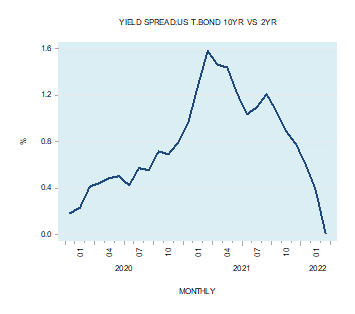

At the end of March this year the difference between the yield on the ten-year Treasury bond and the yield on the two-year Treasury bond fell to 0.010 percent from 1.582 percent at the end of March 2021. Many analysts believe that a change in the shape of the yield spread provides an indication regarding where the economy is heading in the months ahead, with an increase in the yield spread raising the likelihood of a possible strengthening in economic activity in the months to come. Conversely, a decline in the yield spread is seen as indicative of a possible economic downturn ahead. . A Popular Explanation for the Shape of the Yield Curve A popular explanation regarding the shape of the yield curve is provided by expectations theory (ET). According to ET, the

Topics:

Frank Shostak considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| At the end of March this year the difference between the yield on the ten-year Treasury bond and the yield on the two-year Treasury bond fell to 0.010 percent from 1.582 percent at the end of March 2021.

Many analysts believe that a change in the shape of the yield spread provides an indication regarding where the economy is heading in the months ahead, with an increase in the yield spread raising the likelihood of a possible strengthening in economic activity in the months to come. Conversely, a decline in the yield spread is seen as indicative of a possible economic downturn ahead. |

. |

A Popular Explanation for the Shape of the Yield Curve

A popular explanation regarding the shape of the yield curve is provided by expectations theory (ET). According to ET, the expectations for an increase in the short-term interest rate sets in motion an upward-sloping yield curve, while the expectations for the decline in the short-term interest rate sets the downward-sloping yield curve.

In the ET framework, the average of the current and expected short-term rates determines the current long-term rate. Thus, if today’s one year rate is 4.0 percent and next year’s one-year rate is expected to be 5.0 percent, then the two-year rate today should be 4.5 percent (4 + 5):2 = 4.5. Here, the long-term rate (i.e., the two-year rate today) is higher than the short-term (i.e., one year) rate. It follows that expectations for increases in short-term rates will make the yield curve upward sloping, since long-term rates will be higher than short-term rates.

Conversely, expectations for a decline in short-term rates will result in a downward-sloping yield curve because long-term rates will be lower than short-term rates. If today’s one-year rate is 4.0 percent and next year’s one-year rate is expected to be 3.0 percent, then the two-year rate today should be 3.5 percent (4+3):2=3.5. The long-term rate (i.e., the two-year rate today) is lower than the short-term rate.

According to the ET whenever investors start to anticipate economic expansion, they also begin to form expectations that the central bank will raise short-term interest rates by lifting the policy rate. To avoid capital losses, investors will move their money from long-term securities to short-term securities. (A rise in interest rates will have a greater impact on the prices of long-term securities versus short-term securities.) This shift will bid short-term securities prices up and their yields down. With respect to long-term securities, the shift of money away will depress their prices and raise their yields. Hence, we have here a decline in short-term yields and a rise in long-term yields—a tendency for an upward-sloping yield curve emerges.

Conversely, it is held that whenever investors expect an economic slowdown or a recession, they also start forming expectations that the central bank will lower short-term interest rates by lowering the policy rate. Consequently, investors will shift their money from short-term securities towards long-term securities. Thus, the selling of short-term assets will result in a fall in their prices and a rise in their yields. A shift of money towards long-term assets will result in the increase in their prices and a decline in their yields. Hence this shift in money raises short-term yields and lowers long-term yields—i.e., a tendency for a downward-sloping yield curve emerges.

Note again that in the ET framework, the formation of expectations regarding short-term interest rates determines long-term interest rates and, in turn, the shape of the yield curve. In the ET framework, given that the central bank determines short-term rates via the policy rate, it also follows that in the ET framework, interest rates—both short term and long term—are determined by the central bank. However, does the ET framework make sense?

Does the Central Bank Determine Interest Rates?

Note that contrary to the ET framework, interest rates are not determined by central bank monetary policy but by individual time preferences. The phenomenon of interest is the outcome of the fact that individuals assign a greater importance to goods and services in the present versus identical goods and services in the future. The higher valuation is because of capricious behavior, but rather the fact that life in the future is not possible without initially sustaining it in the present.

As long as the means at an individual’s disposal are sufficient to accommodate his immediate needs, he is most likely will assign less importance to future goals. With the expansion of the pool of means, the individual can now allocate some of those means towards the accomplishments of various ends in the future.

As a rule, with the expansion in the pool of means, individuals then are able to allocate more means towards the accomplishment of remote goals in order to improve their quality of life over time. (Individuals could lower their time preference.)

With paltry means, an individual can only consider very short-term goals, such as making a basic tool. The meager size of his means does not permit him to undertake the making of more advanced tools. With the increase in the means at his disposal, the individual could consider undertaking the making of better tools.

Prior to the expansion of wealth, the need to sustain life and wellbeing in the present has made it impossible to undertake various long-term projects, but with more wealth this now is possible. Note that very few individuals are likely to embark on a business venture, which promises a zero rate of return. The maintenance of the process of life over and above hand to mouth existence requires an expansion in wealth. The wealth expansion implies positive returns.

Note that the interest rate is only an indicator reflecting individual decisions regarding present versus future consumption. In a free market, fluctuations in interest rates will reflect changes in consumers’ time preferences. Thus, a decline in the interest rate is in response to the lowering of individuals’ time preferences. Consequently, when businesses observe a decline in the market interest rate, they respond by increasing investment in capital goods in order to be able to accommodate the likely increase in future consumer goods demand.

The Shape of the Yield Curve in an Unhampered Market

According to Ludwig von Mises, in a free market economy, the natural tendency of the yield curve is neither toward an upward-sloping nor toward a downward-sloping shape but rather toward being horizontal. (Observe that the horizontal yield curve emerges after adjusting for risk.) On this Mises wrote:

The activities of the entrepreneurs tend toward the establishment of a uniform rate of originary interest in the whole market economy. If there turns up in one sector of the market a margin between the prices of present goods and those of future goods, which deviates from the margin prevailing on other sectors, a trend toward equalization is brought about by the striving of businessmen to enter those sectors in which this margin is higher and to avoid those in which it is lower. The final rate of originary interest is the same in all parts of the market of the evenly rotating economy.1

Similarly, Murray Rothbard held that in a free market economy, an upward-sloping yield curve could not be sustained, for it would set in motion an arbitrage between short and long-term securities, as funds would be shifted from short maturities to long maturities. This would lift short-term interest rates and lower long-term interest rates, resulting in the tendency towards a uniform interest rate throughout the term structure. Arbitrage is likely to prevent the sustainability of a downward slopping yield curve by shifting funds from long maturities to short maturities thereby flattening the curve.2

Hence, in an unhampered market economy a prolonged upward- or downward-sloping yield curve cannot be sustained. What, then, is the mechanism that generates a sustained upward- or downward-sloping yield curve? We hold that the key factor for this is central bank tampering with financial markets by means of monetary policies.

How the Fed’s Tampering Alters the Shape of the Yield Curve

While the Fed can exercise control over short-term interest rates via the federal funds rate, it has lesser control over longer-term rates, since long-term rates reflect individual time preferences. The Fed’s monetary policies disrupt the natural tendency towards uniformity of interest rates along the term structure. This disruption leads to the deviation of short-term rates from the individuals’ time preferences rates as partially mirrored by the less manipulated long-term rate. This deviation in turn leads to the misallocation of resources and to the boom-bust cycle menace.

As a rule, Fed policy makers decide about the interest rate stance in accordance with the observed and the expected state of the economy and inflation. Thus, whenever the economy shows signs of weakness while the rate of increase of various price indexes begins to ease, investors in the market form expectations that the Fed in the upcoming months will lower its policy interest rate.

As a result, short-term interest rates begin to fall. The spread between the long-term rates and the short-term rates starts to widen—the process of the development of an upward-sloping yield curve is now set in motion. This process, however, cannot be maintained without the Fed’s actually lowering the policy interest rate. For the positive-sloped yield curve to be sustained, the central bank must persist with its easy stance. Should the central bank cease with its easy monetary policy the shape of the yield curve would tend to flatten.

At the same time, whenever economic activity shows signs of strengthening, coupled with a rise in price inflation, investors in the market form expectations that in the months ahead the Fed is going to lift its policy interest rate. As a result, short-term interest rates begin to move higher. The spread between the long-term rates and the short-term rates starts to decline—the process of the development of a downward-sloping yield curve is now set in motion. This process however, cannot be maintained without the Fed actually lifting the policy interest rate.

The downward-sloping yield curve emerges on account of a tighter monetary stance and can only be sustained if the Fed persists with its tighter monetary policy. Should the central bank abandon the tighter stance this would lead to the flattening of the yield curve. Note again that the Fed’s tampering with short-term interest rates distorts the natural tendency of the yield curve to gravitate towards the horizontal shape.

Why Changes in the Yield Curve Precede the Changes in the Pace of Economic Activity

Whenever the central bank reverses its monetary stance and alters the shape of the yield curve, it sets in motion either an economic boom or an economic bust. These booms and busts arise with a lag—they are not immediate. The reason for this is that the effect of a change in the monetary policy shifts gradually from one market to another market, from one individual to another individual. For instance, when the central bank during an economic expansion raises its interest rates and flattens the yield curve, the effect is minimal as economic activity is still dominated by the previous easy monetary stance. Only later on, once the tighter stance begins to dominate, that economic activity begins to weaken.

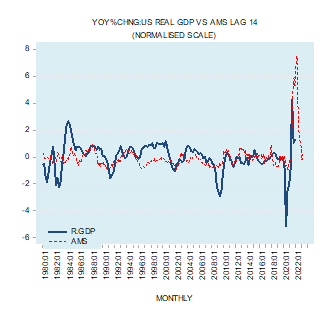

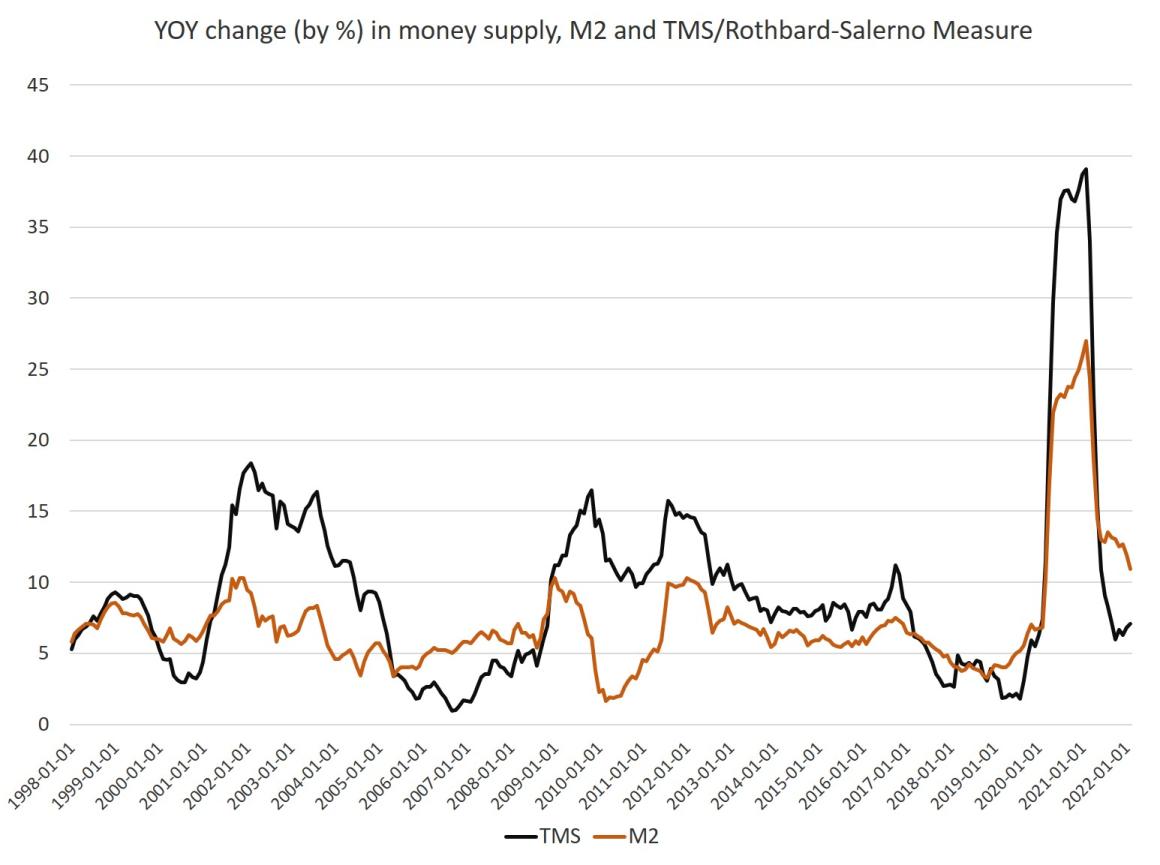

The Yield Spread and the Money Supply Growth RateAs a rule, an upward-sloping yield curve (because of the lowering of short-term interest rates by the Fed) is associated with a strengthening in the generation of money out of “thin air” and in the strengthening in the momentum of the Austrian money supply (AMS) measure. A downward slopping yield curve (because of the tighter interest rate stance by the Fed) is associated with a weakening in the pace of generation of money out of “thin air” and hence with a decline in the annual growth rate of AMS. This means that fluctuations in the momentum of AMS correspond to the relevant yield spread. Thus, a decline in the momentum of AMS, which corresponds to the downward-sloping yield curve, raises the likelihood that after a time lag a decline in economic activity will emerge. An increase in the momentum of AMS, which corresponds to the upward-sloping yield curve, raises the likelihood that after a time lag an increase in economic activity will take place. The yearly growth rate of real GDP (gross domestic product) closed at 5.5 percent in Q4 2021 against 4.9 percent in Q3 and –2.3 percent in Q4 2020. Based on the current downward-sloping yield curve and the corresponding downward momentum of AMS we can suggest that the annual growth rate of economic activity in terms of real GDP is likely to come under downward pressure in the months ahead (see chart). |

. |

Conclusion

A change in the shape of the yield curve emerges in response to Fed’s policy makers setting targets to the federal funds rate. We suggest that changes in the growth rate of money supply correspond to a given shape of the yield curve. An upward-sloping yield curve corresponds to a rising momentum of the money supply. The downward-sloping yield curve corresponds to the declining annual growth rate of money supply. Based on this we hold that currently a visible downtrend in the spread between the yields on the ten-year and the two-year Treasurys does not bode well for economic activity in the months ahead.

Again, we hold that both the upward- and the downward-sloping yield curves are the outcome of the central bank tampering with financial markets. This tampering results in the deviation of market interest rates from the time preference rates. Consequently, this results in the boom-bust cycle menace. We also suggest that in a free market without a central bank, after adjusting for risk, the shape of the yield curve is going to be neither upward nor downward sloping but rather horizontal.

- 1. Ludwig von Mises, Human Action, Third Edition, p. 536.

- 2. Murray Rothbard, Man, Economy, and State, Nash Publishing p. 384.

You Might Also Like

Money Supply Growth Heads Back Up: February Growth Up to 7 Percent

Money Supply Growth Heads Back Up: February Growth Up to 7 Percent

2022-04-07

Money supply growth rose for the third month in a row in February, continuing ongoing growth from October’s twenty-one-month low. Even with February’s rise, though, money supply growth remains far below the unprecedented highs experienced during much of the past two years.

Central Banks Have Broken the True Savings-Lending Relationship

Central Banks Have Broken the True Savings-Lending Relationship

2022-03-30

Most people believe lending is associated with money. But there is more to lending. A lender lends savings to a borrower as opposed to "just money." Let us explain. Take a farmer, Joe, who has produced two kilograms of potatoes. For his own consumption, he requires one kilogram, and the rest he agrees to lend for one year to another farmer, Bob. The unconsumed kilogram of potatoes that he agrees to lend is his savings.

Governments “Sanction” Their Own Citizens Every Day. The Russia Sanctions Are Just a Natural Evolution.

Governments “Sanction” Their Own Citizens Every Day. The Russia Sanctions Are Just a Natural Evolution.

2022-03-19

Russian president Vladimir Putin’s invasion of Ukraine in the last week of February 2022 was the culmination of decades of transnational statist expansion.

Behind Klaus Schwab, the World Economic Forum, and the Great Reset: Part 3

Behind Klaus Schwab, the World Economic Forum, and the Great Reset: Part 3

2022-03-11

Bob continues his series on Klaus Schwab and the Great Reset, highlighting an interesting remark in Biden’s SOTU, Strobe Talbott’s open support for global government, and the introduction to Schwab’s book on Covid-19 and the Great Reset.

Russian Weakness and the Russian “Threat” to the West

Russian Weakness and the Russian “Threat” to the West

2022-02-24

The current advocates for US aggression against Russia would have us believe that Russia is some sort of peer of the United States and of Western Europe.

Tom Rogan at the hawkish Washington Examiner, for example, insists that Russia is a "great power," presumably comparable to the United States in spite of Russia’s small economy.

Moreover, as Ted Galen Carpenter notes, hawks are fond are speaking of modern Russia as if it were pretty much the same thing as the Soviet Union, a state that was considerably larger and more populous than modern-day Russia. Unlike Russia, the Soviet Union was also founded on a totalitarian ideology.

Older readers might find that sort of thing to be plausible. After all, many people over a certain age are still living in the past, in the days of the Cold War, and

The Problem with “Stakeholder Capitalism”

The Problem with “Stakeholder Capitalism”

2021-11-11

Writing in the Investment Monitor on March 18, 2021, Klaus Schwab, the founder of the World Economic Forum, was urging the replacement of the present economic system. According to Schwab, the present system is deficient, since it only benefits a small minority of the population while leaving all the others at a visible disadvantage.

Amazing Street Singer | Street Song From Young Boy (Andrew Moran) | Genius Singer Performing #Shorts

Amazing Street Singer | Street Song From Young Boy (Andrew Moran) | Genius Singer Performing #Shorts

2021-11-09

#Shorts #street_performer #street_song #Genius_Singer

Please Subscribe The Singers Channel if you love his song and vocal

https://www.youtube.com/channel/UCHGKX4lBXMbAKm2KziLJvNQ

Bharat Kanodia: How Subjective Value Generates Valuation In Business

Bharat Kanodia: How Subjective Value Generates Valuation In Business

2021-10-31

All value is subjective. But often, when an exchange is to be made, a numerical value is required. It’s a special kind of economic calculation, what Bharat Kanodia terms “a subjective opinion based on objective facts”.

Bharat has built a career on valuations, from 2-founder garage start-ups to the Eiffel Tower. He shares his knowledge, experience, and insights with the Economics For Business podcast.

Tags: Featured,newsletter