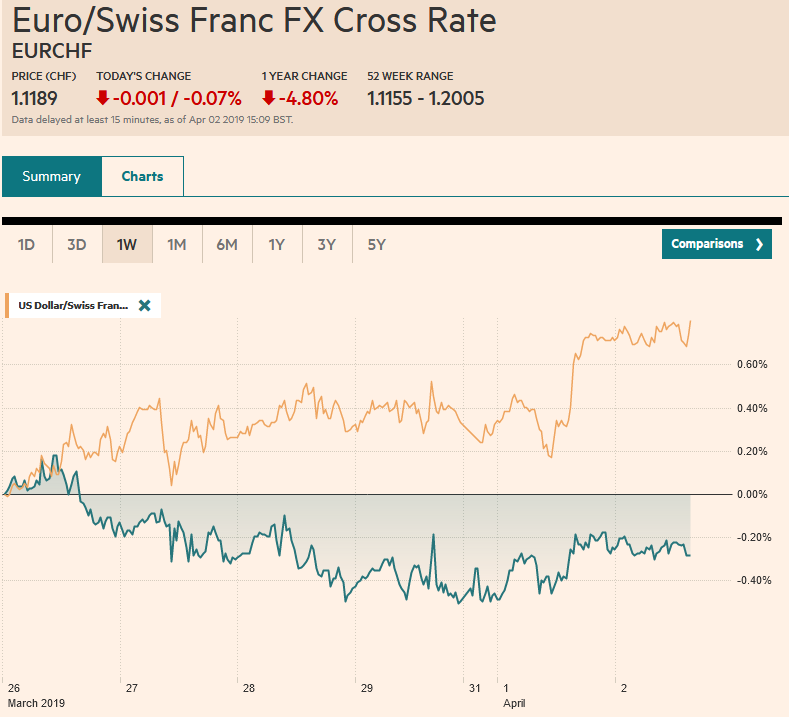

Swiss Franc The Euro has fallen by 0.07% at 1.1189 EUR/CHF and USD/CHF, April 02(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: After surging yesterday, equities are struggling to maintain the momentum that carried that S&P 500 to its best level since last October. Most Asia Pacific equity markets advanced. Japan’s small losses were a notable exception. The Dow Jones Stoxx 600 has advanced in four of the last five sessions and is little changed, while US shares are trading with a heavier bias. Yields edged up in Asia, but core yields in Europe are a little lower and the US 10-year yield, which jumped 10 basis points yesterday to 2.50% and re-inverted the

Topics:

Marc Chandler considers the following as important: 4) FX Trends, Brexit, EUR/CHF and USD/CHF, Featured, newsletter, RBA, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.07% at 1.1189 |

EUR/CHF and USD/CHF, April 02(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: After surging yesterday, equities are struggling to maintain the momentum that carried that S&P 500 to its best level since last October. Most Asia Pacific equity markets advanced. Japan’s small losses were a notable exception. The Dow Jones Stoxx 600 has advanced in four of the last five sessions and is little changed, while US shares are trading with a heavier bias. Yields edged up in Asia, but core yields in Europe are a little lower and the US 10-year yield, which jumped 10 basis points yesterday to 2.50% and re-inverted the 3m-10 year curve that had many observers warning of a recession is consolidating now, leaving it a couple basis points lower. In the foreign exchange market, the dollar is firmer against the majors. With uncertainty over Brexit as thick as ever, sterling has joined the Antipodean currencies as the worst performers, while the yen and Swiss franc are threatening to move higher. Note that yen and Swiss franc enjoy among the highest correlations on a directional basis for the past 18 months. |

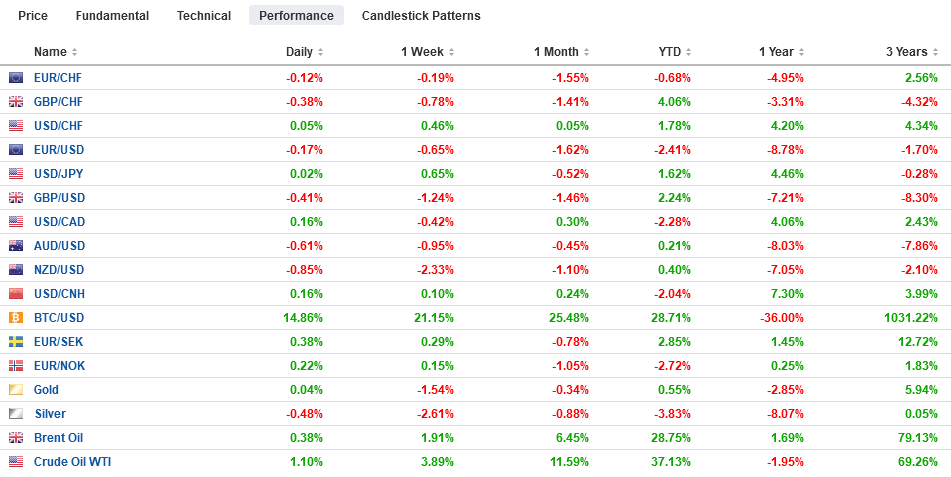

FX Performance, April 02 - Click to enlarge |

Asia Pacific

The Australian dollar is a bit of a conundrum today. The economic news seems supportive, but the Aussie has slipped to the lower end of its recent range (~$0.7060). The central bank’s decision to leaves on hold was no surprise, but the tone of the comments was more upbeat and did not sound like a central bank that was about to join the Reserve Bank in New Zealand and signal an easing bias. Although it recognized that consumption has been impacted by weakness in disposable income due to house prices, it noted that the strong labor market is underpinning wage growth. This underscores the importance of the labor market in the reaction function of the RBA, and therefore, the market will be particularly sensitive to employment and consumption data.

Separately, Australia reported a monster jump in building approvals. The median forecast in the Bloomberg survey was for a loss of nearly 2%. Instead, they surged 19.1%. This was enough to slash the year-over-year decline from almost 29% to 12.5%. Separately, though some may tie the RBA’s neutrality to it, the government unveiled its pre-election (May) budget. It includes A$158 bln in tax cuts over the next ten years and A$100 bln increase in spending. Lastly, the continued rally in iron ore prices (new two-year high) may be helping to lift miner equity prices, but it has not helped the Australian dollar.

After reporting disappointing trade numbers yesterday, South Korea reported soft inflation data today. The headline rate eased 0.2% in March. The median forecast in the Bloomberg survey expected a 0.2% gain. The year-over-year rate eased to 0.4% from 0.5%. It had been expected to rise to 0.7%. The core rate eased to 0.9%, which matches the cyclical low form last August. It had been expected to be unchanged at 1.3%.

Market-moving news from Japan and China were sparse. We note that Apple will reportedly cut iPhone prices in China by 6% and Foxconn indicated it may begin producing the iPhone in India. India is widely expected to cut interest rates on Thursday. It would be the second consecutive cut as the new central bank governor unwinds the two hikes that his predecessor delivered last year. Shades of Draghi and Trichet.

The dollar is in less than a 20 tick range against the Japanese yen today, trading mostly JPY111.30-JPY111.40. Note that the downtrend line drawn off last month’s highs is found today near JPY111.50. It may have to probe lower first before pushing closer to JPY112.00, where a $1.8 bln option expire tomorrow. There are about $1.7bln in options struck between JPY111.05 and JPY111.20 that expire today. The Australian dollar is nearly 1% off yesterday’s best levels. It appears to have found support near $0.7065. There is an A$1.1 bln option expiring today at $0.7100, and another one for A$1.2 expires tomorrow. Lastly, note that although mainland Chinese bonds were including in the Bloomberg/Barclay’s benchmark, the yield on China’s 10-year bond rose from 3.05% at the end of last week to 3.15% today, which is the highest since early March.

Europe

May was an accidental prime minister, and many see her leadership as weak. However, her challenges are also formidable and the House of Commons demonstrated yesterday the near impossibility of herding cats. May’s Withdrawal Bill may be detested (it lost 3 votes and may yet lose a fourth), but Parliament itself cannot agree on an alternative (much likely the debate about the Affordable Care Act in the US). Four different alternatives were voted on, and none received majority support. The customs union was the closest. It lost by three votes. The Tories themselves failed to support any measure. No more than 37 Conservatives supported any of the four measures. May has called an extra-long cabinet meeting today.

The risk of a national election appears to be growing as a way to break the logjam. It would be the third election in four years. Cameron had led legislation to introduce a regular election schedule, but like the idea that a referendum would unite the Tory Party, this too is not working too well in practice. While we have argued that Article 50 was triggered prematurely and without giving much thought to its obligations under the Good Friday Agreement, others have argued that May’s loss of a majority in the election she said she would not call in 2017 failed to lead to a change in strategy, leading to the current mess.

While US and Japanese trade talks are to being this month in the US, Europe and America’s trade talks may take a little longer to formally begin. Reports suggest that it is Macron who is balking. It is not over agriculture, which Europe wants to exclude (though reform of the Common Agriculture Program-CAP-would help EU free up funds that could be spent elsewhere) and the US wants to include. Rather Macron’s objections are over the role of climate and environment, a sore spot since the US withdrew from the Paris Accord.

The euro has been mostly confined to a 10-tick range on both sides of $1.12, where a 1 bln euro option expires today. The 18-month low set in early March was a little above $1.1175. Recall that it peaked near $1.1450 on the back of the dovish FOMC. It has fallen all but one day since. It is spending more time below its previous $1.13-$1.15 range. It appears to be entering a new range. We suspect the $1.1250 area may be the top end of the near-term range. Sterling is trading inside yesterday’s range, and the price action is choppy. There are around GBP1.5 in options struck between $1.3025 and $1.3055 that expire today. On the topside, yesterday’s high was near $1.3150, and the 20-day moving average is almost $1.3165.

America

Comments from Bank of Canada Poloz yesterday did not seem like a central banker ready to adopt an easing bias. While acknowledging that the economy still requires monetary stimulus, which means not hike, he saw the current slowdown as a temporary soft patch. Like Australia, Canada also goes to the polls this year (October), and the government has already submitted its election budget with tax cuts and spending increases.

Mexico’s government cut its growth forecast. This year’s outlook was cut to 1.1%-2.1% from 1.5%-2.5%. Next year’s forecasts were cut more: now 1.4%-2.4% from 2.1%-3.1%. The high-frequency data points have been soft. Worker remittances in February were light (by ~$100 mln vs. expectations) and the Markit manufacturing PMI slipped below the 50 boom/bust level in March to 49.8 (from 52.6) the low Q1.

The US reports February durable goods orders today. They were likely weighed down by a drop in aircraft orders. Excluding aircraft and defense, a small gain is expected after a 0.8% gain in January. However, barring a significant disappointment, the market (and policymakers) appear to be looking past Q1. February retail sales reported yesterday were disappointing, and although the upward revision in the January series offset the weakness in full, it does appear that real consumption slowed considerably from the 2.5% pace in Q4 18. The March ISM is more promising. Broad gains were reported, especially in employment (biggest increase in four years) and the strongest prices paid since September 2017. New orders increased for the third consecutive month. Construction spending rose 1% in February. Economists expected a small decline. The January report was revised; nearly doubling the initial estimate of 1.3% to 2.5%.

The US dollar is finding support against near CAD1.3300. Initial resistance is pegged near CAD1.3340. All three drivers of the Canadian dollar are supportive. Oil prices are firm, with May WTI near $62 a barrel. Note that $63.45 is a 61.8% retracement of the decline from Q4 18, and our technical objective is near $67. The risk-on mood is firm even if it is consolidating today. The Canadian discount to the US on two-year money is the smallest in two months (near 69 bp). The dollar found support against the Mexican peso a little below MXN19.15. We like the US dollar higher.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,EUR/CHF and USD/CHF,Featured,newsletter,RBA