Jeffrey P. Snider

October 10, 2019

SNB & CHF

I’ve said all along that they would be dragged into them kicking and screaming. After all, the Federal Reserve undertook its last rate hike in December 2018 – just as the markets were making clear he was completely mistaken in his view of the economy. What followed was the ridiculous “Fed pause” which pretty much everyone outside of the central bank and the Economics profession knew wasn’t the end of it.

You know the story. When he finally gave in at the end of July,...

Read More »

Jeffrey P. Snider

October 8, 2019

SNB & CHF

They remain just as confused as Richard Fisher once was. Back in ’13 while QE3 was still relatively young and QE4 (yes, there were four) practically brand new, the former President of the Dallas Fed worried all those bank reserves had amounted to nothing more than a monetary head fake. In 2011, Ben Bernanke had admitted basically the same thing.

But who was falling for it?

The stock market, sure.

Investors on Wall Street are still betting as if it will work any day...

Read More »

Jeffrey P. Snider

October 5, 2019

SNB & CHF

For the second time this week, the ISM managed to burst the bond bear bubble about there being a bond bubble. Who in their right mind would buy especially UST’s at such low yields when the fiscal situation is already a nightmare and becoming more so? Some will even reference falling bid-to-cover ratios which supposedly suggests an increasing dearth of buyers.

Bid-to-cover, however, is irrelevant. That only tells you about one part of the buying equation, the number...

Read More »

Jeffrey P. Snider

September 25, 2019

SNB & CHF

There’s been an unusual level of honesty coming out of Liberty Street of late. Not total honesty but certainly more than the usual nothing denials and dismissals. If you don’t immediately recognize the reference, that’s the street in NYC where FRBNY and its Open Market Desk resides. What is supposed to be the moneyed centered of the universe. After all, as Ben Bernanke famously threatened in November 2002, that’s the printing press.

Or is it?

In my own conversations...

Read More »

Jeffrey P. Snider

September 25, 2019

SNB & CHF

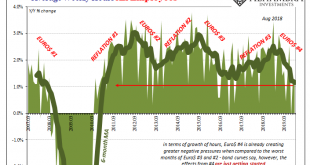

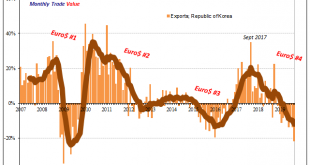

Engaged in one of those protectionist trade spats people have been talking about, the flow of goods between South Korea and Japan has been choked off. The specific national reasons for the dispute are immaterial. As trade falls off everywhere, countries are increasingly looking to protect their own. Nothing new, this is a feature of when prolonged stagnation turns to outright contraction.

While the dispute with Japan hasn’t helped, it isn’t responsible for the level...

Read More »

Jeffrey P. Snider

September 20, 2019

SNB & CHF

Jay Powell’s disastrous week is coming to a close, not yet his long nightmare. He has been battling fed funds (meaning repo) for his entire tenure dating back to February 2018. This week wasn’t the conclusion to the contest, just the latest and biggest round of it.

According to DTCC, the GC repo (UST) rate came back down to 1.975% today. That’s much less than the 3.000% yesterday and 6.007% on Tuesday. As yesterday, today’s unscheduled overnight repo operation...

Read More »

Jeffrey P. Snider

September 7, 2019

SNB & CHF

Federal Reserve policymakers appear to have grown more confident in their more optimistic assessment of the domestic situation. Since cutting the benchmark federal funds range by 25 bps on July 31, in speeches and in other ways Chairman Jay Powell and his group have taken on a more “hawkish” tilt. This isn’t all the way back to last year’s rate hikes, still a pronounced difference from a few months ago.

The common forecast relies entirely on the subjective...

Read More »

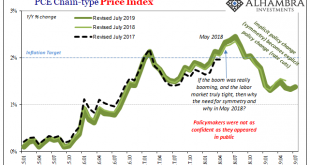

Jeffrey P. Snider

September 3, 2019

SNB & CHF

It isn’t inflation which is driving gold higher, at least not the current levels of inflation. According to the latest update from the Bureau of Economic Analysis, the Federal Reserve’s preferred inflation calculation, the PCE Deflator, continues to significantly undershoot. Monetary policy explicitly calls for that rate to be consistent around 2%, an outcome policymakers keep saying they expect but one that never happens.

For the month of July 2019, the index...

Read More »

Jeffrey P. Snider

August 15, 2019

SNB & CHF

If you like rate cuts and think they are powerful tools to help manage a soft patch, then there was good news in two international oil reports over the last week. The US Energy Information Administration (EIA) cut its forecast for global demand growth for the seventh straight month. On Friday, the International Energy Agency (IEA) downgraded its estimates for the third time in four months.

That wasn’t all, as the EIA’s report focused in on some more sobering aspects...

Read More »

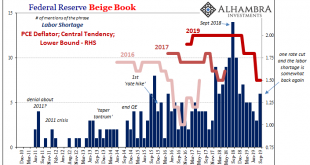

Jeffrey P. Snider

July 27, 2019

SNB & CHF

In the official narrative, the economy is robust and resilient. The fundamentals, particularly the labor market, are solid. It’s just that there has arisen an undercurrent or crosscurrent of some other stuff. Central bankers initially pointed the finger at trade wars and the negative “sentiment” it creates across the world but they’ve changed their view somewhat.

A few billion in tariffs, even if we include what is to...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org