Rulers found out early on that they could debase gold and silver coins for their own gain. As a consequence, the money supply increased, whereas money’s purchasing power fell. This pseudoalchemy is the true definition of inflation and has been a policy for more than a thousand years. What’s more, an increase in the money supply leads to rising prices. This symptom of inflation is often mistaken as inflation itself. The correct term, though, is price inflation. Moreover, inflation creates boom-bust cycles and redistributes wealth, which results in winners and losers. In a world of governments, inflation is inevitable since it is advantageous to the ruling class. Though we can’t escape this dreadful disease, we can learn to better deal with its symptoms—starting

Topics:

Andreas Granath considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Rulers found out early on that they could debase gold and silver coins for their own gain. As a consequence, the money supply increased, whereas money’s purchasing power fell. This pseudoalchemy is the true definition of inflation and has been a policy for more than a thousand years.

What’s more, an increase in the money supply leads to rising prices. This symptom of inflation is often mistaken as inflation itself. The correct term, though, is price inflation.

Moreover, inflation creates boom-bust cycles and redistributes wealth, which results in winners and losers.

In a world of governments, inflation is inevitable since it is advantageous to the ruling class. Though we can’t escape this dreadful disease, we can learn to better deal with its symptoms—starting with knowledge.

Hence, I would like to share some insights I wish I had learned before the massive covid money pumping began in 2020.

The Price of Money and Consumer Price Indexes

The price of any good or service is expressed in money. If the money price of a pen is one dollar, the pen price of a dollar is one pen. Note that money is a common denominator, whereas a good, such as a pen, is not. We cannot say that the price of a dollar is one pen. So, the price of a dollar must be expressed in each and every good and service, in order to determine its purchasing power.

Yet, attempts have been made to determine the purchasing power of money through consumer price indexes. These indexes are said to reflect a population’s consumption. Regarding the Consumer Price Index (CPI) in the United States, the Bureau of Labor Statistics writes on its website: “The CPI represents changes in prices of all goods and services purchased for consumption by urban households.”

The CPI simply cannot include all goods and services. Also, it leaves out many of those goods and services purchased individually. It is, therefore, deceiving to view the CPI as a measure of the personal (price) inflation rate.

If we take a closer look at the CPI, we find it being divided into eight major groups of goods and services. Should we zoom in further, we find that there are more than two hundred smaller groups within these eight. Furthermore, we see that the rate of increase differs for different groups—which brings us to the next insight.

The Cantillon Effect

Some economists and laymen believe in the neutrality of money. This means that changes in the money supply affect all prices simultaneously and proportionally. However, as Irish banker Richard Cantillon noted almost three hundred years ago, money is not neutral.

Suppose that you owned a printing press in your garage that could print a thousand hundred-dollar bills per day. At first, the printing press would favor you since you could spend your money before prices rise.

To simplify, let’s say you go out and spend your newly printed money on sports cars from a local dealership. As a result, the car dealer makes more money, which he spends on suits from a local tailor. After a while, the dealer also starts raising his prices due to the increased demand.

The car dealer keeps spending his money on suits, and soon, the tailor starts raising his prices to meet the increasing demand. Furthermore, the tailor has a penchant for antiques, which he buys from a local dealer. So it goes, until the money has spread throughout the economy.

From this phenomenon, known as the Cantillon effect, we can draw some conclusions. First, the earlier recipients of the new money benefit from it at the expense of the later recipients. Second, the largest increase in prices will typically be where the money first enters. Third, prices are affected singly and disproportionately.

Inflation Hedging According to Mainstream Economists

Many investors and mainstream economists suggest investing in the stock market, precious metals, or real estate to hedge against inflation. There is much truth to this. However, these investors and economists fail to explain why and when to invest in these types of investments.

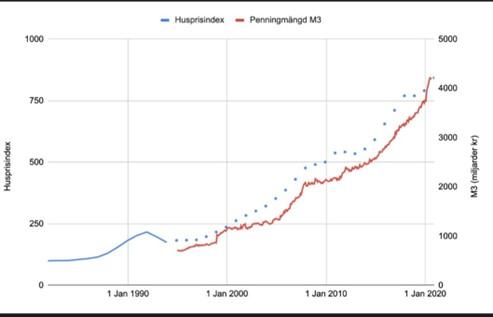

Most of today’s money is created whenever commercial banks make loans, where the money then flows into capital goods and real estate. In the diagram below, we see that the Swedish M3 money supply correlates well with the Swedish house price index.

Figure 1: Swedish M3 money supply and house price index, 1980–2023

Source: Data from scb.se.

Furthermore, central banks buy securities in order to inflate the money supply. This act is known as quantitative easing (QE). Whenever the banks feel the inflation target is reached, they begin to sell off their securities (or raise interest rates). Thereby, they are engaging in what is called quantitative tightening (QT).

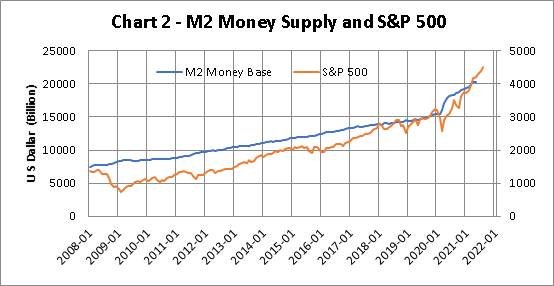

Below, we see the M2 money supply for the US and the S&P 500. Quite the correlation.

Figure 2: US M2 money supply and S&P 500, 2008–22

Source: M2 data from “M2 (WM2NS),” Board of Governors of the Federal Reserve, FRED; S&P 500 data from stooq.com.

In March 2020, the Federal Reserve began its $700 billion QE program along with a zero-interest-rate policy. As expected, the stock market rose significantly. However, in late 2021, the Fed started reducing its purchases. In March 2022, they reverted and commenced QT.

Consequently, the stock market fell in the beginning of 2022 and reached its lowest point in October of that year.

Meanwhile, the twelve-month CPI stayed under 2.0 percent between March 2020 and February 2021. When the stock market peaked in late December 2021, the CPI was up to 7.0 percent.

When the CPI peaked in June 2022 at 9.1 percent, the S&P 500 was down about 25 percent from its highest in January 2022. Thus, he who tried to hedge against the CPI by investing in a stock market index at that time would have been in dire straits.

Conclusion

The purchasing power of money declines over time due to an increase of the money supply. It then follows that the prices of most goods and services increase. However, since money is not neutral, prices will increase disproportionately.

Thus, in order to protect ourselves from inflation, we must follow the money. Where large amounts of money are injected, that’s where we need to be.

Finally, one should consider one’s personal inflation rate and try to compensate by increasing one’s income. At the end of the day, real income is what counts.

Tags: Featured,newsletter