The destruction of ‘phantom wealth’ via default has always been the only way to clear the financial system of unpayable debt burdens and extremes of rentier / wealth dominance. The notion that the world could always borrow more money as long as interest rates were near-zero was never sustainable. It was always an unsustainable artifice that we could keep borrowing ever larger sums from the future as long as the interest payments kept dropping. The only real solution to over-indebtedness since the beginning of finance is default. There are pretty names for variations on default that sound much less gut-wrenching–debt jubilees, refinancing, etc.– but the bottom line is the debts that can’t be paid won’t be paid and whomever owns the debt as an asset absorbs the

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The destruction of ‘phantom wealth’ via default has always been the only way to clear the financial system of unpayable debt burdens and extremes of rentier / wealth dominance.

The notion that the world could always borrow more money as long as interest rates were near-zero was never sustainable. It was always an unsustainable artifice that we could keep borrowing ever larger sums from the future as long as the interest payments kept dropping.

The only real solution to over-indebtedness since the beginning of finance is default. There are pretty names for variations on default that sound much less gut-wrenching–debt jubilees, refinancing, etc.– but the bottom line is the debts that can’t be paid won’t be paid and whomever owns the debt as an asset absorbs the loss.

Every default is a debt jubilee for the borrower. Whether the default is informal or formalized in bankruptcy, the debt payments are no longer being paid to the lender / owner of the debt.

| Every debt jubilee is a default that forces the owner of the debt to write the value down to zero and absorb the loss. The jubilation of the owner of the debt is rather muted unless the state swoops in and passes the losses onto the taxpayers via bailouts / transferring the losses to the public’s balance sheet.

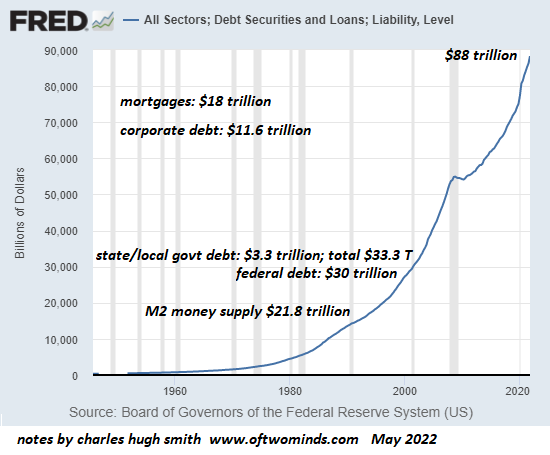

Every default is a refinancing–to zero. We’ve refinanced the debt so the borrower pays zero and the value of the loan / debt is now zero. Very few ordinary households own other people’s debts as assets. It’s the wealthy few who own most of the student loans, vehicle loans, mortgages, government and corporation bonds, etc. Yes, ordinary households may own other people’s debts through pension plans or ownership of mutual funds, but by and large debt is a favored asset of the rentier class, i.e. the wealthiest few. We’re constantly told that mass defaults would destroy the economy, but this is flim-flam: mass defaults would destroy much of the wealth of the rentier class which has been greatly enriched by the global expansion of debt, while freeing the debtors of their obligations. Recall that debt is the transfer of income from the borrower to the owner of the debt. Borrowing money is like every other form of consumption: when it’s cheap and abundant, we over-indulge. The costs are only apparent after the banquet has been cleared. The illusion that the global economy could effortlessly add trillions in debt to fund living large forever was based on a brief historical anomaly of zero interest rates enabled by low inflation. There’s a long lag between the vast expansion of debt / consumption and the eventual consequences on supply, demand, risk and price discovery. The lag time is up and now the consequences are finally visible: the tide of rapid growth in consumption and income required to fund ever-greater burdens of debt has ebbed, and so the global burden of debt–$300 trillion or so– is no longer sustainable / payable. |

. |

The favored solutions of the state–printing money or transferring the losses to the public–are no longer viable. Now that inflation has emerged from its slumber, printing trillions to bail out the wealthy is no longer an option. The public, so easily conned into accepting the bailout of the wealthy in 2008, has wised up and so that particular con won’t work again. (“Bail out the super-wealthy now or your ATM machine will stop working!” Uh, right.)

The state is the protector of the wealthy, and so defaults that actually impact the wealthy are anathema.The wealthy will demand the state absorb their losses (recall that profits are private, losses are socialized) The only equitable solution is to force the losses on those who bought the debt as a rentier income stream.

I’ve been exploring the Core-Periphery dynamic for a decade. (The E.U., Neofeudalism and the Neocolonial-Financialization Model May 24, 2012). This dynamic plays out in a number of ways on a number of levels.

Defaults will play out along the lines of Core-Periphery asymmetries. Some states will be able to “print their way out of default” but most will not, as unrestrained printing of money on such a vast scale would devalue the currency, triggering an even more destructive systemic default.

Debt is a double-edged form of power. Being able to borrow and spend huge sums is an absolutely fabulous way to expand corruption, bribes, exploitation of the powerless, bridges to nowhere and mindless over-consumption, but the habits formed by mindless expansion of debt to fund soaring wealth inequality don’t serve the indebted entities very well when default removes borrowing as a way to pay and play.

Living within one’s means–i.e. net income–is the only solution there has ever been to the end-game of over-indebtedness, i.e. default. Those with relatively secure, diversified net incomes (i.e. the Core) will do much better than those with unstable, limited income.

The destruction of phantom wealth via default has always been the only way to clear the financial system of unpayable debt burdens and extremes of rentier / wealth dominance. Let’s guess that a bare minimum of $100 trillion of the $300 trillion mountain of global debt will default far sooner than most expect. The only question is who will absorb the $100 trillion in losses. Choose wisely, as defaults of debt that are transferred to the public end up bringing down the entire system via political overthrow or currency collapse.

You Might Also Like

You Know What Would Be Really Irritating? A Crazy Rally to New Highs

You Know What Would Be Really Irritating? A Crazy Rally to New Highs

2022-07-08

It would be very irritating to have a rally suck in all the bears salivating for a crash from a bear-market rally peak and then decimate the shorts with a rally that soars rather than collapses to new lows. As a contrarian, I’m always squinting at the consensus and wondering if it is really that easy to be right.

The Age of Discord

The Age of Discord

2022-06-28

It’s very difficult to find common ground that supports cooperation in the disintegrative stage of scarcities, rising prices, catastrophically centralized power and social discord. Today’s topic echoes Peter Turchin’s 2016 book, Ages of Discord, which I have often referenced in blog posts.

Livelihoods in a Degrowth Economy

Livelihoods in a Degrowth Economy

2022-05-30

The sooner we start preparing for degrowth, the better off we’ll be. A Chinese proverb captures this succinctly: By the time you’re thirsty, it’s too late to dig a well. Let’s consider livelihood options in an unsustainable economy of extremes that are unraveling, an economy that is being forced to transition to Degrowth.

The Solution for Social Media Spam Bots Is Already Here

The Solution for Social Media Spam Bots Is Already Here

2022-05-23

The right of free speech should not be confused with an obligation for privately owned enterprises to allow spamming and spoofing under the guise of free speech. The problem of bots on Twitter is in the news. This is of course a problem in all social media: fake accounts, spamming accounts, spoofing (expropriating your identity) accounts, and so on, all courtesy of anonymous account creation.

The Epidemic Nobody Talks About: Burnout

The Epidemic Nobody Talks About: Burnout

2022-05-21

Burnout makes everyone uncomfortable, so it’s largely a silent epidemic. Epidemics are not just biological in origin. A strong case can be made that a silent epidemic has been sweeping the nation for years, an epidemic few acknowledge: burnout.

Curveballs in the Housing Bubble Bust

Curveballs in the Housing Bubble Bust

2022-05-16

All these curveballs will further fragment the housing market. Oh for the good old days of a nice, clean housing bubble and bust as in 2004-2011: subprime lending expanded the pool of buyers, liar loans and loose credit created speculative leverage, the Federal Reserve provided excessive liquidity and the watchdogs of the industry were either induced (ahem) to look away or dozed off in a haze of gross incompetence.

It’s All the Aliens’ Fault

It’s All the Aliens’ Fault

2022-04-03

As for our central banks’ defaulting on their lines of credit with the Martian Central Bank–that’s another

alien intervention we’ll live to regret.

I hope this won’t shock the more sensitive readers too greatly, but I’ve discovered undeniable evidence that all

our planet’s problems are the result of alien intervention. Yes, aliens exist and are actively intervening

in humanity’s activities, to our great detriment.

Wars, plagues, The Illuminati, the World Economic Forum, the Great Reset, locust swarms, mega-droughts,

endless spam, robo-calls, strange lights, billionaires’ cupidity, Windows 11, iOS 15,

the futility of trying to reach the IRS by phone,

the astounding rise of irrationality, that weird feeling of being watched and the grotesque decline of entertainment–

all are the

How Empires Die

How Empires Die

2022-02-08

When the state / empire loses the ability to recognize and solve core problems of security and fairness, it will be replaced by another arrangement that is more adaptable and adept at solving problems. From a systems perspective, nation-states and empires arise when they are superior solutions to security compared to whatever arrangement they replace: feudalism, warlords, tribal confederations, etc.

Tags: Featured,newsletter