In October, money supply growth fell slightly from September’s all-time high, although growth still remains at levels that would have been considered outlandish just eight months ago. October’s easing in money-supply growth comes after eight months of record-breaking growth in the US which came in the wake of unprecedented quantitative easing, central bank asset purchases, and various stimulus packages. Historically, the growth rate has never been higher than what we’ve seen this year, with the 1970s being the only period that comes close. It was expected that money supply growth would surge in recent months. This usually happens in the wake of the early months of a recession or financial crisis. But it appears that now the United States is several months into an

Topics:

Ryan McMaken considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

In October, money supply growth fell slightly from September’s all-time high, although growth still remains at levels that would have been considered outlandish just eight months ago. October’s easing in money-supply growth comes after eight months of record-breaking growth in the US which came in the wake of unprecedented quantitative easing, central bank asset purchases, and various stimulus packages.

Historically, the growth rate has never been higher than what we’ve seen this year, with the 1970s being the only period that comes close. It was expected that money supply growth would surge in recent months. This usually happens in the wake of the early months of a recession or financial crisis. But it appears that now the United States is several months into an extended economic crisis, with around 1 million new jobless claims each week from March until mid-September. More than 6 million unemployed workers are currently collecting standard unemployment benefits, with eight million more collecting “Pandemic Emergency Unemployment Compensation.” Economic growth plummeted in the second quarter as GDP growth fell more than 9 percent.

The central bank continues to engage in a wide variety of unprecedented efforts to “stimulate” the economy and provide income to unemployed workers and to provide liquidity to financial institutions. Moreover, as government revenues have fallen considerably, Congress has turned to unprecedented amounts of borrowing. But in order to keep interest rates low, the Fed has been buying up trillions of dollars in assets—including government debt. This has fueled new money creation.

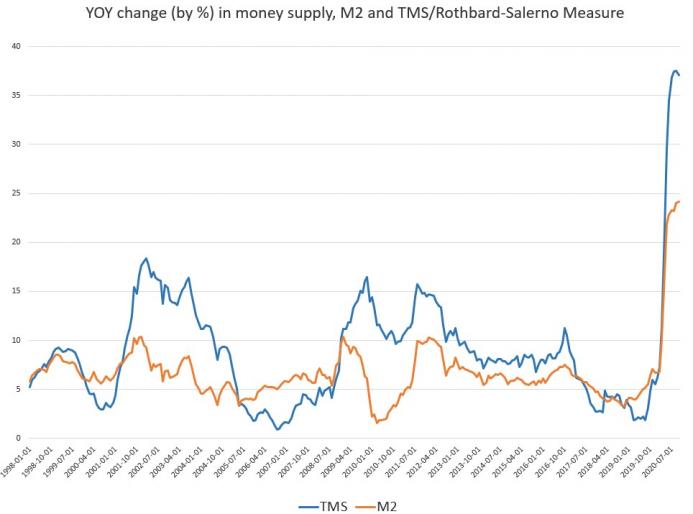

| During October 2020, year-over-year (YOY) growth in the money supply was at 37.08 percent. That’s down slightly from September’s rate of 37.54 percent, and up from October 2019’s rate of 4.8 percent. Historically this is a very large surge in growth, year over year. It is also quite a reversal from the trend that only just ended in August of last year, when growth rates were nearly bottoming out around 2 percent. In August 2019, the growth rate hit a 120-month low, falling to the lowest growth rates we’d seen since 2007.

The money supply metric used here—the “true” or Rothbard-Salerno money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. The Mises Institute now offers regular updates on this metric and its growth. This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits, traveler’s checks, and retail money funds). The M2 growth rate reached new historic highs in October, growing 24.17 percent compared to September’s growth rate of 24.04 percent. M2 grew 6.4 percent during October of last year. The M2 growth rate had fallen considerably from late 2016 to late 2018 but has been growing again in recent months. As of March, it is following a trend similar to that of TMS, but to a lesser degree. Money supply growth can often be a helpful measure of economic activity. During periods of economic boom, money supply tends to grow quickly as banks make more loans. Recessions, on the other hand, tend to be preceded by periods of slowdown in rates of money supply growth. However, money supply growth tends to grow out of its low-growth trough well before the onset of recession. As recession nears, the TMS growth rate climbs and becomes larger than the M2 growth rate. This occurred in the early months of the 2002 and the 2009 crises. February 2020 was the first month since late 2008 that the TMS growth rate climbed higher than the M2 growth rate. The TMS growth rate has exceeded M2 in most of this year. As the year progresses, it does appear that the decline in money supply growth has again preceded a recession, and a severe one at that. Both the second and third quarters showed negative growth in real GDP this year. The second quarter this year fell 9 percent, year over year, and the third quarter was down 2.9 percent, year over year. |

M2 and TMS/Rothbard-Salerno Measure, 1998-2019 - Click to enlarge |

| Although some observers will likely claim that the current economic crisis is a result solely of the covid-19 panic and resulting government-forced shutdowns, several indicators do suggest that the economy was primed for a recession. The preceding decline in TMS is one of these indicators, as is the late 2019 liquidity crisis in the repo markets. The Fed’s moves to drop interest rates and to once again grow its balance sheet speak to the weakness of the economy leading up to April 2020.

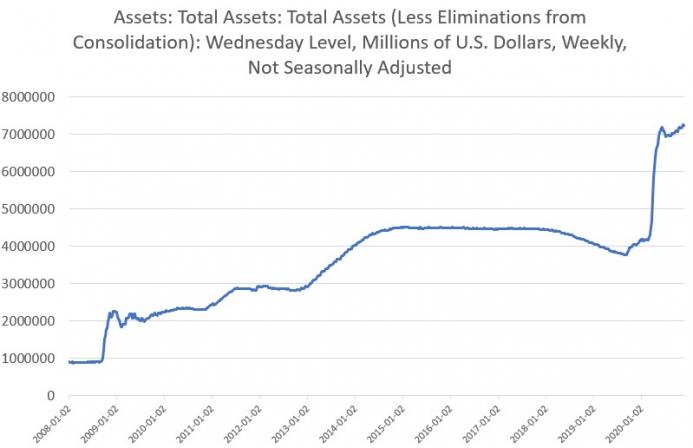

After initial balance sheet growth in late 2019, total Fed assets surged to nearly $7.2 trillion in June and have rarely dipped below the $7 trillion mark since then. As of late October, total assets are again pushing above $7.2 trillion. These new asset purchases have set a new all-time high and are propelling the Fed balance sheet far beyond anything seen during the Great Recession’s stimulus packages. The Fed’s assets are now up more than 600 percent from the period immediately preceding the 2008 financial crisis. While Fed asset purchases are not solely responsible for the surge in new money creation, they are certainly a sizable factor. Bank loan activity has surged as well, also driving new money creation. |

Assets: Total Assets, n.s.a. 2008-2020 - Click to enlarge |

| Below is the dollar volume for M2 and TMS:

In terms of total dollar amounts now extant, the overall M2 total money supply in October was $18.7 trillion and the TMS total was $19.0 trillion. Since January, this is an increase of $3.3 trillion in M2 and $4.8 trillion in the TMS. Moreover, for the past two months, the TMS total has done something new: it has grown to become larger than the M2 total. This is largely being fueled by the immense growth in US Treasury deposits at the Fed, which are factored into TMS, but not M2. Treasury deposits ballooned from $375 billion in March to an unprecedented $1.7 trillion in July. In October, Treasury deposits fell slightly to $1.5 trillion, but remained near record-breaking levels. |

M2 and TMS in billions of $ - Click to enlarge |

You Might Also Like

The COVID Crisis Supercharged the War on Cash

The COVID Crisis Supercharged the War on Cash

2020-07-01

The corona crisis has already taken a very high toll and caused deep damage in our societies and our economies, the extent of which is yet to become apparent. We have seen its impact on productivity, on unemployment, on social cohesion and on political division. However, there is another very worrying trend that has been accelerated under the veil of fear and confusion that the pandemic has spread.

The Social Consequences of Zero Interest Rates

The Social Consequences of Zero Interest Rates

2020-07-06

Anyone who has ever been to Japan knows: Japan is special. The country has many strange habits. The Japanese culture is simply different and many peculiarities are hardly understood in the West. But it’s not only the old established traditions that are foreign to us Westerners.

The Death Wish of the Anarcho-Communists

The Death Wish of the Anarcho-Communists

2020-07-18

[This article first appeared in the Libertarian Forum, January 1, 1970.]

Now that the New Left has abandoned its earlier loose, flexible non-ideological stance, two ideologies have been adopted as guiding theoretical positions by New Leftists: Marxism-Stalinism, and anarcho-communism.

Marxism-Stalinism has unfortunately conquered SDS, but anarcho-communism has attracted many leftists who are looking for a way out of the bureaucratic and statist tyranny that has marked the Stalinist road.

And many libertarians, who are looking for forms of action and for allies in such actions, have become attracted by an anarchist creed which seemingly exalts the voluntary way and calls for the abolition of the coercive State.

It is fatal, however, to abandon and lose sight of one’s own principles in the

America’s Riots Are Just the Latest Version of Marxist “Syndicalism”

America’s Riots Are Just the Latest Version of Marxist “Syndicalism”

2020-08-31

The year 2020 is one of the most disrupted times in at least the last half century, maybe longer. Global protests and riots, the covid-19 virus, lockdowns, and police killings of unarmed citizens. Add to that widespread rioting, looting, arson, homelessness, and destruction of property, including the tearing down of statues.

Hayek’s Plan for Private Money

Hayek’s Plan for Private Money

2020-09-14

The most famous Austrian economist is 1974 Nobel laureate Friedrich Hayek. Because of his moderate views excusing state interventions in various circumstances, hardcore Rothbardians tend to regard Hayek as less than pure in many areas.

Monetary Policy Flapping in the Wind

Monetary Policy Flapping in the Wind

2020-09-19

Stephanie Kelton’s new book has attracted much attention, and Bob Murphy and Jeff Deist have already reviewed it, with devastating results. Why another review? The policies proposed in the book are so pernicious that further exposure of what she has in store for us is needed, and I have some new points to offer for your consideration.

Mises and Moral Relativism

Mises and Moral Relativism

2020-09-29

I heard several days ago from my friend Larry Beane that people in Walter Block’s seminar who had been reading Theory and History wondered whether Mises is a moral relativist. As I’ll try to show, the answer depends on what you mean by “moral relativist,” but in the way the term is usually understood in contemporary philosophy, he isn’t.

Why “Taxing the Rich” Doesn’t Make Us Better Off

Why “Taxing the Rich” Doesn’t Make Us Better Off

2020-09-29

The complete confiscation of all private property is tantamount to the introduction of socialism. Therefore we do not have to deal with it in an analysis of the problems of interventionism. We are concerned here only with the partial confiscation of property. Such confiscation is today attempted primarily by taxation.

Tags: Featured,newsletter