The Pool of Real Wealth Last Thursday, the people of Britain voted in a referendum to leave the European Union (EU). Most commentators view Britain’s exit (“Brexit”) from the European Union as bad news for economic growth in the UK and the euro zone. As a result, it is argued, the growth rate in the rest of the world will be also badly affected. It is more likely that, whether the pace of real economic growth over time will weaken or strengthen is going to be set by the pace of expansion in the pool of real wealth. A strengthening in the pace of economic growth implies a strengthening in the rate of growth of the pool of real wealth. Conversely, a weakening in the pace of economic growth implies a weakening in the rate of growth of the pool of real wealth. The ability of an economy to generate a rising rate of growth of the pool of real wealth is determined by the ongoing expansion and the enhancement of the infrastructure. This permits the increase in the rate of growth of the production of goods and services to support people’s life and well-being. The key for this is an ongoing allocation of some portions of real wealth toward the formation of capital goods (i.e., the enhancement and the expansion of the infrastructure).

Topics:

Frank Shostak considers the following as important: Featured, newslettersent, On Economy, On Politics, Switzerland and Brexit

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

The Pool of Real WealthLast Thursday, the people of Britain voted in a referendum to leave the European Union (EU). Most commentators view Britain’s exit (“Brexit”) from the European Union as bad news for economic growth in the UK and the euro zone. As a result, it is argued, the growth rate in the rest of the world will be also badly affected. It is more likely that, whether the pace of real economic growth over time will weaken or strengthen is going to be set by the pace of expansion in the pool of real wealth. A strengthening in the pace of economic growth implies a strengthening in the rate of growth of the pool of real wealth. Conversely, a weakening in the pace of economic growth implies a weakening in the rate of growth of the pool of real wealth. The ability of an economy to generate a rising rate of growth of the pool of real wealth is determined by the ongoing expansion and the enhancement of the infrastructure. This permits the increase in the rate of growth of the production of goods and services to support people’s life and well-being. The key for this is an ongoing allocation of some portions of real wealth toward the formation of capital goods (i.e., the enhancement and the expansion of the infrastructure). NB: The allocation of real wealth here means that a portion of real wealth is channeled toward the activities that are engaged in the expansion and the enhancement of the infrastructure. Now, if real wealth were to be directed toward the production of final goods and services only — while an inadequate amount is allocated toward the expansion and the enhancement of the infrastructure — this will amount to a consumption of capital. Over time this is going to undermine the economy’s ability to pursue rising economic growth. In fact a prolonged neglect to allocate a sufficient amount of wealth toward the enhancement and the expansion of the infrastructure is likely to result in a stagnant or even in a declining pool of real wealth over time. This means stagnant or declining real economic growth — a fall in people’s living standard. |

Where is the UK economy going next? London bookies await your bets! Cartoon via theguardian.com |

How Will Brexit Affect the Wealth Generation Process?If the process of wealth generation is currently in good shape then Britain’s exit from the EU shouldn’t have any negative effect on real economic growth. This, however, might not be the case. It is likely that the reckless monetary policy of central banks in the UK and the eurozone has inflicted a severe damage to the process of real wealth formation. Loose monetary policies (i.e., monetary pumping and the artificial lowering of interest rates) sets in motion the diversion of real wealth from wealth generators toward non-wealth generating activities. This in turn over time weakens wealth generators ability to expand the pool of real wealth. Since the 2008 financial crisis, following the lead of the US central bank, the central banks in the UK and the eurozone have aggressively lowered interest rates and pushed monetary liquidity to the banking system. In the UK, the central bank policy rate was lowered from 5% in January 2008 to 0.5% currently. In the eurozone the policy rate was lowered from 4.25% in July 2008 to 0% at present. |

Administered interest rates (main refinancing rates) of the BoE and the ECB – click to enlarge. |

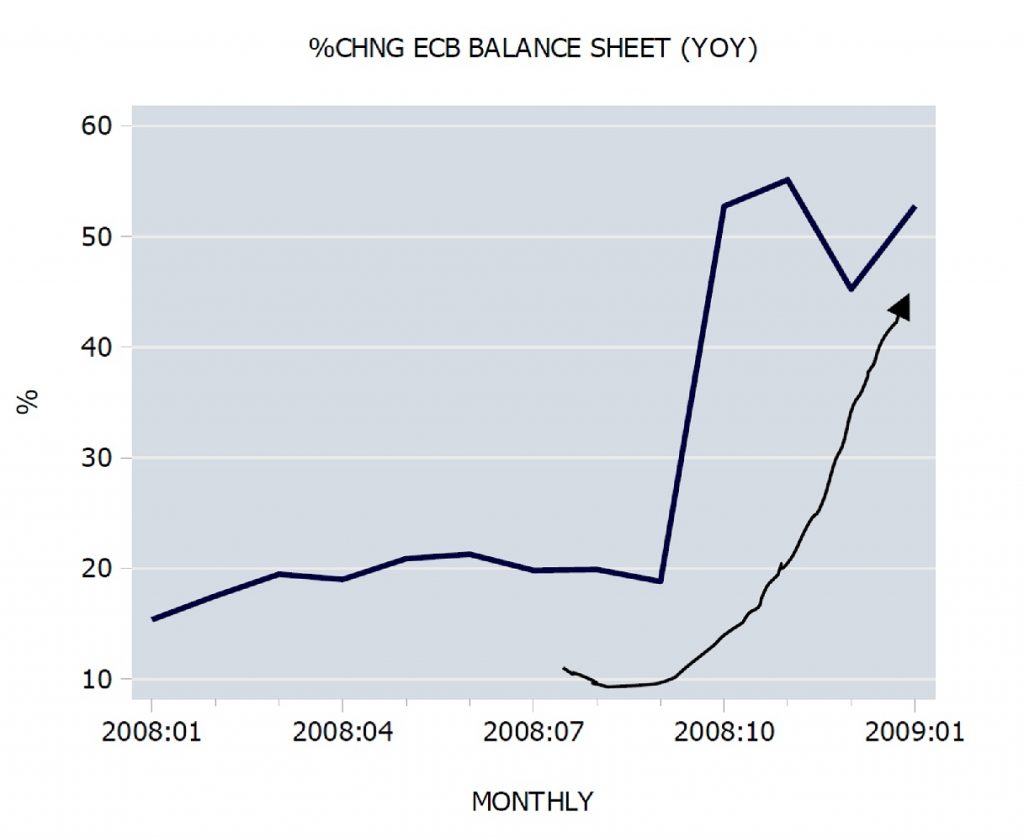

Yearly growth rate of the Bank of England balance sheetThe yearly growth rate of the Bank of England balance sheet jumped from 22.2% in January 2008 to 163.8% by October of that year. The yearly growth rate of the European Central Bank balance sheet jumped from 15.3% in January 2008 to 55.1% by November of that year. |

Growth of the BoE’s balance sheet in 2008 – click to enlarge. |

Yearly growth rate of the ECB balance sheet 2008/2009Unfortunately it is not possible to establish the magnitude of the damage that these loose monetary policies have inflicted on the process of real wealth formation. (It is not possible to calculate the size of the pool of real wealth since we cannot establish the total of various heterogeneous goods and services.) We suggest that in the event of a plunge in real economic growth, this is going to happen not on account of the Brexit but in response to the severe damage that previous reckless monetary policies have inflicted to the process of real wealth formation. In response to the Brexit, it is also highly likely that both the UK and the euro zone central banks will be ready to push more money in order to “keep” real economic growth going, thereby inflicting further damage to the wealth generating process. Also, the current highly regulated EU centralized economic framework is restrictive toward opening up markets, promoting free trade and ultimately economic growth. In this respect BREXIT, which is an act of decentralization will provide more scope for competitive markets and hence should be an agent for economic growth. |

Growth of the ECB’s balance sheet in 2008/9 – click to enlarge. |

Real GDP and Economic GrowthThe popular way of thinking assesses economic growth in terms of so called real GDP. I have noted elsewhere that the whole concept of GDP is a hollow one. Changes in the so-called real GDP are in fact depicting changes in money supply. Consequently, fluctuations in the growth rate of money supply are manifested in the fluctuations of the real GDP. Based on the lagged growth rate of money supply it is likely that the yearly growth rate of UK real GDP is forecast to close at 3.5% by Q4 from 2% in Q1. By Q4 next year the yearly growth rate is forecast to climb to 4%. For the eurozone, I forecast the yearly growth rate of 3.6% by Q4 versus 2% in Q1. For the Q4 next year the growth rate is forecast to settle at 4.3%. |

Percentage change y/y in UK real GDP growth, plus model forecast – click to enlarge |

ConclusionWe can thus conclude that based on the lagged money supply growth rate it is quite likely that we could have a strengthening in the growth momentum of real GDP in both the UK and the euro zone. In terms of true real economic growth the likely acceleration in the monetary pumping by central banks is going to undermine further the process of real wealth formation. As long as the pool of real wealth is still holding, central bank policymakers could get away with the myth that they can grow the economy. Once the pool starts to stagnate or to decline, the myth that central banks can grow an economy is shattered. One could only hope that notwithstanding central banks damaging policies wealth generators could keep the pool of wealth growing. Charts by AASE (Applied Austrian School Economics) Chart and image captions by PT This article appeared originally at the Mises Institute |

Percentage change y/y in EMU real GDP growth, plus model forecast – click to enlarge. |