Christine Lagarde, the new president of the European Central Bank (ECB), has added a new green dimension to monetary policymaking. The charming Frenchwoman signaled that the ECB could buy green bonds, possibly as part of the reanimated bond purchase program (a form of QE). This could reduce the financing costs of green investment projects. If interest rates were negative, the green bond purchases would even amount to a subsidy for climate-friendly investment. This could strengthen environmental protection in times of tight expenditure constraints for overindebted governments. However, from an Austrian overinvestment perspective, low interest rates can contribute to a waste of resources. First, according to Hayek (1931), the too-low interest rates set by central

Topics:

Gunther Schnabl considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Christine Lagarde, the new president of the European Central Bank (ECB), has added a new green dimension to monetary policymaking. The charming Frenchwoman signaled that the ECB could buy green bonds, possibly as part of the reanimated bond purchase program (a form of QE). This could reduce the financing costs of green investment projects. If interest rates were negative, the green bond purchases would even amount to a subsidy for climate-friendly investment. This could strengthen environmental protection in times of tight expenditure constraints for overindebted governments. However, from an Austrian overinvestment perspective, low interest rates can contribute to a waste of resources.

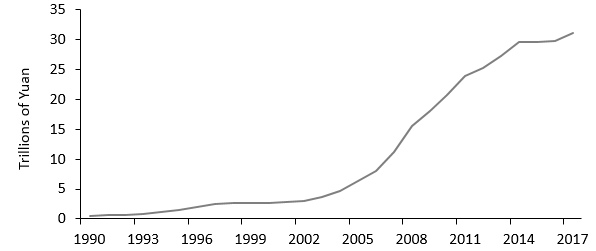

First, according to Hayek (1931), the too-low interest rates set by central banks can trigger unsustainable investment booms and speculation. When interest rates are lifted again, low-return investments have to be dismantled and bubbles burst. Mobilizing capital, labor, and raw materials during the upswing for investment projects with low marginal productivity, which have to be dismantled during the downswing, is a tremendous waste of resources. For example, between 2001 and 2007 strong interest rate cuts by the Fed and the ECB in response to the bursting of the dotcom bubbles triggered hiking real estate prices and construction booms in the United States and the Southern Eurozone area. As real estate owners felt richer and wages increased, consumption booms followed. After the end of the exuberance, abandoned construction sites and large vacancies were left. Furthermore, after the turn of the millennium, the sharp interest rate cuts in the industrialized countries led to huge capital outflows to China. With the Chinese central bank’s exchange rate fixed to the dollar, the capital inflows inflated the balance sheet of the People’s Bank of China (see Figure 1), which created large amounts of cheap credit there (McKinnon and Schnabl, 2012). Because the credit was preferentially allocated to large, export-oriented enterprises via the state-owned banking sector, large additional capacities in manufacturing were created (Schnabl, 2019). Between 2001 and 2014, Chinese manufacturing expanded by 275 percent in terms of value added. In addition, a real estate boom developed, with huge ghost towns being built. |

People's Bank of China Balance Sheet Source: People's Bank of China. - Click to enlarge |

| The large additional capacities in the industrial sector were partially created in the production of everyday consumer goods such as toys, decorative items, small furniture, and apparel. Many of these goods are only bought by consumers in industrialized countries, because they are cheap thanks to the People’s Bank of China’s low-cost credit and exchange rate stabilization (Dooley et al., 2004). At the same time, the low-interest-rate policies in the industrialized countries stimulated the propensity to consume, because household saving was discouraged and fast-rising asset prices lifted the costs of wealth formation.

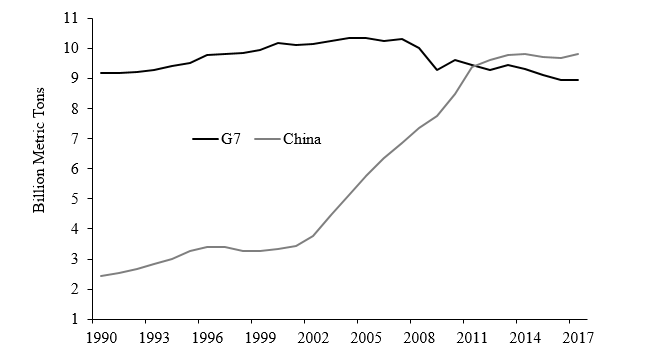

After the Chinese investment boom ended in 2014, with capital now leaving China, the low-return investment projects would have needed to be dismantled. Yet the People’s Bank of China keeps them afloat by continuing to provide low-cost credit to avoid unemployment (Schnabl, 2019). Second, between 2001 and 2014 Chinese and global CO2 emissions hiked. According to Huang et al. (2018), about 20 percent of global CO2 emissions originate in the construction sector. In addition, because about 60 percent of Chinese CO2 emissions are caused by manufacturing (Liu et al., 2019), the Chinese investment boom inflated global CO2 emissions (see Figure 2). Whereas between 1990 and 2000 Chinese CO2 emission grew on average by 3.4 percent per year, average annual growth increased to 8.8 percent between 2001 and 2014 (Figure 2). Since the end of the investment boom in 2014, the growth rate of Chinese CO2 emissions has flattened. |

Annual CO2 Emissions of Group of Seven (G7) and China |

| Since the turn of the millennium, the accelerating reallocation of CO2-intensive production from the industrialized countries to China — where environmental standards are less stringent — is likely to have contributed to hiking Chinese CO2 emissions.1 Out of the global increase in CO2 emissions from 25.1 billion metric tons in 2001 to 35.5 in 2014 (10.4 billion metric tons), China contributed 6.4 billion metric tons.

In contrast, the CO2 emissions of the G7 countries slightly fell during this period (Figure 2). When the Chinese investment boom ended in 2014, Chinese CO2 emissions also stopped growing. Third, to prevent the dismantling of low-return investment projects during crisis, the central banks in the large industrial countries have cut interest rates sharply and have continued to maintain low rates since 2009. According to Hayek (1931), such policies have a negative impact on labor productivity growth. This phenomenon is also dubbed zombification (see Adalet McGowan et al., 2017). With labor productivity gains converging towards zero in most industrialized countries, real wages of growing parts of the populations have come under pressure. This trend is most pronounced in Japan, where the real-wage level has been falling since 1998. Also, real interest rates on savings, another source of income, have become negative. The erosion of real incomes can be assumed to have boosted demand for cheaper products. Therefore, agricultural production is still dominated by environmentally harmful — often plastic-intensive — mass production. The proportion of plastic components in everyday goods has also risen, for example in the case of furniture, cars,2 clothing, and houses.3 As the lifespan of products is often shortened, the consumption of resources is raised since products are replaced earlier. |

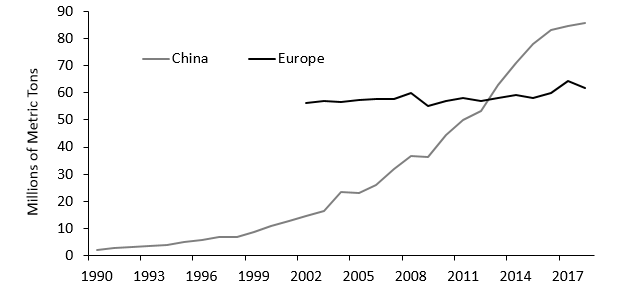

Plastic Production in China and Europe Source: Statista; National Bureau of Statistics of China. - Click to enlarge |

Also, service has tended to be gradually reduced. If individual service is substituted by self-service in the case of coffee or food “to go,” the volume of packaging and the amount of waste is multiplied. Global plastic production has strongly increased, from 100 million metric tons in the year 1999 to 359 million metric tons in 2018. The rise is again substantially driven by China, where plastic production has increased from 9 million metric tons in 1999 to 85 million by 2018 (Figure 3).4 During the same time, plastic production in the industrialized countries has tended to remain comparatively flat, as shown in Figure 3 for Europe.

From this point of view, purchases of green bonds by central banks to protect the environment can also have substantial negative side effects on the environment. The systematic distortion of prices on capital markets leads to malinvestments and excessive consumption of cheap products. It possibly contributes to the reallocation of production to countries with weaker environmental standards and higher CO2 emissions. For this reason, the vision of a “green” monetary policy should be treated with care.

References

Adalet McGowan, Müge, Dan Andrews, and Valentine Millot. “The Walking Dead: Zombie Firms and Productivity Performance in OECD Countries.” OECD Economics Department Working Paper 1372, 2017.

Copeland, Brian, and Scott Taylor. “Trade, Growth, and the Environment.” Journal of Economic Literature 42, no. 1 (2004): 7–71.

Dooley, Michael P., David Folkerts-Landau, and Peter Garber. “The Revived Bretton Woods System.” International Journal of Finance and Economics 9, no. 4 (2004): 307–13.

Geyer, Roland, Jenna Jambeck, and Kara Law. “Production, Use, and Fate of All Plastics Ever Made.” Science Advances 3, no. 1 (2017): 1–5.

Gourmelon, Gaelle. “Global Plastic Production Rises, Recycling Lags.” Vital Signs 22 (2015): 91–95.

Hayek, Friedrich August von. Prices and Production. New York: August M. Kelly Publishers, 2015.

Huang, Lizhen, et al. “Carbon Emission of Global Construction Sector.” Renewable and Sustainable Energy Reviews 81, no. 2 (2018), 1906–16.

Liu, Jian, et al. “Analysis of CO2 Emission in China’s Manufacturing Industry Based on Extended Logarithmic Mean Division Index Composition.” Sustainability 11, no. 1 (2019): 226.

McKinnon, Ronald, and Gunther Schnabl. “China and its Dollar Exchange Rate. A Worldwide Stabilizing Influence?.” World Economy 35, no. 6 (2012): 667–93.

Schnabl, Gunther. “China’s Overinvestment and International Trade Conflict.” China and World Economy 27, no. 4 (2019): 37–62.

- 1. Copeland and Taylor (2004) call the relocation of environmentally unfriendly parts of the production process from industrialized countries to countries with less strict environmental standards the “pollution haven effect.”

- 2. For instance, plastics make up about 50 percent of the volume of a typical US vehicle today (see Gourmelon, 2015).

- 3. About 20 percent of global plastic production is used in construction (see Geyer et al., 2017).

- 4. China is the largest producer of plastics in the world, accounting for about one-quarter of global plastic production.

Tags: Featured,newsletter