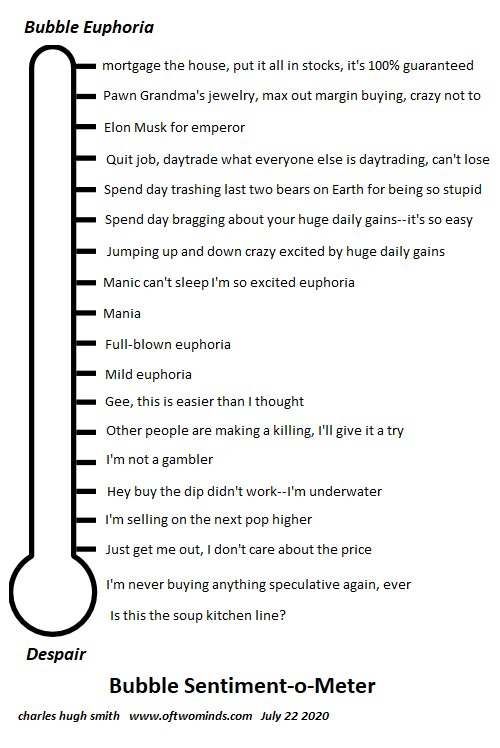

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted, liquidity is not guaranteed. The current market melt-up is taken as nearly risk-free because the Fed has our back, i.e. the Federal Reserve will intervene long before any market decline does any damage. It’s assumed the Fed or its proxies, i.e. the Plunge Protection Team, will be the buyer in any freefall sell-off: no matter how many punters are selling, the PPT will keep buying with its presumably unlimited billions. If this looks risk-free, ask who else will be “buying the dip” in a freefall? Former Fed Chair Alan Greenspan answered this question in his post-2008 crash essay Never Saw It Coming: Why the Financial Crisis Took Economists By Surprise (Dec. 2013 Foreign

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted, liquidity is not guaranteed.

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted, liquidity is not guaranteed.

The current market melt-up is taken as nearly risk-free because the Fed has our back, i.e. the Federal Reserve will intervene long before any market decline does any damage.

It’s assumed the Fed or its proxies, i.e. the Plunge Protection Team, will be the buyer in any freefall sell-off: no matter how many punters are selling, the PPT will keep buying with its presumably unlimited billions.

If this looks risk-free, ask who else will be “buying the dip” in a freefall? Former Fed Chair Alan Greenspan answered this question in his post-2008 crash essay Never Saw It Coming: Why the Financial Crisis Took Economists By Surprise (Dec. 2013 Foreign

Affairs): “They (financial firms) failed to recognize that market liquidity is largely a function of the degree of investors’ risk aversion, the most dominant animal spirit that drives financial markets. But when fear-induced market retrenchment set in, that liquidity disappeared overnight, as buyers pulled back. In fact, in many markets, at the height of the crisis of 2008, bids virtually disappeared.”

For the uninitiated, bids are the price offered to buyers of stocks and ETFs and the ask is the price offered to sellers. When bids virtually disappear, this means buyers have vanished: everyone willing to buy on the way down (known as catching the falling knife) has already bought and been crushed with losses, and so there’s nobody left (and no trading bots, either) to buy.

When buyers vanish, the market goes bidless, meaning when you enter your “sell” order at a specific price (limit order), there’s nobody willing to buy your shares at the current price. The shares remains yours all the way down.

If you decide to just get out at any price and place a market order (sell at whatever the bid is offered), your $100 per share stock might sell for $5 a share. This is known as a flash crash, and astute punters have observed that these are becoming more common.

When markets go bidless, the predictable order flow of low-volume days goes out the window. On a typical low volume day (and all days are low volume recently), the spread between bid and ask is modest in heavily traded issues and sellers can be confident their sell order will execute in a few seconds. In a freefall sell-off, sell orders pile up and the bid plummets to levels that were considered “impossible” in low-volume days.

What Greenspan didn’t discuss is the trading bots that do most of the trading have been programmed to be risk averse. In a real sell-off, why catch the falling knife by hitting the bid on the way down? That’s a guaranteed way to either lose money or ending up a bagholder.

Humans have a default setting for risk aversion: it’s called panic. Once the euphoric comnfidence that the Fed will never allow the market to fall by more than a few percentage points is broken, it’s not replaced by rational risk assessment; it’s replaced by full-blown just-get-me-out panic.

The Plunge Protection Team works just fine on low-volume days, but it fails when a tsunami of selling washes away the bid. Though few seemed to notice, massive selling volume begets more selling as the bots’ risk aversion kicks in.

Ironically, the mass migration of retail punters into the market has introduced a heightened potential for panic selling. The wild swings in Gamestock (GME) earlier in the year were a sneak preview of what can happen as panicked newbies enter market sell orders.

Euphoric punters forget that many of the players are leveraged, meaning that they’re using borrowed money (margin debt) to buy more stocks. Should the market drop instead of rebounding, their account will fall below minimum requirements and they will have to add cash or sell stocks. When buy the dip fails, those with margin calls add to the selling.

Other limits can manifest in cryptocurrency trading. When most trades are buys, few notice the fine print on exchange sell orders in crypto wallets and exchanges. Prices may be guaranteed for a limited time (for example, 10 minutes), and there may not be an option for limit orders. If the order doesn’t execute before the time limit expires, then the order to sell executes at whatever bid is offered.

There’s also no guarantee that your sell order will execute in a timely manner. A reader recently sent me a screenshot of an exchange of a top 100 (by market cap) cryptocurrency for Bitcoin that took almost 2 hours to execute. (The reader passed on using the Lightning Network after reading the disclosures.)

Exchanges may limit the number of coins per exchange. In other words, the implicit assumption that punters can unload their entire position at the current bid may prove unfounded in heavy sell volume days.

The point here is bottlenecks can emerge in heavy sell volume days that traders did not anticipate. The possibility that markets, brokerage platforms and exchanges could break and simply cease to function isn’t on anyone’s radar, despite various bits of evidence that a breakdown isn’t as farfetched as punters currently assume.

Ten minutes is more than enough time for supreme, euphoric confidence to crumble into panic, and trading bots can pull their buy orders in 10 milliseconds.

This is why the big players distribute their shares to overly confident retail punters over many weeks. Big players know there is no way they can dump their entire position without crushing the bid, so they sell in bits and pieces all the way up the euphoric melt-up.

The issue isn’t just the price you get when you sell–it’s being able to get out of your position at all. A strange phenomenon occurs in freefall sell-offs: the exit door (i.e. the liquidity that allows you to liquidate your entire position at the current bid) suddenly shrinks from a barndoor to a mouse-sized hole in the baseboard.

Nobody thinks a euphoric rally could ever go bidless, but as Greenspan belatedly admitted, liquidity is not guaranteed. In a real tsunami of trading-bot selling, the Plunge Protection Team’s card table is no match for the sea of selling.

Risk aversion can go from zero to 200 faster than overconfident punters believe possible.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-04-19

Update April 19 2021: SNB intervening. Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.2 bn. compared to last week.

The Tyranny Nobody Talks About

The Tyranny Nobody Talks About

2021-01-08

All the tricks to hide our unaffordable cost structure have reached marginal returns.

Reality is about to intrude.

There is much talk of tyranny in the political realm, but little is said about the tyrannies

in the economic realm, a primary one being the tyranny of high costs: high costs

crush the economy from within and enslave those attempting to start enterprises or keep their

businesses afloat.

Traditionally, costs are broken down into fixed costs such as rent and fees which don’t change

regardless of whether business is good or bad, and operating costs such as payrolls, fuel,

etc. which rise and fall with revenues.

To some degree, this division no longer matters, because the entire cost structure of our

economy is tyrannically high: if rent, insurance, taxes and general overhead

2020 the “Worst Year Ever”–You’re Joking, Right?

2020 the “Worst Year Ever”–You’re Joking, Right?

2020-12-29

So party on, because "the worst year ever" is ending and the rebound of financial markets, already the greatest in recorded history, will only become more fabulous.

2021 is Already Optimized for Failure

2021 is Already Optimized for Failure

2020-12-01

One sure way to identify a system “optimized for failure” is if all the insiders are absolutely confident the system is “optimized for my success”. I often discuss optimization here because it offers an insightful window into how systems become fragile and break down.

Our Frustrations Run Far Deeper Than Covid Lockdowns

Our Frustrations Run Far Deeper Than Covid Lockdowns

2020-11-25

The reality is the roulette wheel is rigged and only chumps believe it’s a fair game. It’s easy to lay America’s visible frustrations at the feet of Covid lockdowns or political polarization, but this conveniently ignores the real driver: systemic unfairness.

U.S. Healthcare Is Unraveling

U.S. Healthcare Is Unraveling

2020-11-19

The confidence that there will always be facilities and professionals to care for us is no longer realistic. I’ve covered the systemic problems of U.S. healthcare for over a decade, and as a result I’ve attracted numerous healthcare professionals as correspondents.

Prepare for Winter

Prepare for Winter

2020-11-16

Realism must precede optimism or the optimism will collapse as the tsunami of reality comes ashore. It’s time to prepare materially and psychologically for a winter unlike any other in our lifetimes.

Everything You Don’t Want to Know About Covid Vaccines (Because You Can’t Be Bullish Anymore)

Everything You Don’t Want to Know About Covid Vaccines (Because You Can’t Be Bullish Anymore)

2020-11-12

In such a highly polarized, politicized environment, is such a scrupulously objective study

even possible?

Now that we’ve had the happy-talk about Pfizer’s messenger-RNA (mRNA) vaccine (and

noted that Pfizer’s CEO sold the majority of his shares in the company immediately

after the happy-talk), let’s dig into messenger-RNA (mRNA) vaccines

which are fast approaching regulatory approval.

Some people have concluded vaccines are not safe, regardless of their source or mechanisms.

These people will never take any Covid vaccine.

Others will also decline a vaccine because they’ve concluded Covid is overblown.

Fair enough. But many other people conclude Covid is dangerous, partly because so little

is known about its long-term effects (Long-Covid, Long-Haulers). Covid’s low mortality

Tags: Featured,newsletter