The feedback loop has reversed: by saving more, people will spend, borrow and speculate less, draining the fuel from any broadbased expansion. In eras of confidence and certainty, people save less and spend more freely. When we’re confident that good times are not only here but will continue, we not only spend more freely, we’re more inclined to borrow money and speculate on the shimmering promises of more good times ahead. In eras of uncertainty, people save more and spend, borrow and speculate less. There is an obvious feedback loop here: if people feel confident about their future prospects and have a measure of certainty about the general economic trend, they spend more, borrow more and speculate more, all of which feed the expansive mood that then encourages

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The feedback loop has reversed: by saving more, people will spend, borrow and speculate less, draining the fuel from any broadbased expansion.

In eras of confidence and certainty, people save less and spend more freely. When we’re confident that good times are not only here but will continue, we not only spend more freely, we’re more inclined to borrow money and speculate on the shimmering promises of more good times ahead.

In eras of uncertainty, people save more and spend, borrow and speculate less. There is an obvious feedback loop here: if people feel confident about their future prospects and have a measure of certainty about the general economic trend, they spend more, borrow more and speculate more, all of which feed the expansive mood that then encourages further spending, borrowing and speculating.

If their confidence collapses and the future is deeply uncertain, people save more as a hedge against bad things happening in the economy that could trigger hardships in their own household.

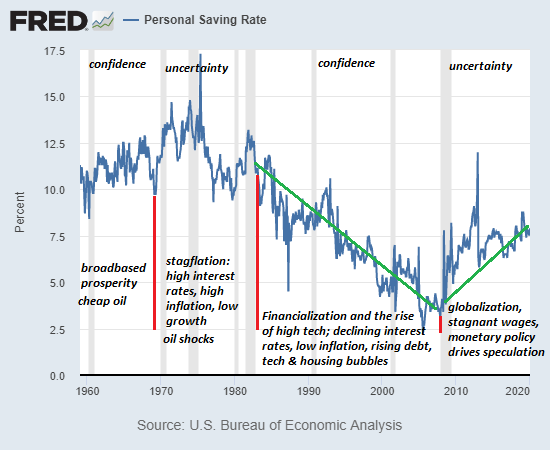

With this in mind, it’s interesting to look at a long-term chart of the U.S. savings rate, courtesy of the St. Louis Federal Reserve database (FRED). It’s easy to discern the waxing and waning of confidence / certainty in the decline or expansion of savings.

The broadbased prosperity of the 1960s is reflected in the high savings rate as cheap oil and real-world growth (as opposed to financial trickery and speculation) fattened paychecks while real-world inflation (cost of living) remained low.

The uncertainties of stagflation–oil shocks, recessions and soaring inflation and interest rates– pushed savings higher in the early 1970s. As purchasing power and speculative gains fell, so did the savings rate as households struggled to keep up with soaring costs of living.

Once inflation and speculative excess were wrung out, the stage was set for a 25-year expansion of “good times” powered by the financialization of the entire economy, the rise of high tech and the first stages of de-industrialization and offshoring, a.k.a. globalization.

Note that the savings rate popped higher after the 1991 oil-shock / Desert Storm recession and again after the dot-com bubble burst in 2000-02.

But the trend to save less and spend/speculate more continued until the the housing bubble burst, triggering the Global Financial Meltdown of 2008-09. When the dot-com bubble burst, the effects were largely confined to the tech sector and those who had speculated in the frenzy. But the housing bubble bursting had far wider consequences, as housing is the bedrock of household wealth and mortgages are the largest category of household debt.

The primary trick of financialization is to turn previously low-risk assets such as home mortgages into high-risk financial instruments that can be traded globally as “low-risk” assets. This fiction–greased by rampant fraud and institutionalized misrepresentation of risk–nearly brought down the global financial system when it finally unraveled.

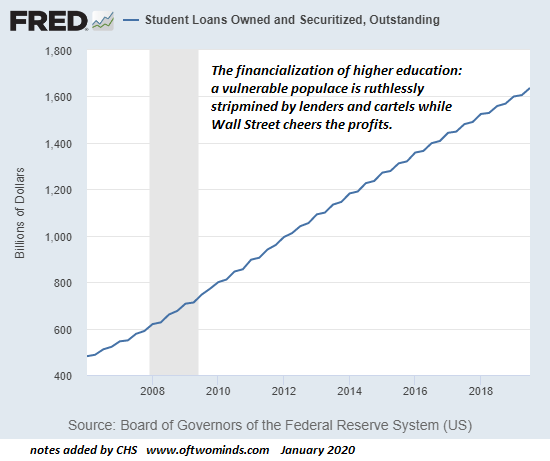

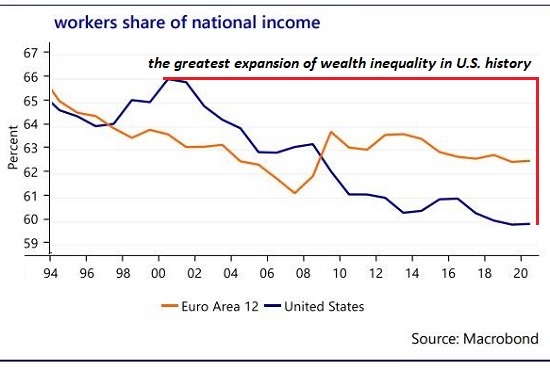

This globalization of financialization went hand in glove with the rapid expansion of offshoring and the hollowing out of real-world economies as the purchasing power of labor (wages) stagnated for all but the top tiers (top 5% and to a lesser degree, the top 10%) of technocrats, managers and entrepreneurs who rode the wave of globalization and technology.

|

To save the financial system from a well-earned collapse, central banks pushed monetary policies to unprecedented extremes, lowering interest rates and flooding the system with liquidity / stimulus. These extraordinary monetary policies boosted assets while leaving the real-world economy in decline as globalization stripmined local economies that could not compete with global corporations feasting on low interest rates, a steady decline in quality and quantity designed to increase profits and cheap overseas labor. Despite the thin gloss of “growth” this hyper-financialization generated, the stagnation of wages and real-world economy are reflected in the savings rate which has been steadily rising since 2009. The erosion of the real-world economy and the purchasing power of wages has sapped confidence in future prospects and ushered in an era of rising uncertainty. The economic-financial fallout from the Covid-19 pandemic is accelerating the loss of confidence and the rise of uncertainty that has been trending higher for over a decade. The feedback loop has reversed: by saving more, people will spend, borrow and speculate less, draining the fuel from any broadbased expansion. This is one reason why monetary policy extremes won’t revive growth, real or fictitious: the uncertainty that was launched in 2009 is only deepening. |

Personal Savings Rate, 1960-2020 - Click to enlarge |

You Might Also Like

The Global Repricing of Assets Can’t Be Stopped

The Global Repricing of Assets Can’t Be Stopped

All bubbles pop, period. The financial elites are pushing a narrative that asset prices, sales and profits will all return to January 2020 levels as soon as the Covid-19 pandemic fades. Get real, baby. Nothing is going back to January 2020 levels. Rather than the "V-shaped recovery" expected by Goldman Sachs et al., the crash in asset prices will eventually gather momentum.

The System Will Not Return to “Normal,” and That’s Good; We Can Do Better

The System Will Not Return to “Normal,” and That’s Good; We Can Do Better

Essential home lockdown reading. The pandemic is revealing to all what many of us have known for a long time: the status quo was designed to fail and so its failure was not just predictable but inevitable. We’ve propped up a dysfunctional, wasteful and unsustainable system by pouring trillions of dollars in borrowed money down a multitude of ratholes to avoid a reckoning and a re-set.

Helicopter Money: Short-Term Relief Won’t Cure our Financial Disease

Helicopter Money: Short-Term Relief Won’t Cure our Financial Disease

The collateral supporting the global mountain of debt is crumbling as speculative bubbles deflate. A great many freebies are being tossed in the Helicopter Money basket. That households experiencing declines in income need immediate support is obvious, as is the need to throw credit lifelines to small businesses.

Economic Decay Leads to Social and Political Decay

Economic Decay Leads to Social and Political Decay

If we want to make real progress, we have to properly diagnose the structural sources of the rot that is spreading quickly into every nook and cranny of the society and culture. It seems my rant yesterday (Let Me Know When It’s Over) upset a lot of people, many of whom felt I trivialized the differences between the parties and all the reforms that people believe will right wrongs and reduce suffering.

What We’ve Lost

What We’ve Lost

This is only a partial list of what we’ve lost to globalism, cheap credit and the Tyranny of Price which generates the Landfill Economy. A documentary on the decline of small farms and the rural economy in France highlights what we’ve lost in the decades-long rush to globalize and financialize everything on the planet– what we call Neoliberalism, the ideology of turning everything into a global market controlled by The Tyranny of Price and cheap credit issued to corporations and banks by central banks.

The Hour Is Getting Late

The Hour Is Getting Late

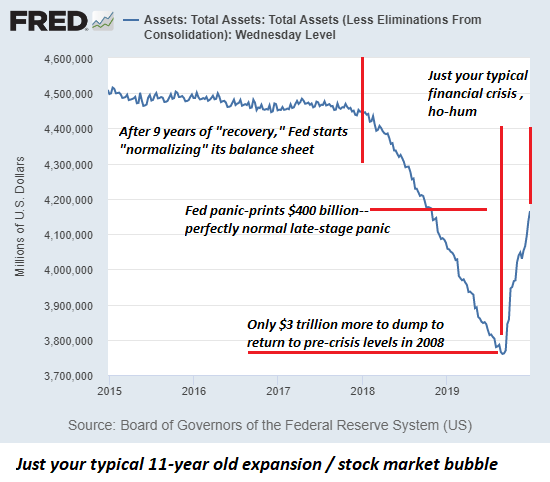

After 11 years of “the Fed is the market” expansion, the Fed has now reduced its bloated balance sheet by 6.7%. This is normal, right? So here we are in Year 11 of the longest economic expansion/ stock market bubble in recent history, and by any measure, the hour is getting late, to quote Mr. Dylan: So let us not talk falsely nowthe hour is getting lateBob Dylan, “All Along the Watchtower”

Pandemic, Lies and Videos

Pandemic, Lies and Videos

Will we wonder, what were we thinking? and marvel anew at the madness of crowds? When we look back on this moment from the vantage of history, what will we think? Will we think how obvious it was that the coronavirus deaths in China were in the tens of thousands rather than the hundreds claimed by authorities?

What the Fed Can Do: Print and Buy, Buy, Buy

What the Fed Can Do: Print and Buy, Buy, Buy

Everyone with a pension fund or 401K invested in stocks better hope the Fed becomes the buyer of last resort, and soon. Much has been written about what the Federal Reserve cannot do: it can’t stop the Covid-19 pandemic or reverse the economic damage unleashed by the pandemic.

Tags: Featured,newsletter