With the acknowledged national debt now a politically and economically unpayable trillion (in reality, its unfunded liabilities are far greater), Americans should start to become acclimated to the realities of the United States’ eventual, inevitable default. While it may seem unfathomable, and the results too catastrophic to imagine, in fact the likely damage to everyday Americans would be minimal in the short term and unquestionably a net plus in the long term. This is far from surprising and not a new problem. As Carmen M. Reinhart and Kenneth S. Rogoff detail in their comprehensive review of the subject, history shows that great powers defaulting on their debts was long the rule, not the exception, and that the long-term implications of various

Topics:

Joseph Solis-Mullen considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

With the acknowledged national debt now a politically and economically unpayable $30 trillion (in reality, its unfunded liabilities are far greater), Americans should start to become acclimated to the realities of the United States’ eventual, inevitable default. While it may seem unfathomable, and the results too catastrophic to imagine, in fact the likely damage to everyday Americans would be minimal in the short term and unquestionably a net plus in the long term.

With the acknowledged national debt now a politically and economically unpayable $30 trillion (in reality, its unfunded liabilities are far greater), Americans should start to become acclimated to the realities of the United States’ eventual, inevitable default. While it may seem unfathomable, and the results too catastrophic to imagine, in fact the likely damage to everyday Americans would be minimal in the short term and unquestionably a net plus in the long term.

This is far from surprising and not a new problem. As Carmen M. Reinhart and Kenneth S. Rogoff detail in their comprehensive review of the subject, history shows that great powers defaulting on their debts was long the rule, not the exception, and that the long-term implications of various regimes’ repudiations of their external debts in particular were minimal or a net plus, depending on the circumstances.

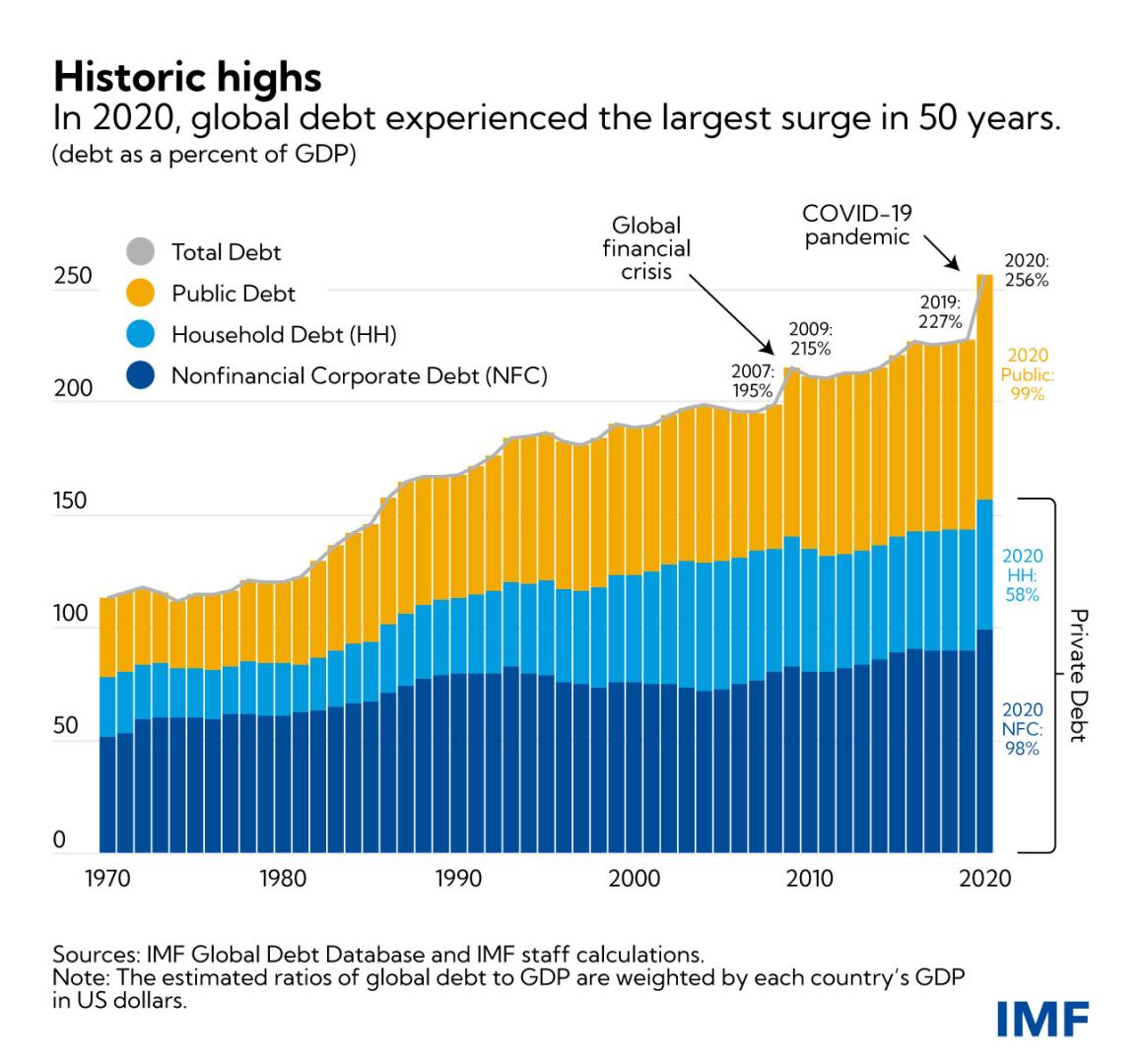

As a way of starting, it is helpful to contextualize the current numbers we’re talking about, because, frankly, they would have been unfathomable previously. As the old math joke “What is the difference between a million and a billion? Basically, a billion” illustrates, the orders of magnitude under discussion are scarcely comprehensible. But the reality is that trillion dollars is $999 billion plus another billion.

The present debt level has only been manageable because of the artificially low interest rates provided by successively accommodating Federal Reserve chairs dating back to Alan Greenspan. With both fiscal and monetary policy having been run heedlessly off the rails for twenty years, the reckoning of a higher interest rate environment necessarily awaits. Short of cuts in annual spending drastic enough to produce large running surpluses (not likely), default is the only sensible option toward which to encourage policy makers.

For context, consider that when Ronald Reagan and the Democrats controlling Congress started running budget deficits that hadn’t been seen since the Second World War, the national debt was running in the hundreds of billions—eventually jumping into the low single-digit trillions.

In the 1990s, as the unipolar moment was beginning, successive administrations and Congress seemed to recognize the foolishness of their previous policies. Compelled by grassroots activism and insurgent Republican candidacies, George H.W. Bush and Bill Clinton both made deals to cut spending and raise taxes. By the time Clinton left office, the country was running a budget surplus and the national debt was projected to be paid off by the end of the decade.

Then came George W. Bush and his disastrous wars of choice. The size and scope of the government grew at the same time that historic tax cuts were enacted. The words of then vice president Dick Cheney should have spooked foreign buyers of US debt more than they did. He was of the opinion that “deficits don’t matter.”

Nor did they matter to Barack Obama, his successors, or their congressional partners—to the point that the mere $30 trillion in openly acknowledged debt amounts to over $80,000 per American.

Nor did the regular trillion-dollar deficits matter to the Fed, which with its accommodating and regularly mandate-violating policies has raised the stakes of the coming financial oppression orders of magnitude higher than they would have been had interest rates been determined formulaically or purely by market forces.

The good news, at least for ordinary Americans, is that we personally just don’t hold very much of the debt. Fully two-thirds is held between the Fed, various other US government entities, and foreign governments. A US government default wouldn’t be the first time the latter have taken a haircut (Alexander Hamilton and Richard Nixon both undertook such necessary actions), and our own government has spent the money so poorly that no coherent argument can be made that justifies paying them back. They would just continue in their profligate ways. As for Wall Street, they’ve lived on corporate welfare long enough to justify their taking a one-time bath.

Apart from not paying perpetual interest on ever-increasing debt, another benefit of default, rarely mentioned but arguably one of the most important from the antiwar libertarian perspective, is that it would essentially end Washington’s ability to practice unbridled military Keynesianism. Slapping pointless wars and military buildups on the credit card has become Congress’s standard operating procedure. It is not a coincidence that our annual trillion-dollar deficits are approximately equal to the trillion dollars dumped into the the military-industrial complex black hole each year.

With foreign investors temporarily alienated, the Fed would be faced with the choice of either absorbing the entire amount of “defense” spending with its own balance sheet (thus sparking a drastic inflationary bout that would visibly discredit the unconstitutional institution) or forcing Washington to give up the myth of global military indispensability.

Either case is preferable to the current course.

It is in the interests of the American people, our children, and our grandchildren, and would arguably do more for world peace than any other realistic scenario imaginable.

So, contact your representative today and tell them you support defaulting on the debt.

You Might Also Like

Roots of Our Current Inflation: A Deeply Flawed Monetary System

Roots of Our Current Inflation: A Deeply Flawed Monetary System

2022-05-08

A monetary system that allows the creation of money out of thin air is vulnerable to the fits of credit expansion and credit contraction. Periods of credit expansion typically occur over many years and even decades while the phases of credit contraction happen like sudden implosions. The monetary policy makers tend to promote the prolongation of credit expansion because they fear deflation.

How Did CNN+ Get Canned by Netflix? Austrian Economists Might Have an Answer

How Did CNN+ Get Canned by Netflix? Austrian Economists Might Have an Answer

2022-04-27

Days after Netflix reported bad earnings and an “unexpected” hit to their subscriber base, CNN announced that it had pulled the plug on its own brand-new streaming service, CNN+. Despite arguments to the contrary from the parent company, the CNN+ adventure turned out to be a costly mistake that attracted few subscribers and a paltry number of regular viewers.

The Nationalities Question

The Nationalities Question

2022-04-22

[This article was published in in The Irrepressible Rothbard, available in the Mises Store.]

Upon the collapse of centralizing totalitarian Communism in Eastern Europe and even the Soviet Union, long suppressed ethnic and nationality questions and conflicts have come rapidly to the fore. The crack-up of central control has revealed the hidden but still vibrant "deep structures" of ethnicity and nationality.

To those of us who glory in ethnic diversity and yearn for national justice, all this is a wondrous development of what has previously lived only in fantasy or longing: it is a chance in Europe at long last, to begin to reverse the monstrous twin injustices of Sarajevo and Versailles. It is like being back in 1914 or 1919 again, with a chance for the map of Europe and near Asia to be

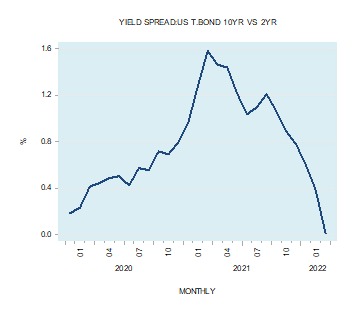

How the Fed’s Tampering with the Policy Rate Affects the Yield Curve

How the Fed’s Tampering with the Policy Rate Affects the Yield Curve

2022-04-19

At the end of March this year the difference between the yield on the ten-year Treasury bond and the yield on the two-year Treasury bond fell to 0.010 percent from 1.582 percent at the end of March 2021.

Money and Savings Are Not the Same Thing

Money and Savings Are Not the Same Thing

2022-02-17

In the National Income and Product Accounts (NIPA), savings are established as the difference between disposable money income and monetary outlays. Disposable income is defined as the summation of all personal money income less tax payments to the government. Personal income includes wages and salaries, transfer payments, income from interest and dividends, and rental income.

The NIPA framework is based on the Keynesian view that spending by one individual becomes part of the income of another individual. The spending of the purchaser is the income of the seller. From this, it follows that spending equals income.

So if people maintain their spending, this keeps overall income coming in. Now, an increase in the supply of money affects the total amount of money spent. Consequently, the

The Divided States of America | A Conversation with Jeff Deist & Tom Woods

The Divided States of America | A Conversation with Jeff Deist & Tom Woods

2022-01-14

Mises Institute President, Jeff Deist, and Tom Woods, author and host of the Tom Woods podcast, join Judge Napolitano to go in-depth on the state of America today.

Tags: Featured,newsletter