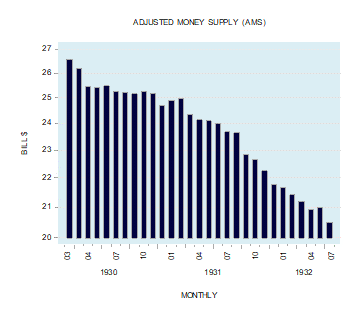

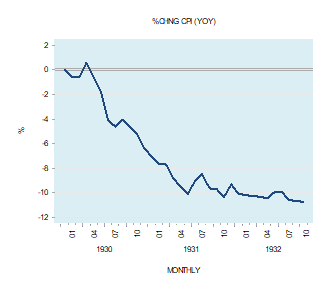

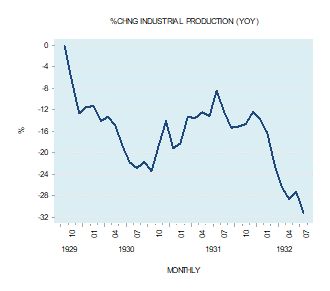

In his writings, Milton Friedman blamed central bank policies for causing the Great Depression. According to Friedman, the Federal Reserve failed to pump enough reserves into the banking system to prevent a collapse in the money stock.1 The adjusted money supply (AMS), which stood at .6 billion in March 1930, had fallen to .5 billion by April 1933—a decline of 22.9 percent.2 According to Friedman, as a result of the collapse in the money stock, economic activity followed suit. Thus, by July 1932 year-on-year industrial production had fallen by over 31 percent (see chart). Also, year-on-year the Consumer Price Index (CPI) had plunged. By October 1932 the CPI was down 10.7 percent (see chart). A close examination of the historical data shows that the Fed

Topics:

Frank Shostak considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| In his writings, Milton Friedman blamed central bank policies for causing the Great Depression. According to Friedman, the Federal Reserve failed to pump enough reserves into the banking system to prevent a collapse in the money stock.1 The adjusted money supply (AMS), which stood at $26.6 billion in March 1930, had fallen to $20.5 billion by April 1933—a decline of 22.9 percent.2 |  |

| According to Friedman, as a result of the collapse in the money stock, economic activity followed suit. Thus, by July 1932 year-on-year industrial production had fallen by over 31 percent (see chart). Also, year-on-year the Consumer Price Index (CPI) had plunged. By October 1932 the CPI was down 10.7 percent (see chart). |  |

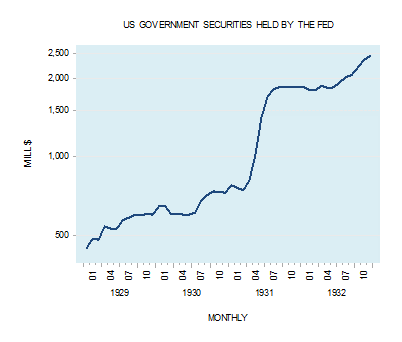

| A close examination of the historical data shows that the Fed was actually extremely loose and pumped reserves into the system in its attempt to revive the economy.3 The extent of the reserve pumping is depicted by the Fed’s holdings of US government securities: in January 1929 these holdings stood at $446 million, but by December 1932 they had jumped to $2.437 billion—an increase of 446.4 percent (see chart). |

|

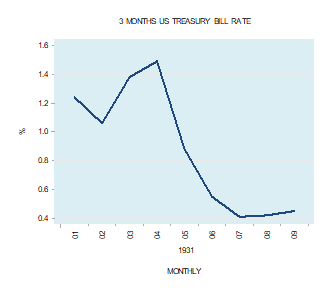

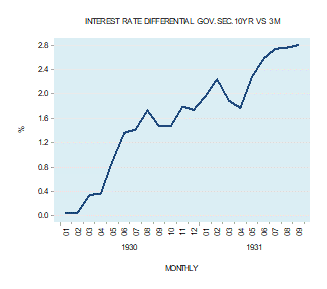

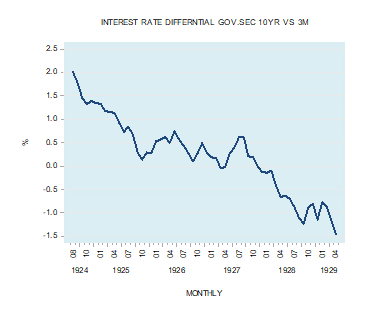

| Also, the three-month Treasury bill rate fell from 1.5 percent in April 1931 to 0.4 percent by July 1931 (see chart). Another indication of a loose monetary stance on the part of the Fed was the widening in the differential between the yield on the ten-year T-Bond and the three-month Treasury bill. The differential rose from 0.04 percent in January 1930 to 2.80 percent by September 1931 (see chart). |  |

|

|

| The sharp fall in the money stock from 1930 to 1933 is not indicative of the Federal Reserve’s failure to pump money. Instead, it is indicative of a shrinking pool of real savings brought about by the previous loose monetary policies of the central bank.

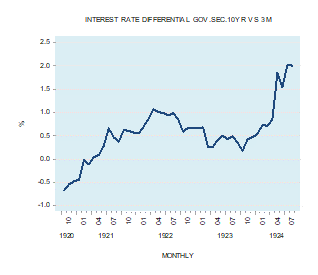

Indeed, the yield spread increased from –0.67 percent in October 1920 to 2 percent by August 1924 (an upward sloping yield curve indicates loose monetary stance) (see chart). |

|

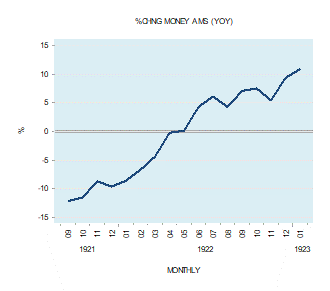

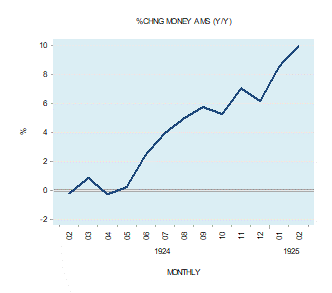

| In addition to this, at some stages monetary injections were massive. For instance, the yearly growth rate of AMS jumped from –12.1 percent in September 1921 to 10.9 percent by January 1923.

Then, from –0.2 percent in February 1924, the yearly growth rate accelerated to 9.9 percent by February 1925. Such large monetary pumping amounted to a massive exchange of nothing for something and to a severe depletion of the pool of real savings needed to sustain economic growth. |

|

|

|

| As long as the pool of real savings is expanding and banks are eager to expand credit (credit out of “thin air”), various nonproductive activities continue to prosper. Whenever the extensive creation of credit out of “thin air” lifts the pace of real wealth consumption above the pace of real wealth production, the flow of real savings is arrested and a decline in the pool of real savings is set in motion.

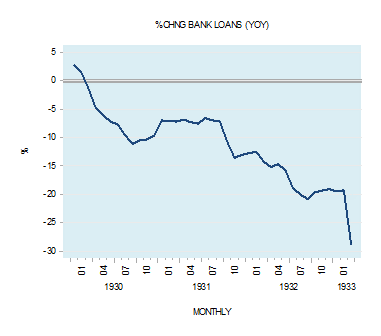

Consequently, the performance of various activities starts to deteriorate and banks’ bad loans start to rise. In response to this, banks curtail their lending activities and this in turn sets in motion a decline in the money stock. In this regard, after growing by 2.7 percent year on year in January 1930, bank loans had fallen by a massive 29 percent by March 1933 (see chart). |

|

| How can credit out “of thin air” lead to the disappearance of money? When loaned money is fully backed by savings, on the day of the loan’s maturity it is returned to the original lender. Thus, on the maturity date Bob—the borrower of $100—will pay back the borrowed sum and interest to the bank. The bank in turn will pass to Joe, the lender, his $100 plus interest adjusted for bank fees.

To put it briefly, the money makes a full circle and goes back to the original lender. When credit is created out of “thin air” and returned to the bank on the maturity date, this amounts to a withdrawal of money from the economy, i.e., to a decline in the money stock. The reason for this is that there was not any original saver/lender since this credit was created out of “thin air.” Economic depressions are not caused by the collapse in the money stock but come in response to a shrinking pool of real savings on account of the previous easy monetary stance of the central bank. |

|

| Consequently, even if the central bank were to be successful in preventing the fall of the money stock, this would not be able to prevent a depression if the pool of real savings is declining. Also, even if loose monetary policies were to succeed in lifting prices and inflationary expectations, this would not revive the economy as long as the pool of real savings is declining.

Note again that contrary to popular thinking, depressions are not caused by tight monetary policies, but are rather the result of previous loose monetary policies. On the contrary, a tighter monetary stance arrests the depletion of the pool of real savings and thereby lays the foundations for economic recovery. Furthermore, the tighter stance reveals the damage that previous loose monetary policies did to the capital structure. As the chart below shows, a tighter monetary policy (depicted by the downward-sloping yield curve) from August 1924 to May 1929, exposed the damage inflicted to the capital structure because of the previous loose monetary stance of the Fed. |

|

Conclusion

The Great Depression of 1930s occurred because of the Fed’s loose monetary stance from October 1920 to August 1924, which undermined the pool of real savings. The sharp fall in the money supply from 1930 to early 1933 was in response to the collapse of this pool. The sharp decline in various key economic indicators was also in response to the decline in the pool of real savings. The Fed made strong attempts to lift the money supply by aggressively expanding its balance sheet. These attempts, however, failed because banks curtailed the expansion of credit out of “thin air.” The reason for this curtailment was the shrinking pool of real savings—the heart of economic growth—that undermined the quality of banks assets.

- 1. Milton Friedman and Rose Friedman, Free to Choose: A Personal Statement (Orlando, FL: Harcourt, 1980), p. 85.

- 2. Frank Shostak, “The Mystery of the Money Supply Definition,” Quarterly Journal of Austrian Economics 3 (Winter 2000): 69–76.

- 3. Murray N. Rothbard, America’s Great Depression (Kansas City: Universal Press, 1963), p. 153.

You Might Also Like

A Rothbardian Analysis of the Constitutional Convention

A Rothbardian Analysis of the Constitutional Convention

Relates to Murray Rothbard’s Conceived in Liberty, Volume V: The New Republic, 1784-1791 and my forthcoming book, Liberty versus Power: A History of Cronyism in the United States, 1607-1849 (2021?)

How Central Banks Destroy Money’s Purchasing Power

How Central Banks Destroy Money’s Purchasing Power

Without a monopolist central bank, market forces would restrain the issuance of bank notes. But once central banks monopolize money creation, wealth is systematically transferred to the central bank and the privileged few who are favored by the state.

There Are No Winners in the US-China “Tech War”

There Are No Winners in the US-China “Tech War”

After unleashing a disruptive trade conflict with China, the Trump administration has also escalated the lingering “cold tech war” between the two rival powers. Over the last two years, the US has passed new rules limiting China’s investments in the US, restricting bilateral information and communications technology (ICT) trade and controlling exports of sensitive and emerging technology to China.

Political Self-Determination and the Nagorno-Karabakh Conflict

Political Self-Determination and the Nagorno-Karabakh Conflict

The right of self-determination in regard to the question of membership in a state thus means: whenever the inhabitants of a particular territory, whether it be a single village, a whole district, or a series of adjacent districts, make it known, by a freely conducted plebiscite, that they no longer wish to remain united to the state to which they belong at the time, but wish either to form an independent state or to attach themselves to some other state, their wishes are to be respected and complied with.

The Global Jobless Recovery

The Global Jobless Recovery

The United States added 1.76 million Jobs in July 2020, compared to a consensus estimate of 1.48 million. Unemployment fell to 10.2 percent versus the 10.6 percent expected.

Why Economics Cannot Be Understood through Experimentation

Why Economics Cannot Be Understood through Experimentation

In the natural sciences, a laboratory experiment can isolate various elements and their movements. There is no equivalent in the discipline of economics. The employment of econometrics and econometric model building is an attempt to create a laboratory where controlled experiments can be conducted.

On Foreign Policy, Trump Is Still the Lesser Evil

On Foreign Policy, Trump Is Still the Lesser Evil

The Democrats, Liz Cheney, and the Never Trumpers still want endless wars, and they hate Trump’s apparent lack of enthusiasm for embracing their dreams of empire.

This Audio Mises Wire is generously sponsored by Christopher Condon. Narrated by Michael Stack.

Original Article: "On Foreign Policy, Trump Is Still the Lesser Evil".

James Mill: Laissez-Faire’s Lenin

James Mill: Laissez-Faire’s Lenin

[An Austrian Perspective on the History of Economic Thought (1995)]

James Mill (1771–1836) was surely one of the most fascinating figures in the history of economic thought. And yet he is among the most neglected. Mill was perhaps one of the first persons in modern times who might be considered a true "cadre man," someone who in the Leninist movement of the next century would have been hailed as a "real Bolshevik." Indeed, he was the Lenin of the radicals, creating and forging philosophical radical theory and the entire philosophical radical movement.

A brilliant and creative but an insistently Number 2 man, Mill began as a Lenin seeking his Marx. In fact, he simultaneously found two "Marxes," Jeremy Bentham and David Ricardo. He met both at about the same time, at the age of 35, Bentham

Tags: Featured,newsletter