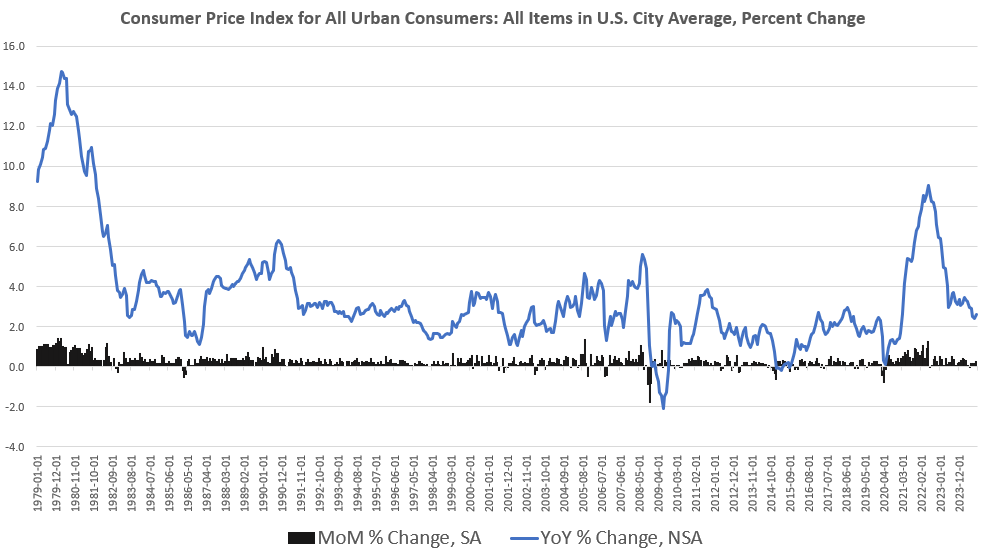

According to the Bureau of Labor Statistics’ latest price inflation data, CPI inflation in October accelerated and month-to month increases in CPI inflation hit multi-month highs.The seasonally adjusted Consumer Price Index (CPI) rose 0.24 percent month over month in October, rising to a six-month high. Year over year, the CPI rose 2.49 percent in October, not seasonally adjusted. That’s a three-month high.The ongoing price increases largely reflect growth in prices for shelter. Year over year, shelter prices rose 4.9 percent, according to the BLS report. That’s up from September’s year-over-year increase of 4.8 percent.Similarly, the CPI measure, less food an energy, also showed increases with a month-over-month growth rate of 0.28 percent. Year over year, the

Topics:

Ryan McMaken considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

According to the Bureau of Labor Statistics’ latest price inflation data, CPI inflation in October accelerated and month-to month increases in CPI inflation hit multi-month highs.

The seasonally adjusted Consumer Price Index (CPI) rose 0.24 percent month over month in October, rising to a six-month high. Year over year, the CPI rose 2.49 percent in October, not seasonally adjusted. That’s a three-month high.

The ongoing price increases largely reflect growth in prices for shelter. Year over year, shelter prices rose 4.9 percent, according to the BLS report. That’s up from September’s year-over-year increase of 4.8 percent.

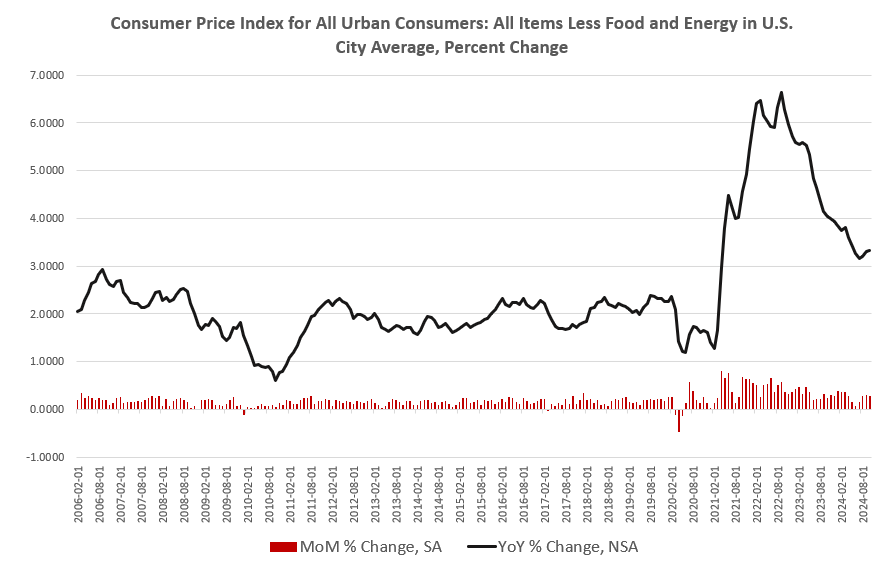

Similarly, the CPI measure, less food an energy, also showed increases with a month-over-month growth rate of 0.28 percent. Year over year, the same index showed prices increasing by 3.3 percent, the highest in six months. The year-over-year growth in this measure has now increased three months in a row.

The downward trend in price inflation that we saw in late summer has now stalled. Moreover, accumulated growth in the CPI continues unabated, with no relief in sight for middle- or lower-income consumers.

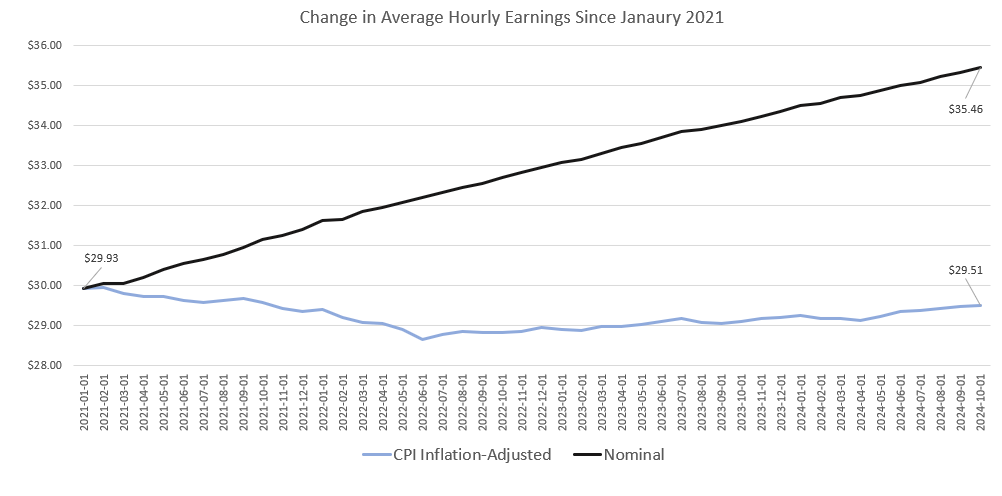

Since January 2021, for example, the consumer price index has increased by 20 percent. Wages have not kept up with rising prices, however. Looking at growth since 2021, we see that average hourly earnings increased by about five dollars while real average hourly earnings fell by 50 cents. In other words, workers have still not recovered from the aggregate inflation of recent years.

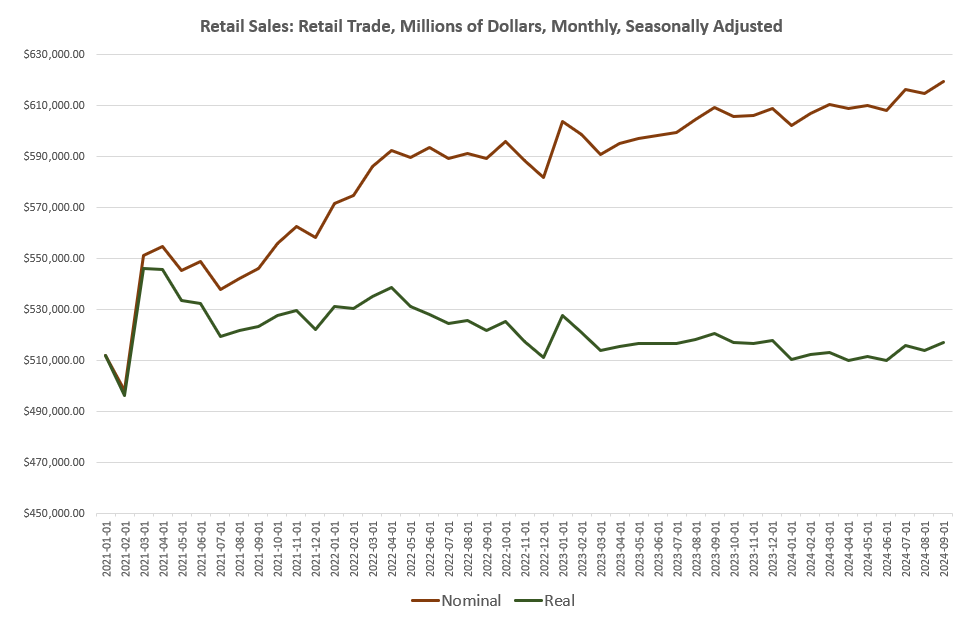

We can make similar comparisons in other areas of the economy as well. For example, if we look at retail sales, the nominal increase since 2021 is 21 percent. Once we adjust for the CPI, however, we find the increase in retail sales is a mere 0.9 percent. All those “solid gains” in retail that the media tells us about don’t look so excellent after all.

The effects of inflation on workers over time have generally been ignored by the media and regime spokesmen. Interestingly, however, Jerome Powell at last week’s FOMC press conference admitted that workers have not yet recovered from the mounting price inflation of recent years. When asked why so many voters appeared dissatisfied with the economy, Powell explained that, even though recent price inflation numbers have moderated, workers are still feeling the aggregate effects of inflation over several years.

Remote video URL

Indeed, Powell has largely abandoned the confident posture he had adopted during the September FOMC press conference. In September, when the Fed saw fit to slice the federal funds rate by fifty basis points, Powell assured his audience that inflation rates were clearly returning to the two-percent target and the Fed was therefore free to concentrate on maintaining strong employment numbers. Such a large cut in the target rate suggested the Fed was confident price inflation would continue to decelerate.

Things don’t seem to have worked out. In contrast to September, Powell yesterday struck a far more cautious tone on price inflation and stated “The economy is not sending any signals that we need to be in a hurry to lower rates.”

One might wonder how, if this is true, the FOMC felt the need to cut by 50 basis points in September.

We are unlikely to every receive a straight answer on this from anyone at the Fed, but there are a couple of possibilities. One option is that the Fed simply wanted to give the economy a monetary shot in the arm in mid-September in order to help the incumbent vice president win re-election. Powell will never admit to this, even if it is true. Another possibility is that the Fed really did believe in September that price inflation would continue to fall consistently. If that is the case, then the Fed and its legions of economists miscalculated. A third option is that the Fed sees a recession coming and hit the panic button when it cut the target rate by 50 bps.

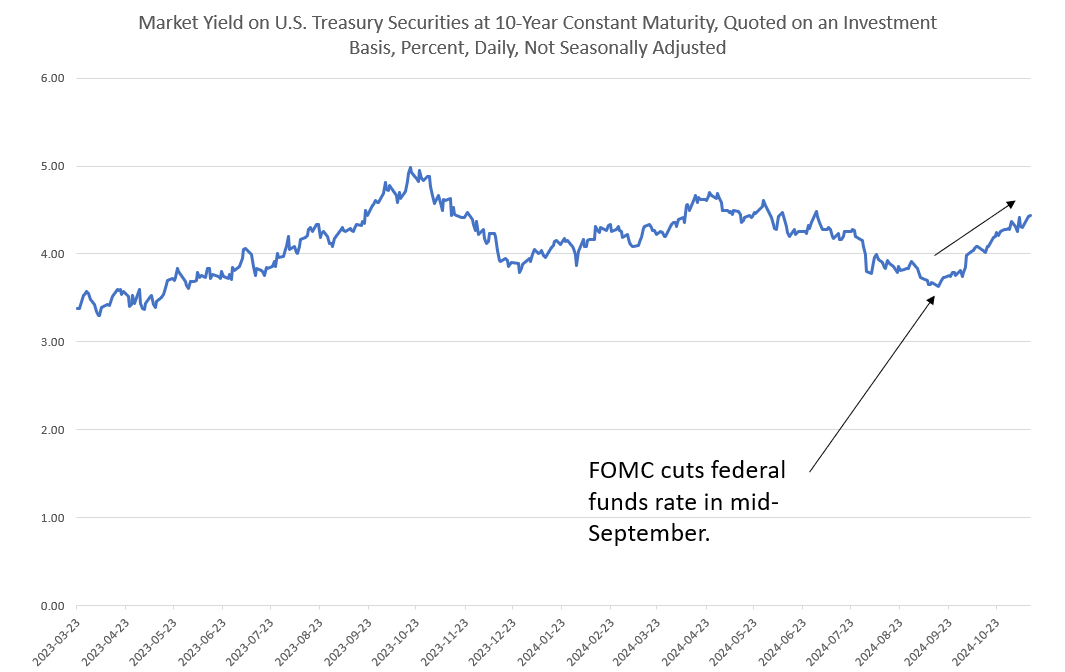

In any case, bond investors appear to have never bought the narrative that price inflation has been conquered and is headed to two percent or less. As we noted here at mises.org yesterday, almost as soon as the Fed cut the federal funds rate in September, longer-term interest rates began to rise signaling that many bond investors expect more price inflation moving forward.

Tags: Featured,newsletter