– £1 trillion crisis looms as pensions deficit and consumer loans snowball out of control– UK pensions deficit soared by £100B to £710B, last month– £200B unsecured consumer credit “time bomb” warn FCA– 8.3 million people in UK with debt problems– 2.2 million people in UK are in financial distress– ‘President Trump land’ there is a savings gap of trillion– Global problem as pensions gap of developed countries growing by B per dayThere is a £1 trillion debt time bomb hanging over the United Kingdom. We are nearing the end of the timebomb’s long fuse and it looks set to explode in the coming months.No one knows how to diffuse the £1 trillion bomb and who should be taking responsibility. It is made up of two

Topics:

Jan Skoyles considers the following as important: Featured, GoldCore, newsletter, Weekly Market Update

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| – £1 trillion crisis looms as pensions deficit and consumer loans snowball out of control – UK pensions deficit soared by £100B to £710B, last month – £200B unsecured consumer credit “time bomb” warn FCA – 8.3 million people in UK with debt problems – 2.2 million people in UK are in financial distress – ‘President Trump land’ there is a savings gap of $70 trillion – Global problem as pensions gap of developed countries growing by $28B per dayThere is a £1 trillion debt time bomb hanging over the United Kingdom. We are nearing the end of the timebomb’s long fuse and it looks set to explode in the coming months.No one knows how to diffuse the £1 trillion bomb and who should be taking responsibility. It is made up of two major components.

How did the sovereign nation that is the United Kingdom of Great Britain and Northern Ireland get itself so deep in the red? This is not a problem that is bore only by the Brits. In the rest of the developed world a $70 trillion pensions deficit hangs heavy. We are all in this boat because we apparently didn’t learn from the massive man made crisis that was the 2008 financial crisis. The ‘we’ is referring to UK individuals who are on average holding £14,367 of debt. It refers to the pension fund managers who are ignoring the fact they hold more liabilities than assets. It refers to banks and mortgage and loan providers who give loans to people who are already indebted and who will struggle to pay the debt back. It refers to a compliant media who do not have ask hard questions about irresponsible lending practices and cheer lead property bubbles due to getting significant revenues from the banking and property sectors. And, ultimately the ‘we’ is the government who peddled such terrible monetary policy that it has brought us as close to nuclear financial disaster as we have been since 2008. |

- Click to enlarge |

| In the red, everywhere

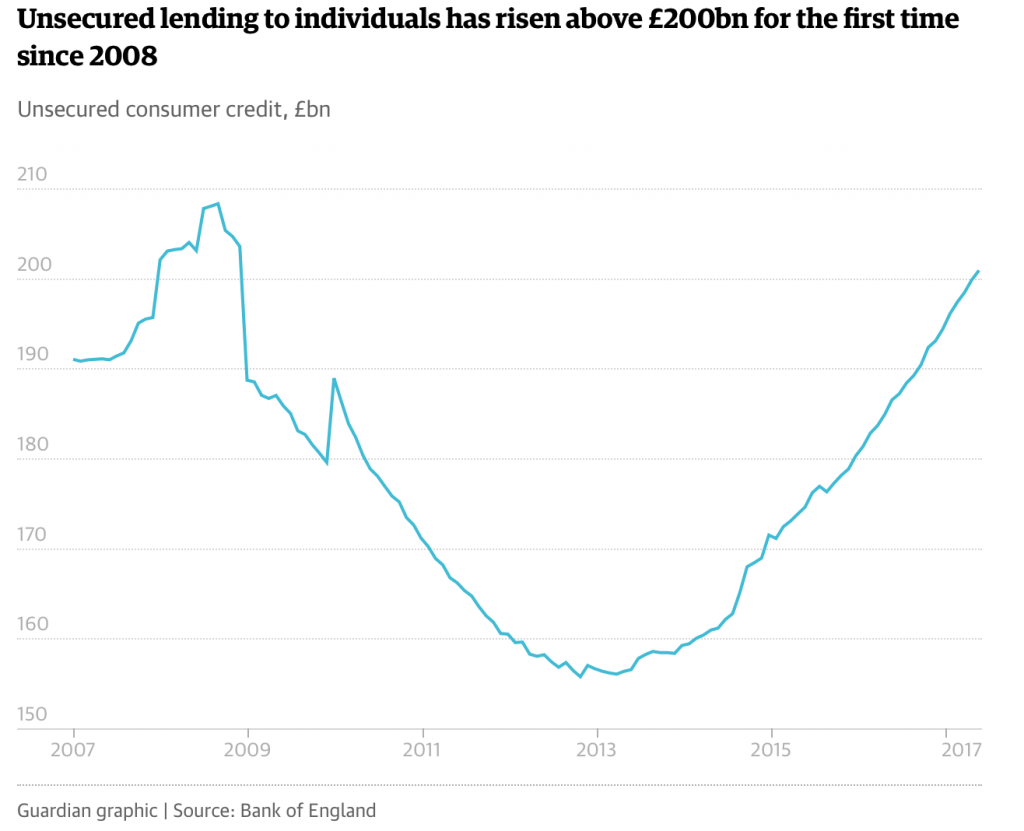

In the United Kingdom we are running a deficit not only in our day-to-day lives but also in our future lives. Unsecured consumer credit is now at 2008 levels. There is £200 billion of unsecured credit. The FCA’s Andrew Bailey has put this dangerous issue at the top of the regulator’s agenda. However it is not just for the FCA to be dealing with. There is no one organisation responsible for the huge levels of personal debt that will eventually cause this financial system to implode. There are 8.3 million people in the UK with debt problems. The number of debtors falling behind on payments increased by 40% in the first half of this year. The problem shows no sign of improving: 45% of the £65 billion of credit card debt is managed using the 0% transfer balance offers. But with half of those that transfer, the balance remains the same at the end of the period. Earlier this year the Bank of England’s director for Financial Stability warned lending standards were at risk of going ‘from responsible to reckless very quickly’. This comes to mind when you consider that 86% of cars are now bought on PCP (personal contract purchase). So concerned are financial observers with the UK’s personal debt crisis that in July this year Moody’s downgraded the outlook on bonds backed by credit card customers, buy-to-let mortgages and car loans. Greg Davies, Moody’s assistant vice president warned: “Household debt is high and still growing, leaving consumers vulnerable to an economic downturn, while higher inflation, weaker wage growth and levels of indebtedness leaves those in lower-income brackets the most exposed.” So in our day-to-day lives we are over £200bn in debt. How on earth could we possibly save for our futures? Sadly, this is a struggle as well. Not just because of our debt but thanks to the rising cost of inflation and stagnant wages and underfunded pension pots in both public and private sectors. |

Unsecured Lending to Individuals, 2007 - 2017 - Click to enlarge |

| Nest egg isn’t looking so cosy

Ageing populations, low birth rates and dire monetary policy means that over 27 million people in the UK will not be receiving adequate pensions once they retire. These 27 million are those relying on a a defined-benefit (DB) pension – such as a proportion of final salary, index-linked to inflation for life. Those who aren’t relying on a DB pension are in just as dire straits. Savers in modern defined-contribution (DC) plans – where there are no guarantees about what the pension will ultimately pay out – are at risk of not saving enough to avoid poverty in old age. This is particularly bad when you consider that listed companies may need to meet their increased DB obligations and so DC investors will see their own investments grow more slowly. In the UK it is estimated that more than one-in-five people are not saving for their pensions. Even more are uninformed about how much they will need in retirement. Low interest rates are clearly greatly exacerbating this crisis as pensions dependent on yields from bonds have seen yields fall to near zero and sometimes go to zero. Sadly there is little sign of a let-up. In the United Kingdom the pensions deficit grew by £190bn last year. In the last month it has jumped by another £100bn to £710bn. This is leading to lower-than-expected returns on both corporate and government bonds. The low corporate bond yield has significantly contributed to the growing pension deficit. Interest rates have been at record lows for over ten years thanks to easy monetary policy. Thank you Bank of England, ECB and Federal Reserve. Tom McPhail, head of retirement policy at Hargreaves Lansdown, told the Express: “Current monetary policy may have kept the economy going but it is killing pension schemes, with disastrous consequences, both for any employers sponsoring a final salary scheme and for any individuals looking to buy an annuity.” |

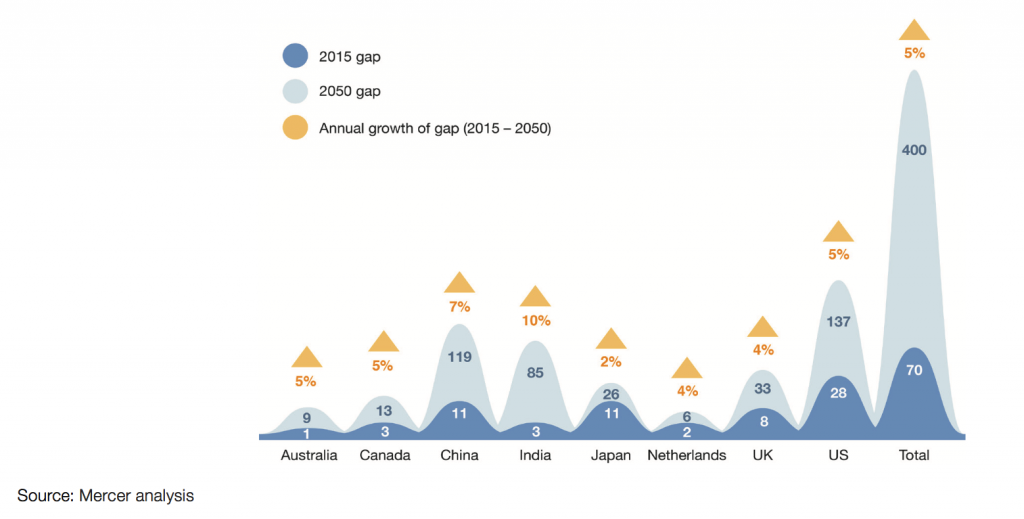

Annual Growth of Gap 2015 - 2050 - Click to enlarge |

| Developed nations with underdeveloped pensions

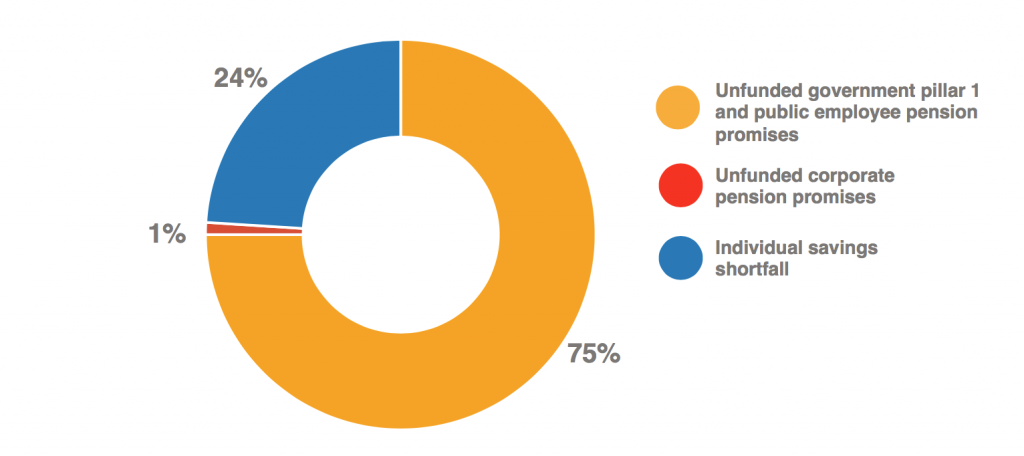

This is not a problem unique to the UK. Currently the world’s leading economies are dealing with a $70 trillion deficit. The World Economic Forum (WEF) was that this could increase to $224 trillion by 2050. If you add in India and China then this gap hits $400 trillion in 2050. The United States has the largest shortfall of the countries measured, followed closely by the United Kingdom. In the land of President Trump there is a savings gap of $70 trillion. It is growing at a rate of $3 trillion per year (5 times the annual defence budget). The overall savings gap, of the eight countries assessed, is predicted to grow at a rate of $28 billion per day. Unsurprisingly it is in India and China where the gaps will widen the quickest. 10% and 7% respectively. The global situation is so bad that the WEF has referred to the pensions deficit as ‘the financial equivalent of climate change.’ The OECD recommends pensioners have a retirement income of 70% of their earnings. This is a ‘crude’ assessment according to the WEF who argue low-income workers need closer to 100%. This is also a sex issue. According to a report in 2014, 50% more women than men cannot afford to contribute to their pensions. It is so bad for the female of the species that 30-40% of global retirement balances are lower for women than men. Where is the deficit coming from? The WEF’s report looked both public and corporate pensions. It was the government and public pensions that were the most unhealthy looking, accounting for 75% of the under funding. The WEF seemed little concerned that the largest corporate pension markets were in the UK and US, where there are over $4 trillion in liabilities. The organisation reassures itself that the market is highly regulated and the deficit ‘is modest compared to other components of the pension system’. |

Developed Nations with Underdeveloped Pensions - Click to enlarge |

Corporates and individuals should not rest on their laurels

No matter what the WEF thinks, the corporate pension market in both the U.S. and Europe is in serious bother.

A report by MSCI found North American and European companies have the largest pension underfunding levels compared with revenues.

This is not surprising. Corporations are struggling to maintain pension pots for the very same reasons the WEF believe there is a major pensions shortfall:

- Rapidly ageing populations

- Falling birth rates

- Poor access to pension products & poorly performing products with high charges

The final one is a huge one and the one which the majority of pension fund managers are unlikely to have foreseen. Individual savers even less so.

According to OECD measures the UK’s shortfall is higher than £6.2 trillion, set to increase by 4% per year. This will be over £25 trillion in 2050.

Take responsibility

The final reason the WEF gave for the current pensions disaster was ‘High degree of individual responsibility to manage pension’.

The WEF argue that the information given to individuals was not enough to expect them to understand how their pensions would work in the future and what was required of them now.

It is vital that individuals take responsibility for their pensions. You must ask questions about it as soon as possible.

Particularly, you should ask if you can invest in gold as part of your pension.

The traditional mix of equities and bonds that make up pension funds has under performed in the last 15 to 20 years.

Stock and bond markets have done well in the short term and they are artificially overvalued thanks to the easy monetary policy of central banks.

It is clear that pension funds’ overexposure to bonds and stocks has impacted pension investors returns over the long term.

With that in mind it’s sensible to allocate some of your pension to gold. Internationally, the trend for doing this is extremely low which is surprising given the role it has played in preserving and growing pension wealth.

Dr. Constantin Gurdgiev, formerly an adviser to GoldCore, says the following about the importance of having gold in your pension:

“Gold is a long-term risk management asset, not a speculative one.

As such it should be analysed and treated predominantly in the context of its role as a part of a properly structured, risk-balanced and diversified portfolio spanning the full life-cycle of the investment and pension horizon for individual investors and those with pensions.

Whether they be SIPPs in the UK or IRAs in the USA.”

Investors in the UK and Ireland, the US, the EU can invest in gold bullion in their pension, through self-administered pension funds.

UK investors can invest in gold bullion through their Self-Invested Personal Pensions (SIPPs), Irish investors can invest in gold in Small Self Administered Schemes (SSAS) and US investors can invest in gold in their Individual Retirement Accounts (IRAs).

Adding gold to your pension is a time-proven way to protect your retirement from the pensions time bomb. There is little we can do to stop it, investors should act now and take responsibility for their retirement nest egg by investing in the ultimate form of financial insurance – gold bullion.

The ‘pensions timebomb’ looms. UK pension funds’ lack of diversification and overexposure to traditional paper assets may cost pension holders dearly.

Pensions allocations to gold are very low in the UK and yet gold has an important role to play over the long term in preserving and growing pension wealth. You can read our guide about how to invest in gold in a pension in the UK here.

Tags: Featured,newsletter,Weekly Market Update