MicroStrategy (MSTR) stock is soaring alongside Bitcoin. In the wake of extreme confidence, we fear many MicroStrategy investors fail to grasp the inherent risks with its unique convertible bond funding and leverage scheme. A recent podcast featuring Tom Lee presented some positive facts about MicroStrategy's recent convertible bond offering but failed to tell the whole story. Left out of Tom Lee's enthusiastic outlook is that the "novel strategy" can also bankrupt the company. While Bitcoin may continue higher, proving MicroStrategy's CEO Michael Saylor a genius, investors should at least appreciate what may happen if things do not go according to plan. We now present the other side of the story. What is MicroStrategy? Per its website, MicroStrategy

Topics:

Michael Lebowitz considers the following as important: 9) Personal Investment, 9a.) Real Investment Advice, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

MicroStrategy (MSTR) stock is soaring alongside Bitcoin. In the wake of extreme confidence, we fear many MicroStrategy investors fail to grasp the inherent risks with its unique convertible bond funding and leverage scheme. A recent podcast featuring Tom Lee presented some positive facts about MicroStrategy's recent convertible bond offering but failed to tell the whole story. Left out of Tom Lee's enthusiastic outlook is that the "novel strategy" can also bankrupt the company.

While Bitcoin may continue higher, proving MicroStrategy's CEO Michael Saylor a genius, investors should at least appreciate what may happen if things do not go according to plan. We now present the other side of the story.

What is MicroStrategy?

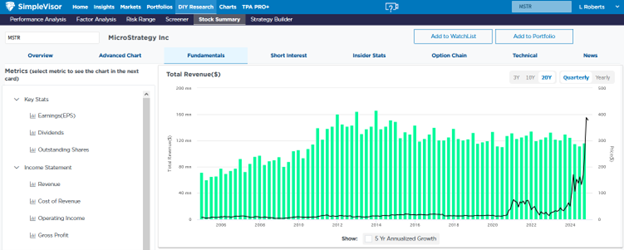

Per its website, MicroStrategy "provides software solutions and expert services that empower every individual with actionable advice." Since 2000, the company has had a cumulative $1.4 billion net loss. Furthermore, its revenue has deteriorated over the last ten years, as shown below, courtesy of SimpleVisor.

As a software solutions company, it is a bust. However, its CEO, Michael Saylor, has avoided bankruptcy, at least for now.

Saylor transformed a flailing technology business into a leveraged Bitcoin holding company.

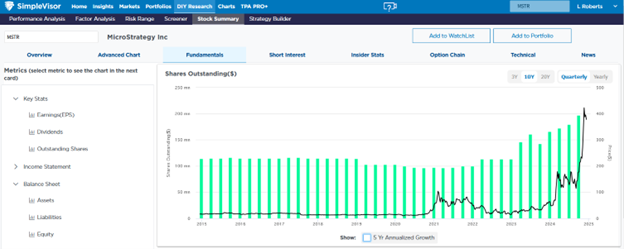

Over the last five years, MicroStrategy has borrowed $7.27 billion via convertible debt securities and doubled its share count to purchase Bitcoin. We highlight the tremendous growth in its outstanding shares and the value of its Bitcoin holdings below.

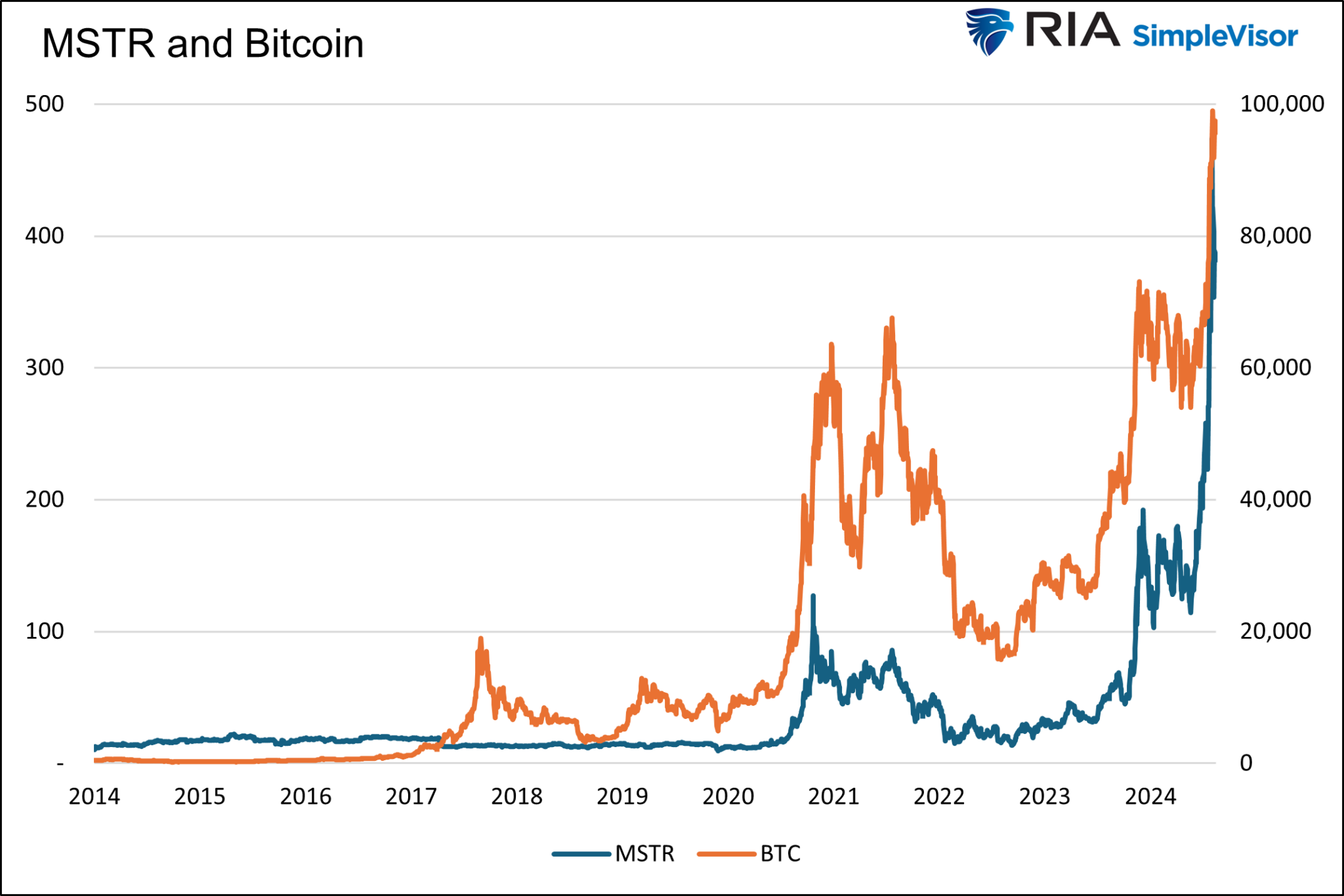

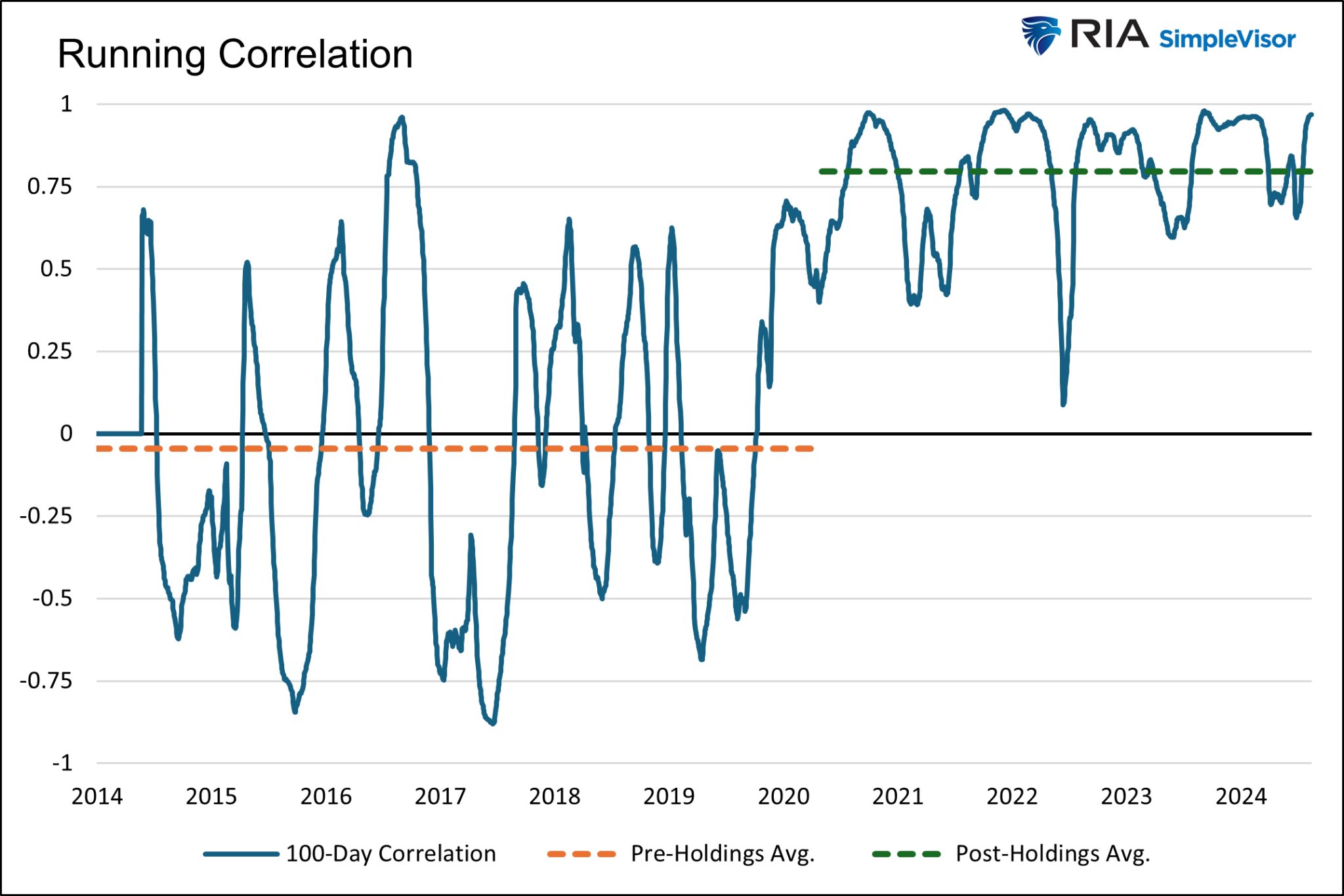

The following graphs show that once they started buying Bitcoin in 2020, its price became closely correlated with Bitcoin. The company is essentially a leveraged Bitcoin holding company, so the relationship may strengthen further as it buys more Bitcoin.

Valuing MicroStrategy

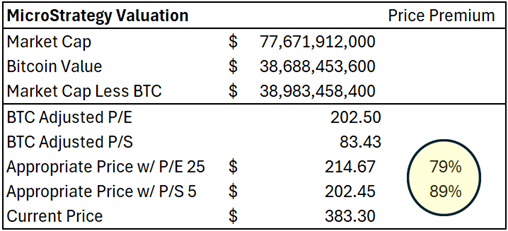

On December 6, 2024, SimpleVisor shared a valuation analysis of MicroStrategy. The bottom line was that even with some friendly valuation assumptions for its core technology operations, investors are paying an exorbitant premium for its bitcoin holdings. Per the article:

We previously mentioned that MSTR has become a vehicle for making a leveraged bet on the value of BTC. Below, we dissect the company's valuation to evaluate the premium investors are paying for the underlying company. The company's market capitalization, less the market value of its BTC holdings, gives us an idea of the value placed on the underlying company. Combining that metric with the TTM recurring EPS, we see the underlying business trades at an astronomical P/E of 202.5. Similarly, P/S is "headed to the moon" at 83.4.

Next, we make a naive assumption that the appropriate P/E and P/S ratios for the underlying business are 25 and 5, respectively. These are very generous assumptions, given that the underlying business has exhibited very little revenue and EPS growth over the long run. Under these conditions, we calculate the fair value price of MSTR, including its BTC position, to be somewhere between $202.45 and $214.67. Thus, even with generous growth assumptions, investors are paying an 80%-90% premium over fair value to hold shares of MSTR. With both leveraged and unlevered Bitcoin ETFs now available on stock exchanges, it's mind-boggling that investors would pay such a premium for MSTR.

Tom Lee's Commentary

Wall Street veteran Tom Lee, a frequent contributor to CNBC and other large financial media outlets, is well known for being an optimist, or as some say, a perma-bull. He recently gave his bullish thoughts on MicroStrategy (LINK). The following is transcribed from a video, so please ignore his grammar and speech patterns.

MicroStrategy, uh around five years ago, transformed the company by using its balance sheet. They had a lot of cash on hand to buy Bitcoin and so instead of the stock being valued on its actual software business which had been languishing, it's valued as a holder of Bitcoin. But as Bitcoin has risen and MicroStrategy stock has gone up it's created an opportunity for them to issue convertible bonds and debt to acquire more Bitcoin.

Now you might think that this is uh a little bit reckless, but it turns out it's a very novel strategy because they have created a lot of network value. They're one of the largest holders of Bitcoin now and ultimately, they may become the second largest holder of Bitcoin after the US government and they're doing this with the ability to borrow at a very low cost. You might wonder why bond holders are buying these bonds they're offering. For the first time the ability for someone to put a billion dollars work in the bond world to own a bond that has exposure to bitcoin.

Convertible Debt Funding

As we share below, MicroStrategy has borrowed $7.27 billion solely using convertible bonds. The proceeds were used to purchase Bitcoin.

Convertible bonds are unique because they offer investors the benefits of a bond with the bonus of equity exposure. Assuming the convertible bond issuer doesn't default, bondholders get paid back their initial investment at maturity, earn interest, and own a call option, allowing them to buy shares in the company at a specific conversion rate.

Let's examine MicroStrategy's recent convertible debt issuance to help you better appreciate the bet its buyers are making.

On November 21, 2024, MicroStrategy issued $3 billion of 0% convertible notes maturing on December 1, 2029. Click HERE for the press release with details.

Its stock was trading at $430 at issuance, and the conversion price was $672. Investors were willing to accept call options instead of interest payments. The equity options have value if MicroStrategy shares rise by more than 50% over the next five years. If the stock does not get above $672, investors will earn a 0% return on their investment.

There is also the opportunity cost to consider. MicroStrategy's S&P credit rating is junk (B-). The yield on similar bonds, per the ICE BOA index, is 6.75%. The return on a five-year compounding investment at 6.75% provides a total return of 47%.

Thus, investors are forgoing a five-year total return of 47%, hoping that MicroStrategy shares will double in five years to break even versus holding similar-rated junk bonds.

Investors Are Paying Dearly For Call Options

Option prices derive from the current stock price, the strike price, time until expiration, implied volatility, interest rates, and dividends. All those factors are known except implied volatility. Formulas such as Black-Scholes solve for implied volatility to equate the option price with the other factors.

Implied volatility measures how much investors think the underlying stock will move in the future.

Convertible debt is priced off the company's credit risk, the bond's interest rate, and the call option's value. The more the call value is worth, the more proceeds the issuing company can garner. In this case, incredibly high implied volatility on MicroStrategy shares pushes the option value higher, allowing the company to raise more funds.

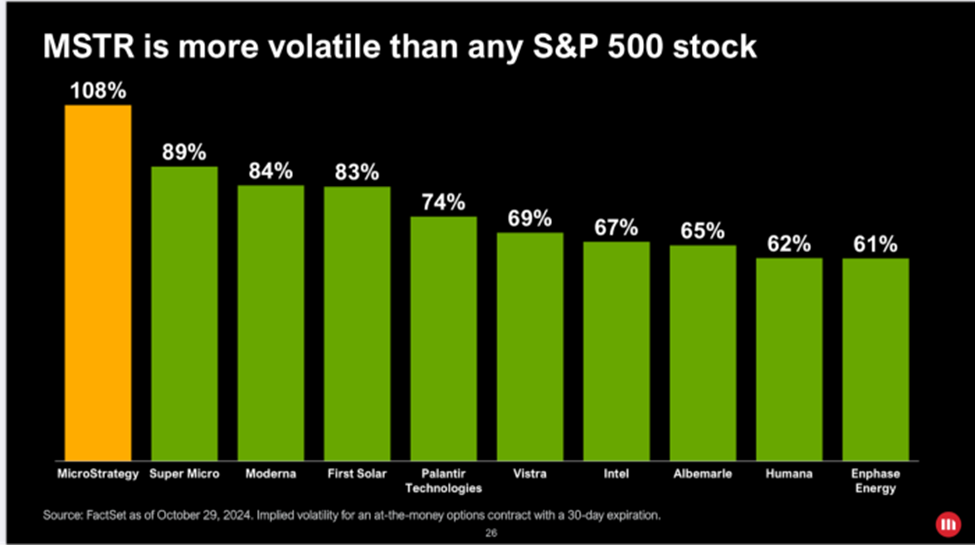

We cannot get prices on five-year MicroStrategy call options, but we can provide some context for the high implied volatility with one-year option prices. Currently, the implied volatility on one-year options with a strike price equal to its current price is 102.30%. That means investors expect the shares to change by 6.5% (102.30% / Sq. Root of 252) daily.

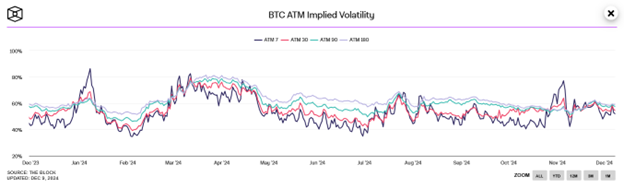

The first graph below, courtesy of the Financial Times, shows that MSTR is more volatile than any other S&P 500 stock. Moreover, the second graph, courtesy of The Block, shows that MSTR has about twice the implied volatility of Bitcoin.

Saylor Is Pumping Volatility

MicroStrategy and its CEO, Michael Saylor, are touting Bitcoin to push the implied volatility of its shares higher, thus allowing it to issue debt as cheaply as possible. Here is a recent example:

The co-founder and chairman of MicroStrategy told CNBC on Friday that Bitcoin should deliver an annualized rate of return of 29% over the next 21 years. -Yahoo Finance

The Financial Times, in its article entitled MicroStrategy's Secret Sauce Is Volatility, Not Bitcoin, sums the strategy up as follows:

This sheds light on one of the paradoxes around the MicroStrategy story: why does co-founder Michael Saylor relentlessly hype bitcoin while his company is buying it? Most people would talk down an asset they're accumulating.

But for MicroStrategy, volatility is the real currency. Saylor's bombastic interviews, grandiose predictions, and relentless social media posting aren't just noise — they're the fuel for the financial fire. There's never a dull moment with the guy. The crazier the stock, the better the terms for the next convertible.

Cheaper Approaches To Owning Bitcoin

Tom Lee is correct in that investors limited solely to fixed-income investments, now have a way to gain exposure to Bitcoin. However, there are much better options for anyone else wanting to own Bitcoin. As we noted earlier, MicroStrategy's stock valuation is at least double that of the Bitcoin it holds. And, as a reminder, its software business has almost no value. One could even argue it has a negative value. Accordingly, investors who want to buy Bitcoin should just buy Bitcoin or the numerous Bitcoin ETFs available.

Furthermore, investors can buy call options on Bitcoin or Bitcoin ETFs, which essentially is what the convertible debt is. As we were writing this article, the implied volatility of IBIT (iShares Bitcoin ETF) was 69%. While high, it is much cheaper than the MicroStrategy options embedded in their convertible debt, at over 100%.

As Tom Lee claims, issuing convertible debt to buy Bitcoin may be "novel," but as market pricing informs us, it's a scheme to take advantage of unwary investors.

What Can Go Wrong?

The potential reward for convertible bondholders is that the price of MicroStrategy shares is higher than the conversion price.

The risks of owning the debt are twofold.

First, assuming the company doesn't default, bond investors will get their money back if the share price trades below the conversion price. But, they will have earned nothing for five years.

The worst-case scenario occurs when one considers how MicroStrategy can pay back the $7.2 billion of convertible debt as it matures. Unlike most companies, the answer is not with the income it earns. The graph below shows their cumulative net income after taxes since 2000 is negative $1.5 billion. Its average quarterly loss over the last eight quarters is $316 million. The last time they made a quarterly profit was in 2021. Even at MicroStrategy's peak earnings ability, its cumulative net income was only about $650 million.

The company could issue more stock to pay its bondholders back. Such would dilute current shareholders and likely reduce the stock price and the value of the convertibility option.

MicroStrategy could instead issue more debt to pay back old debt. However, if the price of Bitcoin is down, bondholders may not accept convertible debt and instead demand a back-breaking interest rate.

Lastly, they can sell Bitcoin to pay back its bondholders. Such a plan may work out if Bitcoin trades at a high price. However, it could be very problematic if the price is much lower. Surely, if one of the world's top three holders of Bitcoin were to sell significant amounts, it could significantly damage the price of Bitcoin.

Paying back the debt is a potentially slippery slope for MicroStrategy and, ultimately, its investors.

Summary

We think MicroStrategy is preying on investors. They are pumping up optimism on Bitcoin to drive higher volatility in their stock. Doing so allows them to raise funds and add to their Bitcoin holdings. Its convertible funding strategy is legal, but the risks to its shareholders and bondholders are much more significant than many of its investors appreciate.

The problem with such a leveraged scheme is that the company is putting all its eggs into Bitcoin. A sharp decline in Bitcoin will likely accompany the collapse of MicroStrategy! The other risk, although less likely under the Trump presidency than Biden, is if the SEC decides to investigate MicroStrategy over their "unique" strategy.

We leave you with a word from Doug Kass:

As MicroStrategy's shares fall, the company continues to sell $1 bills for $3.

The post MicroStrategy And Its Convertible Debt Scheme appeared first on RIA.

Tags: Featured,newsletter