We can also predict that the next round of instability will be more severe than the previous bout of instability. Everyone is in favor of “doing whatever it takes” to “restore financial stability” when the house of cards starts swaying, but funny things happen on the way to “Restoring Financial Stability.” Whatever “emergency measures” are rushed into service to “stabilize” an inherently unstable system resolve the immediate problem but opens unseen doors to new sources of instability that eventually trigger another round of systemic instability that must be addressed with more “emergency measures.” These unintended consequences proliferate as policy extremes are pushed to new extremes, and “emergency measures” become permanent sources of the very instability

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

We can also predict that the next round of instability will be more severe than the previous bout of instability.

Everyone is in favor of “doing whatever it takes” to “restore financial stability” when the house of cards starts swaying, but funny things happen on the way to “Restoring Financial Stability.” Whatever “emergency measures” are rushed into service to “stabilize” an inherently unstable system resolve the immediate problem but opens unseen doors to new sources of instability that eventually trigger another round of systemic instability that must be addressed with more “emergency measures.”

These unintended consequences proliferate as policy extremes are pushed to new extremes, and “emergency measures” become permanent sources of the very instability they were supposed to eliminate.

As @concodanomics recently observed on Twitter: “A major flaw of finance is that it nearly always mutates the very instruments meant to protect investors into crisis-inducing time bombs.”

Another major flaw in finance is the self-serving pressure applied by politically influential players to “enable innovation,” a.k.a. new opportunities for skims and scams. The usual covers for these “innovations” are 1) deregulation (“growth” will result if we let “markets” self-regulate) and 2) technology (generating guaranteed profits by front-running the herd is now technically possible, so let’s make it legal).

Broadening the pool of punters who can be skimmed and scammed is also a favored form of financial “growth” and “innovation.” “Democratizing markets” was the warm and fuzzy cover story for enabling everyone with a mobile phone to dabble in risk-on gambles with margin accounts (cash borrowed against a portfolio of stocks).

Mixing “innovation,” “democratizing markets” and “deregulation” enabled funny things like the FTX debacle, which admirably displayed every dynamic of our rickety tar-paper-shack of a financial system, a shelter that seems fine on a summer day but starts coming apart as soon as it rains: absurdly transparent influence-buying; Ponzi schemes presented as “innovative finance,” insider dealing, corruption, fraud, malfeasance, shrill proclamations of innocence, etc.

Unintended consequences have their own unintended consequences, a.k.a. second-order effects. So broadening the pool of people who qualified for a jumbo mortgage by lowering lending standards in the mid-2000s sounded very fine and progressive, i.e. “democratizing homeownership,” but handing out jumbo mortgages to uncreditworthy households ended up “democratizing” fraud on such a scale that the ensuing collapse almost took down the entire global financial house of cards.

To backstop the resulting mess, the Federal Reserve bought a couple trillion dollars of mortgage-backed securities and dropped mortgage rates to historic lows. These “saves” ended up (surprise!) inflating an even more extreme housing bubble which is currently popping, as all bubbles eventually do, with the usual devastating results to punters who were swept up in the “fear of missing out” frenzy that inflates bubbles.

| In real-time, it’s not that easy to discern how the latest policy “fixes” are creating new perverse incentives and opening new loopholes for insiders to exploit. While we may not have clarity on the specifics, we can confidently predict that the latest policies to “restore financial stability” will create new perverse incentives and open new loopholes which will lead to the next round of panicky instability.

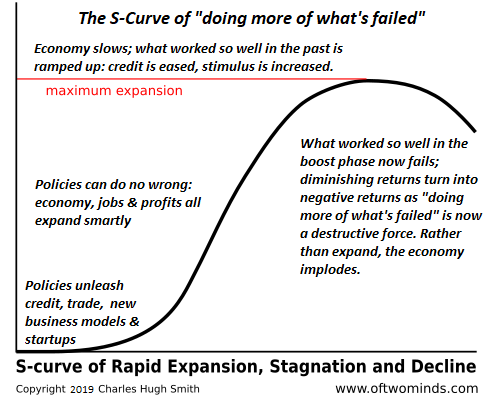

We can also predict that the next round of instability will be more severe than the previous bout of instability.This is what happens when the system starts sliding down the backside of the S-Curve, and doing more of what worked in the past transforms into doing more of what’s failed spectacularly. The irony is rather rich, isn’t it? The policies rushed into service to “restore financial stability” insure the next round of financial instability will be even harder to stabilize, until the instability undergoes a phase change that puts it out of reach of all stabilization policies. Yes, the tar-paper shack is full of cracks that are widening as it settles deeper into the swamp, but no worries, we’ve got some financial reports right here we can stuff into the cracks. A few more rounds of “innovation,” “democratizing markets” and policy “saves” and this place will be transformed into a palace, just you wait. |

. |

Tags: Featured,newsletter