No government looking to massively expand its size in the economy and monetize a soaring deficit is going to act against rising prices, despite claiming the opposite. One of the things that surprises citizens in Argentina or Turkey is that their populist governments always talk about the middle classes and helping the poor, yet inflation still soars, making everyone poorer. Inflation is the gradual erosion of the purchasing power of the currency. Governments will always use different excuses to justify inflation: soaring demand, “supply chain disruptions,” or evil corporations’ greed. However, most of the times these are excuses. Inflation is always a monetary phenomenon. Prices soar because money supply rises massively above real output and real money demand.

Topics:

Daniel Lacalle considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| No government looking to massively expand its size in the economy and monetize a soaring deficit is going to act against rising prices, despite claiming the opposite.

One of the things that surprises citizens in Argentina or Turkey is that their populist governments always talk about the middle classes and helping the poor, yet inflation still soars, making everyone poorer. Inflation is the gradual erosion of the purchasing power of the currency. Governments will always use different excuses to justify inflation: soaring demand, “supply chain disruptions,” or evil corporations’ greed. However, most of the times these are excuses. Inflation is always a monetary phenomenon. Prices soar because money supply rises massively above real output and real money demand. |

How can there be “shipping bottlenecks” driving a 100 percent rise in freights when the shipping industry was burdened by massive overcapacity in 2019? How can anyone say that natural gas and oil have soared due to supply chain disruptions when supply has perfectly followed demand? The reality is that some of those factors may explain a small proportion of the price rise, but the Global Food Index and Bloomberg Commodity Index are not at multiyear highs due to these problems.

What happened in 2020 was that massive money creation in the middle of an economic lockdown created monetary inflation in nonreplicable and relatively scarce goods and services. Why did this not happen before?

Well, it did. Before, we saw a massive rise in asset prices. Inflation is created where the excess of money goes, be it soaring equity, and high yields in bond markets or all-time high housing and private equity valuations. More money chasing the same number of goods. Furthermore, there was also massive inflation in essential goods and services. The prices of housing, healthcare, and education rose significantly above the official Consumer Price Index (CPI) print.

Why has it burst so aggressively now? First, massive money printing in the middle of a lockdown kept asset valuations elevated but also started to generate fund flows to scarce—so-called value—sectors. And what are “value sectors”? Those that suffered overcapacity and weakening demand growth in the past decade. So, more money flowed to oil, natural gas, even coal or aluminum, where the industry was plagued by excess capacity in the decade of cheap money.

Inflation does not happen the next day you print money. It is a slow process of gradual erosion of the purchasing power of the currency that started years ago and culminated with the insane decision to implement monster demand-side policies (huge government spending and money printing) in the middle of a lockdown.

But why do governments ignore it? Why do they not act? Surely it is in their best interest to keep prices low and consumers—voters—happy. The answer is simple: because governments are the biggest beneficiaries of inflation. They collect more receipts from indirect taxes and their soaring debt is slowly eroded by inflation.

Furthermore, governments never act against inflation, because they benefit from it and, more importantly, can blame it on everyone except their policies. Even in Argentina, where inflation is higher than 50 percent and ten times higher than in neighboring countries, citizens are slowly convinced that there must be other causes than money printing. Even when presented with the evidence of a central bank that has raised money supply more than 120 percent in two years with diminishing demand, the press and politicians blame inflation on “multicause” effects. A joke.

Take the recent comments about soaring prices in the United States from the US administration.

White House chief of staff Ron Klain said that inflation was a “high-class problem” and, when confronted, Jen Psaki, press secretary, replied that people buying more things than ever before were the cause of inflation. However, in the latest figure, real consumer spending is down to 1 percent annualized in the United States, according to Capital Economics.

National Economic Council director Brian Deese said that if you deducted the rise of beef, pork, and poultry, price increases were normal. “If you take out those three categories, we’ve actually seen price increases that are more in line with historical norms.” So, if you deduct the price increase of the things you eat every day and eliminate the price of the things you buy, there is no inflation, right?

All are using the usual excuses. Blame businesses for higher prices (evil pork and chicken farmers, evil shippers and port managers), blame consumers (you buy too much too fast), and smile, saying they really care and are working on it … Printing and spending more.

The rhetoric about “transitory” inflation remains, both in governments, who are unwilling to reduce massive spending, and in central banks, who are caught between a rock and a hard place, as they have to monetize soaring deficits from highly indebted governments and at the same time defend their strategy of “price stability.” Between those two, guess what they have decided to opt for? Yes, keep printing and say some day it will pass.

The problem of the “transitory inflation” argument is that it is a fallacy when you look at accumulated inflation. If the Consumer Price Index rise is 5 percent in 2021 and, say, 3 percent in 2022, they will say that inflation is down, but you and I will have seen our real wages and savings eroded by more than 8.1 percent. Even worse, if inflation rises above 6 percent in 2021 and comes in below 2 percent in 2022, you and I will have lost also more than 8.1 percent in purchasing power, but central banks will say they have to print more to “combat deflation risks.”

Interventionist governments are unwilling to cut spending or reduce deficits substantially, so they will use the inflationary tax knowing that they can use the usual excuses: 1) say there is no inflation if you eliminate the prices that rise, 2) say it is transitory, 3) blame businesses, 4) blame consumers, 5) present themselves as the solution with “price controls.”

Inflation is taxation without legislation, as Milton Friedman said. There is no such thing as “multicause” inflation. It is a lot more money going to the same number of goods. And the inflation tax is increasing the size of government in the economy both ways: through massive deficit spending and eroding the purchasing power and savings of the private sector through currency debasement.

You Might Also Like

Can Economic Data Explain the Timing and Causes of Recessions?

Can Economic Data Explain the Timing and Causes of Recessions?

2021-09-20

Most economists are of the view that through the inspection of economic data it is possible to identify early warning signs regarding boom bust cycles. What is the rationale behind this way of thinking?

War Has Declined in the West Because War Isn’t “Worth It” for Rich Countries

War Has Declined in the West Because War Isn’t “Worth It” for Rich Countries

2021-09-17

The triumph of peace in contemporary societies is expressed as an obvious fact by mainstream intellectuals. Noting the relatively peaceful state of the world is part of a broader narrative to paint a positive picture of humanity. Yet there is a kernel truth to the assertion that quality of life indicators are improving, as explored by Marian Tupy and other optimists. But the game of warfare is more complicated.

Depriving People of Purchasing Power Is A Moral Transgression | Andrew Moran

Depriving People of Purchasing Power Is A Moral Transgression | Andrew Moran

2021-08-30

Purchasing Power Matters! Andrew shares what and why it matters to him. Governments and Central Banks are depriving the people from the fruits of their labor and ability to save for the future.

Share your thoughts in the comment section below. Tell your story and let the world hear why Purchasing Power Matters to you.

Connect with Andrew on Twitter & YouTube here:

https://twitter.com/andrewliberty23

https://andrewmoran.net/

Visit the PPM website for details on how to share your story and to read informative articles.

https://www.purchasingpowermatters.co

Follow the Purchasing Power Matters social media links here:

Twitter – https://www.twitter.com/ppowermatters

Instagram – https://www.instagram.com/purchasingpowermatters

Facebook – https://www.facebook.com/purchasingpowermatters

WaPo Editors: “Liberty” Requires Us to Implement Vaccine Passports

WaPo Editors: “Liberty” Requires Us to Implement Vaccine Passports

2021-08-20

Mandating private and government employees to be immunized against covid-19 and requiring the use of standardized electronic passes as proof of immunization across the nation is what liberty is made of, the editors of the Washington Post argued last week.

The Old Right on War and Peace

The Old Right on War and Peace

2021-08-10

As the force of the New Deal reached its heights, both foreign and domestic, during World War II, a beleaguered and tiny libertarian opposition began to emerge and to formulate its total critique of prevailing trends in America.

Andrew Moran Evadé d’un tribunal anglais, arrêté en Espagne.

Andrew Moran Evadé d’un tribunal anglais, arrêté en Espagne.

2021-06-26

#Replay #Reportage #ReplayTv #belgium

#Police_Belge #Belgique #policebelges #France

#gendarmesfrançais #Gendarmes_français #Police

#100_jours avec #la_police #reportage,#reportage2021,#reportage_choc,#reportagem,#reportage_francais,

#reportage_complet,#reportage_comique,#reportage_documentaire,#documentaire,

#documentaire_français, #documentaire_politique, #reportage#complet_en_francais,

#reportage_complet_fr 2021 #nouveauté,#enquete_exclusive 2016, #francais,

#reportage_police,#drogue,#violence,#armée,#guerre,#enquete d’actualité,#cannabis, #magazine,#enquetes,#Enquete_EXclusive #Gendarmes,#Gendarmes2021,#cambrioleurs #reportages2021.

film telefilm complet en francais,

film telefilm thriller,

film telefilm complet en francais 2019,

film

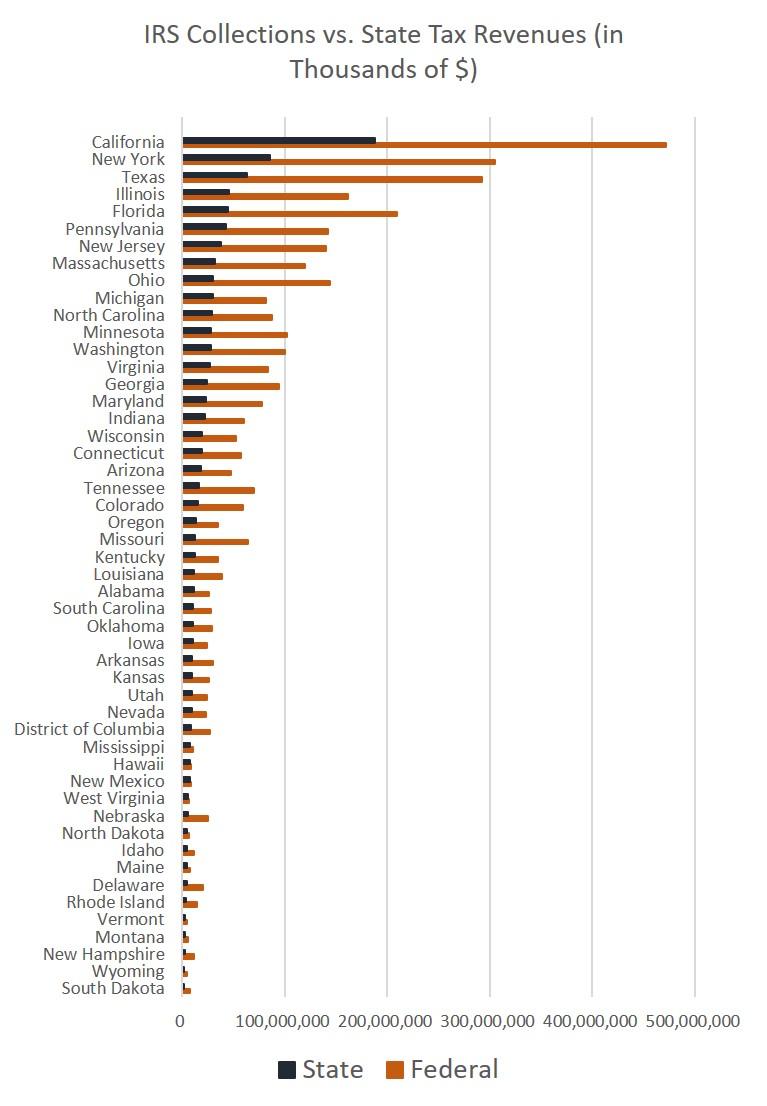

The Feds Collect Most of the Taxes in America—So They Have Most of the Power

The Feds Collect Most of the Taxes in America—So They Have Most of the Power

2021-06-26

In 2021, it’s clear Americans now have thrown off any notions of subsidiarity and instead embraced the idea that the federal government should be called upon to fund pretty much anything and everything. From "stimulus checks" to "paycheck protection," it’s assumed an entire national workforce can be propped up by federal spending.

How Monetary Expansion Creates Income and Wealth Inequality

How Monetary Expansion Creates Income and Wealth Inequality

2021-05-19

“Every change in the money relation alters … the conditions of the individual members of society. Some become richer, some poorer.” – Mises, Human Action, p. 414. New money enters the economy at a particular point. It does not enter in the form of a proportional and simultaneous increase in everybody’s incomes.

Tags: Featured,newsletter