiss houses that must be demolished

Claudio Grass writes The Case Against Fordism

Claudio Grass writes “Does The West Have Any Hope? What Can We All Do?”

Investec writes Swiss milk producers demand 1 franc a litre

Spillover effects

Turkey’s debt problem, coupled with the plummeting lira, is arguably the most important risk factor for the nation’s economy. To make matters worse, far from it posing a threat just to Turkey itself, it also has the potential to inflict significant damage elsewhere too, starting with key economies in the Eurozone.

At first glance, the situation in Turkey might resemble many past similar scenarios of a heavily indebted nation with a plummeting currency that descends into a severe recession and eventually gets bailed out, like Greece. However, there is one key difference that makes Turkey’s debt problem much more complicated and potentially dangerous. Unlike Greece, Italy or other seriously debt-laden economies, it’s not just government borrowing that’s the main risk here. Instead, it’s the unsustainable and increasingly unfinanceable corporate debt that makes Turkey a ticking time bomb and renders an IMF-rescue option problematic.

Private debt to GDP stands at a staggering 170%, while, overall, over half of the borrowing is denominated in foreign currencies. Thus, the collapse of the lira has made it extremely challenging for businesses to pay off or even service their debt, while the default risk has surged. Around $179 billion in external debt is due to mature until July 2019, which amounts to almost a quarter of the country’s annual economic output, according to JPMorgan estimates. Most of that, $146 billion, is owed by the private sector and banks in particular.

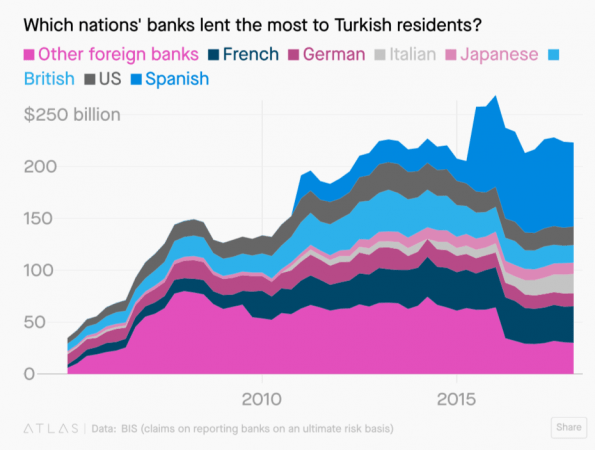

However dire the current debt predicament might seem for Turkey’s businesses and economic outlook, it is important to also consider the implications for its debtholders, especially since European banks feature prominently among them. In fact, the level of exposure in some cases is so worrying that it justifiably raises concerns that what happens in Turkey won’t just stay in Turkey.

Spain’s banking sector is one of very few in the European bloc that was so far considered not to be problematic; especially in comparison to Italian or Greek banks. However, the exposure of Spanish banks to Turkish debt means that the currency and debt woes of Europe’s neighbor have decisively challenged these assumptions. Spain’s second-biggest bank, BBVA, controls 49.9% of Turkish bank Garanti, which has already reported a rise in non-performing loans. Spanish banks also led the lending spree to Turkish businesses over the past years, rendering them vulnerable to the spiking default risk.

Although Spanish banks were by far the greatest lenders for Turkey, French, Italian and German banks also have significant exposure to Turkish debt. This already became problematic from the onset of the Turkish woes this past summer, when investors dumped Eurozone bank shares and prices suffered significant blows. Among the worst hit were BBVA, Unicredit, and PNB Paribas. Yet still, a blow to the stock price is nothing compared to the damage that a sustained currency crisis and rising default risk can inflict to the already vulnerable European banking sector.

Key lessons

Overall, Turkey’s woes are yet another important and timely reminder of the frailty of the current monetary system and of the banking sector, as well as of the systemic weaknesses and inevitable unsustainability of a centrally planned economy and of fiat money.

After all, the lira’s value, as that of any other fiat currency, depends on the trust the people place in its issuer. Once that is lost or even shaken, no measures and no force applied by the central planners can stabilize it. We saw that play out over the last months in Turkey, with the government trying a wide variety of approaches to control the currency’s fall, to no avail. That clearly demonstrated the flimsy and fickle nature of the entire system.

As the Turkish currency collapsed, demand for gold more than doubled in the country, while gold priced in lira reached all-time highs, as is to be expected in times of crisis. Erdogan’s public calls for citizens to sell the “gold under their pillows” and buy lira to help defend the country against the “economic attacks” from the outside were clearly ignored. Consumers flocked to the precious metal in response to the deteriorating fiat currency and gold imports to Turkey increased eightfold last December, while the Turkish central bank itself also dramatically increased its official reserves over the last two years.

As the country now joins the long list of nations that came to regret reckless interventionism and aggressive monetary manipulation, it also sends a strong message to those investors who are wise enough to heed it. In order to effectively prepare for the upcoming economic slowdown and all that it will bring, one needs to hedge against these inherent risks that are deeply embedded in our current system. While inflation, currency depreciations, volatile stock markets or a rise in toxic debt might be all we’ll see during the next downturn, nobody can be sure what the extent of the damage will be and whether it would be contained before threatening the banking system at large. Especially in Europe, the outlook is rather grim and the odds of a timely rescue are not favorable. As the central bank is already overstretched, after so many years of QE and negative interest rates, it is likely to lack the tools to fight the next recession and to limit its impact.

Turkey’s story can arguably be seen as a warning and as a cautionary tale. While governments and central banks will dismiss it, individual investors should not. Separating the signal from the noise has always been crucial in forming solid strategies and in planning for the future. At this stage, when the signs of a widespread economic slowdown can already be seen on the horizon, the necessity of a physical precious metals position is imperative for any responsible investor who wishes to preserve their wealth.

Claudio Grass, Hünenberg See, Switzerland

www.claudiograss.ch

Bildrechte: iStock.com/PashaIgnatov