The “yield curve” refers to a graph showing the relationship between the maturity length of bonds—such as one month, three months, one year, five years, twenty years, etc.—plotted on the x axis, and the yield (or interest rate) plotted on the y axis.1 In the postwar era, a “normal” yield curve has been upward sloping, meaning that investors typically receive a higher rate of return if they are willing to put their funds into longer-dated bonds. A so-called inverted yield curve occurs when this typical relationship flips, and short-dated bonds have a higher rate of return than long-dated ones. Investors and financial analysts are very interested in this phenomenon, because an inverted yield curve (defined in a particular way) has been a perfect leading indicator

Topics:

Robert P. Murphy considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The “yield curve” refers to a graph showing the relationship between the maturity length of bonds—such as one month, three months, one year, five years, twenty years, etc.—plotted on the x axis, and the yield (or interest rate) plotted on the y axis.1 In the postwar era, a “normal” yield curve has been upward sloping, meaning that investors typically receive a higher rate of return if they are willing to put their funds into longer-dated bonds. A so-called inverted yield curve occurs when this typical relationship flips, and short-dated bonds have a higher rate of return than long-dated ones.

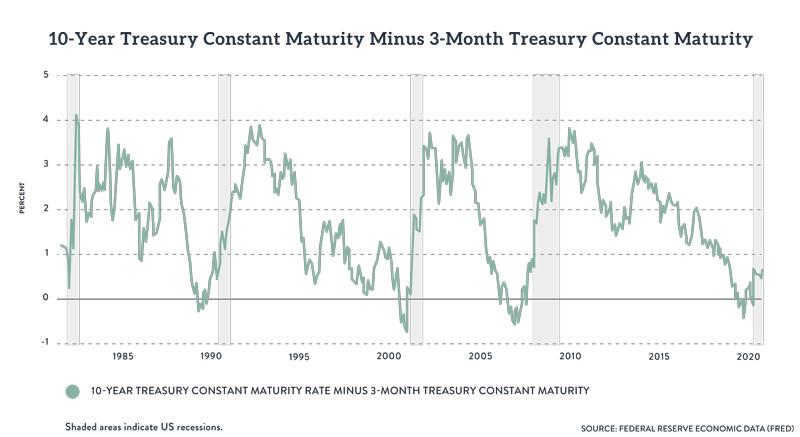

| Investors and financial analysts are very interested in this phenomenon, because an inverted yield curve (defined in a particular way) has been a perfect leading indicator of a recession going back at least fifty years. If we look at the last eight recessions, beginning with the downturn that began in December 1969, an appropriately defined yield curve inversion preceded all of them about a year ahead of time. Moreover, during this same fifty-one-year period the (appropriately defined) yield curve has only inverted when there would soon be a recession. (See the endnotes for citations to the scholarly literature.2) The following chart illustrates the yield curve’s apparent predictive power:

In the above chart (which only goes back to the early 1980s and so doesn’t cover the full extent of the yield curve’s successful track record), we have charted the difference (or “spread”) between the implicit interest rate on ten-year Treasury bonds and three-month Treasury bills. The normal state of affairs is for the yield on the longer ten-year security to be higher than the yield on the very short three-month security. (That’s why the line in the chart is typically above the black horizontal line at the 0 percent notch.) However, every once in a while the yield curve inverts, meaning that the line in the chart dips below the 0 percent threshold, corresponding to a situation in which the yield on three-month T-bills is actually higher than the yield on ten-year Treasury bonds. Notice in our chart that whenever that happens—and only when that happens—the economy soon goes into a recession (indicated by the gray bars). Economists have tried to explain the mechanism by which an inverted yield curve signals an impending recession. As we will see, the conventional attempts—such as the one offered by Paul Krugman—do not fit the actual facts. In contrast, the Misesian explanation of the business cycle quite easily explains the pattern we observe in interest rates during the “normal” boom time and shortly before the bust. |

. |

Paul Krugman on the Inverted Yield CurveIn his New York Times column and associated blogging platform, Paul Krugman over the years has clearly singled out investor expectations as the driving force behind the historical pattern. Here is Krugman in late 2008:

Then, in his column from mid-August of 2019—commenting on the then recent inversion of the two-year and ten-year yields, which was spooking investors—Krugman applied his framework to the data:

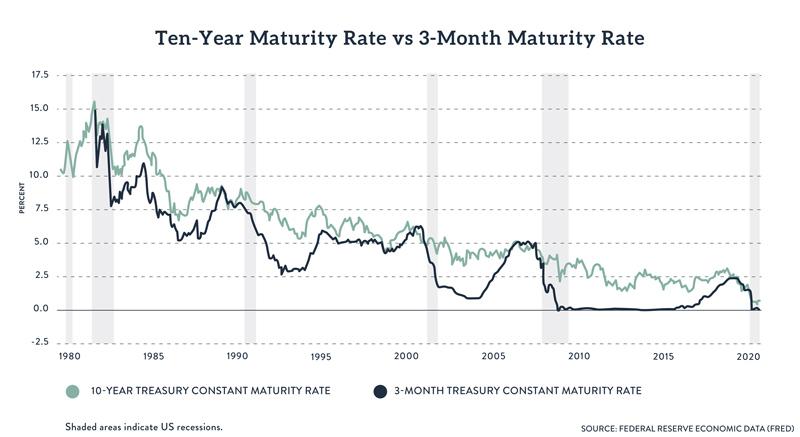

As the above quotations make clear, Krugman argues that the yield curve flattens/inverts before a recession because investors forecast trouble ahead. There are two problems with this approach. First, why would an inverted yield curve spook investors if the reason it inverts is that investors already know a recession is coming? Second and more significant: Krugman’s explanation would make sense if yield curve inversions typically occurred when the long bond yield collapses. But in fact, as the following chart makes clear, the yield curve inverts primarily because the short rate spikes upward before a recession: In the above chart, particularly for the middle three recessions, it is clear that the yield curve inverted because the three-month yield (black line) rose rapidly to surpass the ten-year yield (green line). This is the opposite of what Krugman’s readers would have expected to see. |

. |

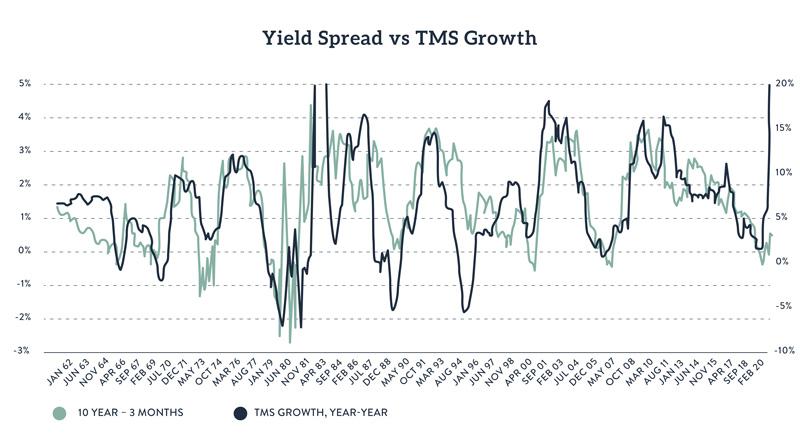

An Austrian ExplanationIn contrast to Krugman’s story, standard Austrian business cycle theory—which we explained in chapter 9—is quite compatible with the evidence presented in the above figure. In the Misesian framework, the unsustainable boom is associated with “easy money” and artificially low interest rates. When the banks (led by the central bank, in modern times) change course and tighten, interest rates rise and trigger the inevitable bust.5 (It is standard in macroeconomics to assume that the central bank’s actions affect short-term interest rates much more than long-term interest rates.) In fact, as Ryan Griggs and the present author have demonstrated, changing growth rates in the Austrian “true money supply” (TMS) monetary aggregate correspond quite well with the spread in the yield curve: In the above chart, the green line (corresponding to the left axis) is the difference between the ten-year Treasury bond yield and the three-month T-bill yield. The black line (corresponding to the right axis) is the twelve-month percentage growth in the true money supply as defined by Rothbard and Salerno (and which we briefly discussed in chapter 5). |

. |

As the chart indicates, these two series have a remarkably tight connection. Specifically, when the money supply grows at a high rate, we are in a “boom” period and the yield curve is “normal,” meaning the yield on long bonds is much higher than on short bonds. But when the banking system contracts and money supply growth decelerates, then the yield curve flattens or even inverts. It is not surprising that when the banks “slam on the brakes” with money creation, the economy soon goes into recession.

In summary, the standard Austrian explanation of the business cycle has, as a natural corollary, a straightforward explanation for the apparent predictive power of an inverted yield curve.

This article is adapted from Murphy’s 2021 book, Understanding Money Mechanics.

- 1. The material in this chapter draws on a forthcoming QJAE article authored by Ryan Griggs and Robert P. Murphy.

- 2. Perhaps the first systematic exploration of the inverted yield curve’s ability to forecast recessions was Campbell Harvey, “Recovering Expectations of Consumption Growth from an Equilibrium Model of the Term Structure of Interest Rates” (PhD diss., University of Chicago, 1986), https://faculty.fuqua.duke.edu/~charvey/Research/Thesis/Thesis.pdf. For a more recent discussion, see Arturo Estrella and Mary R. Trubin, “The Yield Curve as a Leading Indicator: Some Practical Issues,” New York Fed: Current Issues in Economics and Finance, July/August 2006, pp. 1–7, https://www.newyorkfed.org/medialibrary/media/research/current_issues/ci12-5.pdf.

- 3. See Paul Krugman, “The Yield Curve (Wonkish),” Paul Krugman blogs, New York Times, Dec. 27, 2008, https://krugman.blogs.nytimes.com/2008/12/27/the-yield-curve-wonkish/.

- 4. See Paul Krugman, “From Trump Boom to Trump Gloom,” New York Times, Aug. 15, 2019, https://www.nytimes.com/2019/08/15/opinion/trump-economy.html.

- 5. Paul Cwik’s work explains the inverted yield curve’s predictive power in light of Austrian business cycle theory. See for example Paul Cwik, “The Inverted Yield Curve and the Economic Downturn,” New Perspectives on Political Economy 1, no. 1 (2005): 1–37; and “An Investigation of Inverted Yield Curves and Economic Downturns,” (PhD diss., Auburn University, 2004).

You Might Also Like

Austrian Economists Are Not Surprised by the Shortages

Austrian Economists Are Not Surprised by the Shortages

2022-05-30

While supporters of the Biden administration fault Putin for shortages, Austrian economists know the answer lies in Washington’s monetary and economic mismanagement.

Peace through Strength? Excessive US Military Spending Encourages More War

Peace through Strength? Excessive US Military Spending Encourages More War

2022-05-28

The Russian invasion of Ukraine has brought America’s foreign policy interventions under the limelight once again. Ryan McMaken argues that the US administration’s claim that countries should not have the right to a sphere of influence, implicitly addressing Russia, is hypocritical.

Wie der Staat uns mit Inflation plündert

Wie der Staat uns mit Inflation plündert

2022-05-13

Ein Video von Thorsten Polleit, aufgenommen am 13. Mai 2022. | Thank you for your interest!

Thorsten Polleit: Kreditausfallrisiko jetzt extrem hoch

Thorsten Polleit: Kreditausfallrisiko jetzt extrem hoch

2022-03-11

▶︎ EINLADUNG ▶︎ „Die größten Gefahren für Ihr Vermögen“ – Online-Info-Veranstaltung

Hier gratis anmelden: https://bit.ly/3sgCZ02

▶︎ Abonnieren Sie hier unseren Kanal ▶︎ https://bit.ly/FinanzNEWS_abonnieren

▶︎ Prof. Thorsten Polleits Buch auf Amazon:

“Der Antikapitalist: Ein Weltverbesserer der keiner ist”

Hier bestellen: https://bit.ly/Thorsten-Polleit-auf-Amazon

Das könnte Sie auch interessieren:

▶︎ LEBENSVERLÄNGERUNG ▶︎ Die “Nie mehr altern”-Formel: https://bit.ly/3mdokfT

▶︎ HOCHPREIS-STRATEGIEN ▶︎ Raus aus dem Preiskampf: https://bit.ly/3a8mQ4k

#thorstenpolleit #finanznews #schattenregierung #ezb #herrscher

Thorsten Polleit (* 4. Dezember 1967) ist ein deutscher Chefökonom beim Degussa Goldhandel, Partner der Polleit & Riechert Investment Management LLP, Präsident und Gründer

Why Sanctions Don’t Work, and Why They Mostly Hurt Ordinary People

Why Sanctions Don’t Work, and Why They Mostly Hurt Ordinary People

2022-03-10

The United States and its western European allies have in recent days repeatedly increased economic sanctions against not only the Russian regime, but against millions of ordinary Russians.

Economic Knowledge Is Qualitative, Not Quantitative

Economic Knowledge Is Qualitative, Not Quantitative

2022-02-25

According to the popular way of thinking, our knowledge of the economy is elusive. Consequently, the best that we can do is to attempt to ascertain some facts of economic reality by applying various statistical methods to the so-called macro data.

The Case for the Austrian School of Economics | Per Bylund

The Case for the Austrian School of Economics | Per Bylund

2022-02-21

The Austrian School of Economics is gaining traction in business schools and the political sphere alike. Per Bylund, PhD, a Mises Fellow and associate professor of entrepreneurship at Oklahoma State University, explains the appeal of the Austrian School in that it offers an alternative means to understanding financial crises and how free markets work.

Vizlsa Silver (TSXV:VZLA | NYSE: VZLA) has discovered two new ore bodies in Napoleon and Tajitos, and the firm is expanding from 10 rigs to 13 rigs in 2022 for their newly consolidated project in Mexico, CEO Mike Konnert explains in our weekly sponsor segment.

Show notes: https://goldnewsletter.com/podcast/the-case-for-the-austrian-school-of-economics/

00:00 Intro

00:22 Podcast

16:30 Sponsor segment

23:35 Podcast

31:57 Outro

Is NATO a Dead Man Walking?

Is NATO a Dead Man Walking?

2022-02-21

While geopolitical commentators are fixated on Russia’s border with Ukraine, a more interesting development is slowly boiling underneath the surface of the Russo-Ukrainian conflict that could potentially reorder international relations—namely, the death of the North Atlantic Treaty Organization (NATO).

Tags: Featured,newsletter