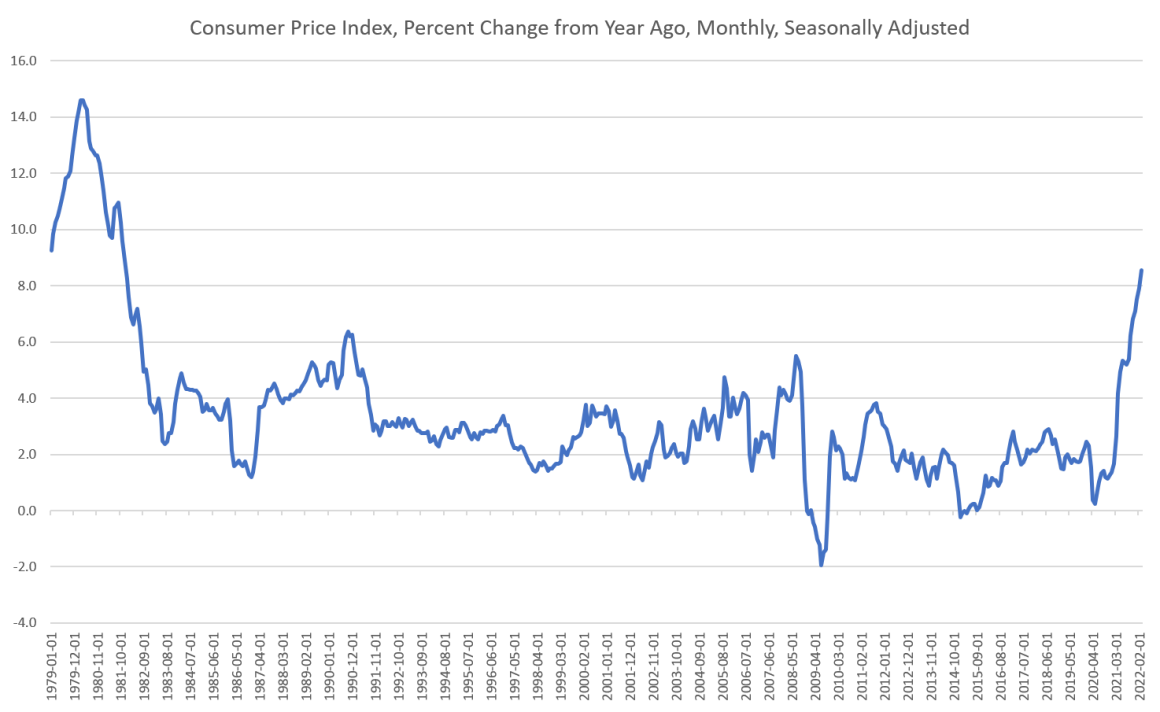

The government’s latest report puts the twelve-month official consumer price inflation rate at 8.5 percent, the highest since December 1981: As economists debate the causes of, and cure for, this price inflation, it’s worth recounting which schools of thought saw it coming. Although individuals can be nuanced, generally speaking the Austrians have been warning that the Fed’s reckless policies threaten the dollar. In contrast, as I will document in this article, two of the leaders of the Keynesian and market monetarist schools didn’t see this coming at all. . My Worst Professional Mistake Before diving into it, I need to address a problem: my hands-down worst professional mistake occurred during the early years of the Fed’s “QE” (quantitative easing) programs,

Topics:

Robert P. Murphy considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The government’s latest report puts the twelve-month official consumer price inflation rate at 8.5 percent, the highest since December 1981:

As economists debate the causes of, and cure for, this price inflation, it’s worth recounting which schools of thought saw it coming. Although individuals can be nuanced, generally speaking the Austrians have been warning that the Fed’s reckless policies threaten the dollar. In contrast, as I will document in this article, two of the leaders of the Keynesian and market monetarist schools didn’t see this coming at all. |

. |

My Worst Professional Mistake

Before diving into it, I need to address a problem: my hands-down worst professional mistake occurred during the early years of the Fed’s “QE” (quantitative easing) programs, when I made bets on (consumer price) inflation with two economist colleagues. I ended up losing those bets and thereby gave Paul Krugman the opportunity to lecture me on my intellectual dishonesty because I clung to my (ostensibly falsified) Austrian model even after my prediction blew up in my face. Indeed, if you check out my Wikipedia entry, you’ll see that apparently my life story is that I was born, got my PhD, and lost an inflation bet—in that order. (For those interested in the details, I summarize the episode with relevant links in this postmortem blog post. I also participated in a 2014 Reason symposium along with Peter Schiff and others, commenting on the lack of inflation.)

Ever since the rounds of QE failed to yield surging consumer price inflation at the scale some of us warned of, the Keynesians and market monetarists understandably ran victory laps, saying that they were to be trusted over those permabear Cassandra Austrians. (To be sure, the market monetarists were far more civil about it than the prominent Keynesians.) So it is not with gloating or vindictiveness that I write the present article, but rather I do it to set the record straight and document for posterity that the leading Keynesians and market monetarists totally missed this bout of price inflation.

The Keynesians Camp: Paul Krugman and Klaus Schwab

Let’s do the fun one first: Paul Krugman has not fared well in light of our current inflationary experience. As late as June 2021, Krugman wrote an article in the New York Times titled “The Week Inflation Panic Died.” Here are some key excerpts, with my bold added, and keep in mind that when Krugman wrote this, the most recent Consumer Price Index (CPI) inflation rate was only 4.9 percent:

Remember when everyone was panicking about inflation, warning ominously about 1970s-type stagflation? OK, many people are still saying such things, some because that’s what they always say, some because that’s what they say when there’s a Democratic president….

But for those paying closer attention to the flow of new information, inflation panic is, you know, so last week.Seriously, both recent data and recent statements from the Federal Reserve have, well, deflated the case for a sustained outbreak of inflation …

o panic over inflation, you had to believe either that the Fed’s model of how inflation works is all wrong or that the Fed would lack the political courage to cool off the economy if it were to become dangerously overheated.

Both beliefs have now lost most of whatever credibility they may have had….The Fed has been arguing that recent price rises are similarly transitory … The Fed’s view has been that this episode, like the inflation blip of 2010–11, will soon be over.

And it’s now looking as if the Fed was right …

…. Monetary doomsayers have been wrong again and again since the early 1980s, when Milton Friedman kept predicting an inflation resurgence that never arrived. Why the eagerness to party like it’s 1979?To be fair, government support for the economy is much stronger now than it was during the Obama years, so it makes more sense to worry about inflation this time around. But the vehemence of the inflation rhetoric has been wildly disproportionate to the actual risks—and those risks now seem even smaller than they did a few weeks ago.

Of course, Krugman’s confident dismissal of those Biden-hating doomsayers blew up in his face, as CPI inflation kept ratcheting higher and higher. In a December 2021 NYT column, Krugman threw in the towel and admitted he had been wrong, but in his own special way (again, with my bolding):

The current bout of inflation came on suddenly…. Even once the inflation numbers shot up, many economists—myself included—argued that the surge was likely to prove transitory. But at the very least it’s now clear that “transitory” inflation will last longer than most of us on that team expected….

… I believe that what we’re seeing mainly reflects the inherent dislocations from the pandemic, rather than, say, excessive government spending. I also believe that inflation will subside over the course of the next year and that we shouldn’t take any drastic action. But reasonable economists disagree, and they could be right….

The latest projections from board members and Fed presidents are for the interest rate the Fed controls to rise next year, but by less than one percentage point, and for the unemployment rate to keep falling.

Perhaps surprisingly, my own position on policy substance isn’t all that different from either Furman’s or the Fed’s. I think inflation is mainly bottlenecks and other transitory factors and will come down, but I’m not certain, and I am definitely open to the possibility that the Fed should raise rates, possibly before the middle of next year….

Maybe the real takeaway here should be how little we know about where we are in this strange economic episode. Economists like me who didn’t expect much inflation were wrong, but economists who did predict inflation were arguably right for the wrong reasons, and nobody really knows what’s coming.

For those keeping score at home, remember that when I pointed out that Keynesians Christina Romer and Jared Bernstein had been notoriously wrong in their forecasts of unemployment following the Obama stimulus package, Krugman told us that “some predictions matter more than others.” So this time around, Krugman can’t argue that his botched inflation predictions are irrelevant. Instead, as we see above, he’s claiming that his opponents were right but for the wrong reasons. Even when Krugman is wrong, he’s still better than his enemies!

And for the sake of completeness, let’s reproduce this quotation from Klaus Schwab (who has doctoral degrees in both economics and engineering) and Thierry Malleret in COVID-19: The Great Reset. Writing in July 2020, Schwab and Malleret claimed:

At this current juncture, it is hard to imagine how inflation could pick up anytime soon…. The combination of potent, long-term, structural trends like ageing and technology … and an exceptionally high unemployment rate that will constrain wages for years puts strong downward pressure on inflation. In the post-pandemic era, strong consumer demand is unlikely. (p. 70)

So when he’s not plotting to take over the world, Klaus Schwab is making erroneous inflation predictions.

The Leader of the Market Monetarists, Scott Sumner

As I said earlier, the market monetarists are far more civil than Krugman, Brad DeLong, and some other leading Keynesians. (And as far as I know, they’re not bent on world domination either.) But to repeat myself: since 2008, the one trump card the market monetarists had in their rivalry with the Austrians was that many of us prematurely warned about consumer price inflation à la the 1970s, whereas the market monetarists relied on TIPS (Treasury inflation-protected securities) yields and other market indicators to reassure their readers that inflation wouldn’t be a problem.

In that context, then, it’s very interesting that Scott Sumner, founder and leader of the market monetarists, wrote a blog post entitled, “Fed Policy: The Golden Age Begins,” in January 2020. Here are the key excerpts, with my bold:

We are entering a golden age of central banking, where the Fed will become more effective and come closer to hitting its targets than at any other time in history. Over the next few decades, inflation will stay close to 2% and the unemployment rate will generally be relatively low and stable. And this certainly won’t be due to fiscal policy, which is currently the most recklessly pro-cyclical in American history.

… Fed policy is becoming more effective because it is edging gradually in a market monetarist direction….

If they continue moving in this direction, then NGDP [nominal gross domestic product] growth will continue to become more stable, the business cycle will continue to moderate, inflation will stay in the low single digits, and unemployment will stay relatively low and stable.

It won’t be perfect; the business cycle is not quite dead. There will be an occasional recession. But the business cycle is definitely on life support….

As an analogy, when I was young I would frequently read about airliners crashing in the US…. My daughter is a junior in college and doesn’t recall a single major airline crash in the US, excluding a couple of small commuter planes in the 2000s…. After each crash, problems were fixed and planes got a bit safer.

Recessions and airline crashes: They are getting less frequent, and for the exact same reason.

Before closing, let me deal with the obvious response from the market monetarist camp: They could defend Sumner’s claims by arguing that the Fed only strayed from the ideal path because of covid. Well, sure, but Sumner was still wrong for placing so much faith in central bankers and their “independence.”

Furthermore, as I explain in my chapter on market monetarism in this book, Sumner’s criterion of “NGDP growth” as a measure of tight or loose policy is almost a tautology. It is close to me arguing, “We will continue to see rising prices because of the Fed’s reckless policies, unless demand growth subsides, in which case we won’t.”

You Might Also Like

Achtung Inflation: Wohlstand in Gefahr! (JF-TV Interview mit Thorsten Polleit)

2022-04-14

Seit 2021 steigt die Inflationsrate kontinuierlich an, lag im März dieses Jahres bei besorgniserregenden 7,3 Prozent. In Medien und Politik wird diese Entwicklung oft mit dem Krieg in der Ukraine assoziiert, in Wahrheit liegen die Gründe jedoch viel tiefer, wie der Chefökonom der Degussa Goldhandel, Thorsten Polleit, im JF-TV Interview erklärt. Und Polleit fürchtet: “Diese Inflation ist gekommen um zu bleiben”, selbst eine vorrübergehend zweistellige Inflationsrate im Euroraum hält der Ökonom für möglich. Damit verteuern sich Waren und Dienstleistungen dramatisch, während Ersparnisse ihren Wert verlieren. Wieso die Bürger vom Staat in diesem Zusammenhang keine Hilfe erwarten sollten und was sie selbst tun können, ihr Vermögen zu schützen, erklärt der Ökonom zum Ende des Gespräches.

Sehr

Heavy Sanctions against Russia Could Usher in a Wider Economic War

2022-04-11

Vladimir Putin’s invasion of Ukraine was met with unprecedented economic sanctions by the United States and its allies in order to cripple Russia’s capacity to wage war. Never before in post–World War II history has an economy of Russia’s size been reprimanded with such force. Moreover, the sanctions could remain in place after the war ends and reach other major economies too, in particular China. In this case, current sanctions could be the harbinger of a longer-term economic war with dire consequences for global productivity and welfare.

Sweeping Sanctions Invite Countersanctions

The round of sanctions imposed on Russia following the annexation of Crimea in 2014 were limited to travel bans, freezing of the assets of certain Russian officials, and a prohibition of credit and technologyThe Fed Has No Real Plan, and Will Likely Soon Chicken Out On Rate Hikes

2022-01-27

The Fed’s Federal Open Market Committee (FOMC) released a new statement today purporting to outline the FOMC’s plans for the next several months. According to the committee’s press release: With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate.

Andrew Moran: NBA skills trainer on Tyler Herro offseason workout, and strong start to the season.

2022-01-26

In this segment NBA skills trainer Andrew Moran talks about Tyler Herro offseason workout, mindset, comments about being one of the top players, and a strong start to the season

Fiye show: https://www.instagram.com/fiye.show/

Miami Hoop School: https://www.instagram.com/miamihoopsc…

Miami Hoop School website: https://www.miamihoopschool.com/

Miami hoop school academy Instagram: https://www.instagram.com/miamihoopschool_academy/Life Expectancy in 2020 Fell 2.3 Percent to 77 Years. Does This Justify the Covid Panic?

2021-12-26

According to a new report released Wednesday by the Centers for Disease Control, the life expectancy at birth in the United States fell to 77.0 iyears n 2020, falling from 2019’s life expectancy of 78.8 years. The report also noted an increase of mortality with age-adjusted mortality in the US rising from 715.2 per 100,000 in 2019 to 836.4 per 100,000 in 2020.

Markieff Morris workouts with Mariano Sánchez and Andrew Moran in Las Vegas

2021-11-29

Todo lo necesario para compensar el juego interior en @lakers complementando a figuras @keefmorris5.0 se ganó un espacio de respeto en equipos donde necesitan ser finos en oportunidades externas y en la zona ! Un jugador con excelente tiro ! Runners + floaters y entrando a jugar en la zona con personalidad en sus comportamientos tácticos ! Todo bajo timing y técnica . Días de progresión asistiendo a @miamihoopschool en Las Vegas ! Una continua progresión durante años en sus recursos hacia situaciones de juego, conditioning + efectividad , que desglosaremos en clinics y entrenamientos para formación ! ??

Tags: Featured,newsletter

Permanent link to this article: https://snbchf.com/2022/04/p-murphy-keynesians-market-monetarists-didnt-see-inflation/

On Swiss National Bank

SNB Sight Deposits: Inflation and WAR is there, CHF must Rise

Macro Week 2022: Thomas Jordan

Switzerland has frozen CHF7.5bn in assets under Russia sanctions

UBS-Präsident Axel Weber verabschiedet sich mit Genugtuung

Andréa M. Maechler / Thomas Moser: Life after Libor: A new era of reference interest rates

Featured and recent

More from this category

Zahlungen mit Cryptocoins auf Amazon noch weit entfernt

19 Apr 2022

Debt Saturation: Off the Cliff We Go

19 Apr 2022

Crypto Nation Switzerland tackles workforce shortages

19 Apr 2022

How the Fed’s Tampering with the Policy Rate Affects the Yield Curve

19 Apr 2022

Keynesians and Market Monetarists Didn’t See Inflation Coming

19 Apr 2022

Greenback Starts New Week on Firm Note

18 Apr 2022

Swiss consumed 4.3 percent more electricity in 2021

18 Apr 2022

Hoppe: “My Dream Is of a Europe Which Consists of 1,000 Liechtensteins.”

18 Apr 2022

Students demand a bitcoin education

18 Apr 2022

Swiss government prepares for electricity price shock

18 Apr 2022

Yield Curve Inversion Was/Is Absolutely All About Collateral

18 Apr 2022

Is There a Case for the Pre-1914 Gold Standard? Yes, if You Believe Inflation is a Bad Thing

18 Apr 2022

Social Media Financial Scams Balloon

17 Apr 2022

Darshan Mehta: Insights Are Game Changers For Business

17 Apr 2022

China More and More Beyond ‘Inflation’

17 Apr 2022

Alabama Passes Sound Money Law, Expands Sales Tax Exemption Involving Gold and Silver

17 Apr 2022

Are the days of morally neutral corporate decision-making over?

17 Apr 2022

NFT des ersten Twitter-Tweets verliert massiv an Wert

16 Apr 2022

Is The Ruble Backed By Gold Now?

16 Apr 2022

Swiss bail-out plan aims to prevent electricity crunch

16 Apr 2022

Leave a Reply